2015

2015 somebody2015 in review and a forecast for California’s housing market in 2016

2015 in review and a forecast for California’s housing market in 2016 somebodyPosted by Carrie B. Reyes | Dec 31, 2015 | Feature Articles, Laws and Regulations, Market Watch | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

What do you believe will most influence real estate sales in 2016?

- Interest rates. (51%, 159 Votes)

- Mortgage bankers and lenders. (17%, 53 Votes)

- Buyer-occupants. (14%, 42 Votes)

- Sellers. (8%, 26 Votes)

- Investors. (6%, 20 Votes)

- Builders. (3%, 9 Votes)

Total Voters: 309

Learn about the changes brought to California’s real estate market in 2015 and how they’ll impact real estate business in the coming year.

New real estate laws

Each year, federal and state governments pass new laws which affect California real estate transactions, homeowners and agents. In 2015, the biggest change took place in the world of mortgage origination disclosures.

The Consumer Financial Protection Bureau (CFPB) introduced new integrated disclosures to replace the old required consumer mortgage lender disclosures:

- The Loan Estimate replaced the Good Faith Estimate (GFE) and the initial Truth-in-Lending Statement [See RPI Form 204-5 and 221]; and

- The Closing Disclosure replaced the Settlement Statement (HUD-1) and the final Truth-in-Lending Statement. [See RPI Form 402]

There was lender concern that use of the new disclosures may delay closings and somehow hurt home sales after they took effect in October 2015, a time of the year when sales volume is greatly reduced as the norm. However, while closings slowed in November 2015, timely closings were restored by the end of the year.

One real estate-related law to look ahead to in 2016 is the newly required Office Management and Supervision (OMS) continuing education (CE) course mandatory for brokers and sales agents renewing their licenses in California. Beginning January 1, 2016, California Bureau of Real Estate (CalBRE)-licensed brokers and sales agents now need to complete an approved OMS course as part of their continuing education requirements. [Calif. Business and Professions Code § 10170.5]

Editor’s note — first tuesday was the first CE provider to include the required OMS course in every CalBRE continuing education course enrollment. View enrollment details here.

To catch up on the many other new real estate laws introduced in 2015 — most of which will take effect beginning in 2016 — see:

Economic picture — here and abroad

The big news going into 2016 is the Fed’s decision to increase the Federal Funds rate which directly affects ARM rates. This hovered around 0% from 2009 to December 2015. At that point, the Fed increased the rate to fall within their target range of 0.25%-0.5%. Looking forward, the Fed indicates they will gradually increase this short-term rate nearly one percentage point in each of the coming three years and plans for the Federal Funds rate to rest around 3%-4% by 2018.

This rate increase is of immense importance to the real estate market, since rising mortgage rates makes borrowing dollars more expensive for homebuyers. In turn, buyer purchasing power is reduced as the mortgage amount for which a buyer is able to qualify decreases. Thus, home sales volume are likely to slip and prices will suffer. 2016 won’t likely experience a decrease in prices, but by 2017 sellers (and their agents) will have lost their sticky pricing illusions and prices will dip briefly before we head into the next expansion, on the tail of a swiftly recovering jobs market.

That’s here in California, and more broadly across the nation. But the global economy experienced several setbacks in 2015, from the stalled recovery in the Eurozone and Japan to China’s renminbi decline and Brazil’s, Russia’s and Turkey’s magically shrinking economies. How do these global forces influence our U.S. economy, and more specifically the real estate market?

First, the uncertainty of many global markets causes foreign investors to eye U.S. Treasury Notes as stable. Parking their money in 10-year T-Notes is a safe bet while their own nations deal with economic setbacks. Therefore, as long as investors place heavy value on a 2% return for 10-year T-Notes, fixed rate mortgage (FRM) rates will remain near their current low rates of 4% or below. As 2016 moves along, these investors will eventually withdraw from 10-year T-Notes as they find investment opportunities in their home countries, and FRM rates will increase.

14% of real estate agents surveyed by the California Association of Realtors assisted international clients in 2014, and reports from national sources indicate the share of foreign buyers continued to rise in 2015. The largest international investor presence in California is found in San Francisco and Los Angeles.

However, international interest in owning California’s real estate will subside when foreign economies begin to improve, likely by late 2016. Most foreign investors hail from China, and investors have begun to look to more stable sources of income following China’s economic shock late in 2015. More importantly, the relatively strong U.S. dollar now makes it difficult for Chinese investors — and investors from other global economies in poor shape — to purchase U.S. real estate in 2016. Therefore, expect to see the investor presence decline somewhat throughout 2016.

California’s housing market

California’s housing market experienced a modest boost in 2015 over the previous year. Home sales volume increased about 9% over 2014, with roughly 39,000 more homes sold in 2015. For historical perspective, 2015 is about level with 2013, a year when speculator buying greatly increased sales volume, and about 300,000 — or 40% — less than the number of homes sold in 2005 during the Millennium Boom’s peak.

Home prices also increased in 2015, ending the year 7%-10% higher than the same time at the end of 2014. Prices increased more quickly in low-tier homes and less so in high-tier homes, continuing the bumpy plateau sales volume experienced throughout this long recovery.

Construction across California continued to recover in 2015, but at a reduced pace. Single family residential (SFR) construction starts rose by 10% over the previous year. Multi-family construction rose by 20% over 2014.

This is an impressive recovery for multi-family starts, which experienced the best year since the multi-family boom of the 1980s. However, SFR construction starts still have much room for improvement, currently experiencing only one-quarter of the construction pace of the Millennium Boom.

Going forward, expect history to repeat itself. In the 1980s, the Baby Boomer generation produced high demand for multi-family rentals as they graduated and finally found jobs. This environment fueled the boom in multi-family construction. In the following decade, their desire to trade up for SFR housing fueled the late 1980’s and l990’s boom in SFR construction.

Now, the children of the Baby Boomer generation — Generation Y (Gen Y) — are finally coming of age, albeit belatedly in the aftermath of the Great Recession. As Gen Y moves out of dorms and parents’ basements and look for apartments to rent or buy at a reduced cost near urban employment centers, multi-family will continue to outpace SFR construction, swelling to a peak around 2020.The shift from apartments to SFRs for Gen Ys will then create vacancies in apartments, as occurred in the early 1990s.

Extended forecast for California’s real estate market

How will home sales volume and prices likely fare in 2016 and beyond?

Sales volume is likely to continue its rise through the first part of 2016 as job numbers continue to grow. But this growth will be short-lived, to fall back in the months following the inevitable FRM rate increase. The FRM rate rise is likely to occur after mid-2016, thus sales volume will likely slip in the second half of 2016.

Anticipate prices to continue to rise slightly throughout 2016. However, after home sales volume trends down due to the FRM rate increase, expect prices to follow within 9-12 months. Absent other extraneous factors (like rampant speculation, as occurred in 2012-2014), prices follow home sales volume movement axiomatically.

Strategic defaults and bankruptcies will rise slightly heading into 2018, as occurred during the mid-1980s and mid-1990s recoveries when the Fed raised rates for the first time in those recovery periods.

The good news for sellers — not buyers — is home prices won’t stay down for long, despite interest rate increases. The jobs recovery will give home sales a needed boost in 2018, which will cause prices to begin rising again around mid-2018, first led by returning speculator acquisitions, then end user occupants. Increased construction starts will fill user demand for more housing in coastal city centers.

Rents and prices will then rise dramatically with demand centered in urban areas close to the best-paid employment, but less so in inland regions. Smaller coastal cities will likely fail to lift zoning restrictions on much needed high-density, high-rise multi-family starts driving Gen Y to other communities. Members of Gen Y will enter the rental and homebuying market en masse; in a demand convergence, their Baby Boomer parents will continue to retire in increasing numbers, selling and buying rather than renting. Home inventory for sale will be tight without new zoning and construction, causing prices to rise.

As a result, new real estate licensees will flood the market, large broker firms adding sales agents to match the cyclically higher sales volume.

Flying into all this excess, the Fed is likely to induce the next business recession. The hope is the Fed won’t let the economy get too out of hand before acting to cool it off, and risk another Great Recession and zero-to-negative interest rates.

Factors to watch out for in 2016 and beyond:

- Keep an eye on foreign investors in your local real estate market. The global upheaval makes the U.S. a very attractive place to invest, but the strong dollar makes it difficult for foreign investors to enter the U.S. dollar-dominated asset market.

- Watch for interest rates increases. While the short-term rate began to increase in December 2015 and immediately affect ARM rates, first tuesday expects FRM rates to increase later, after mid-2016 due to investor movement. But no matter when FRM rates do rise, prepare for sales volume to decline and prices to follow, albeit briefly.

- Stay informed on movements in your local jobs market. While influenced by global and national economics, real estate is significantly a local phenomenon. Therefore, future housing market movement can be foreseen in improvements (or failures) in the quality and quantity of employment immediately available to the local population.

Related topics:

california home prices, california real estate, construction, foreign real estate investor, law

Become a military-friendly real estate agent!

Become a military-friendly real estate agent! somebodyPosted by Carrie B. Reyes | Jun 26, 2015 | Buyers and Sellers, Your Practice | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

If you’re a real estate agent near a military base — and you likely are since California is home to dozens of military bases — you’ve probably had the privilege of assisting a military family buy, rent or sell a home.

Serving in the military usually means moving within a couple years of arriving in a new community. Turnover is high and time is especially important when buying and selling. It’s a challenge for military homeowners. Agents assisting military homeowners share in the challenge, but have the opportunity to develop expertise in a niche market with a great referral base.

In most cases, a homebuyer needs to reside in their home for two-to-five years (depending on the location) for owning to make more financial sense than renting, mostly due to transaction costs. In California’s largest military populace — San Diego — the average breakeven horizon when buying makes more sense than renting is 3.8 years.

Therefore, to avoid losing money on a home purchase, a military homebuyer in San Diego either has to:

- bet on getting reassigned to the same duty station at the end of their current (usually two-year) tour; or

- plan to rent their home out after they move.

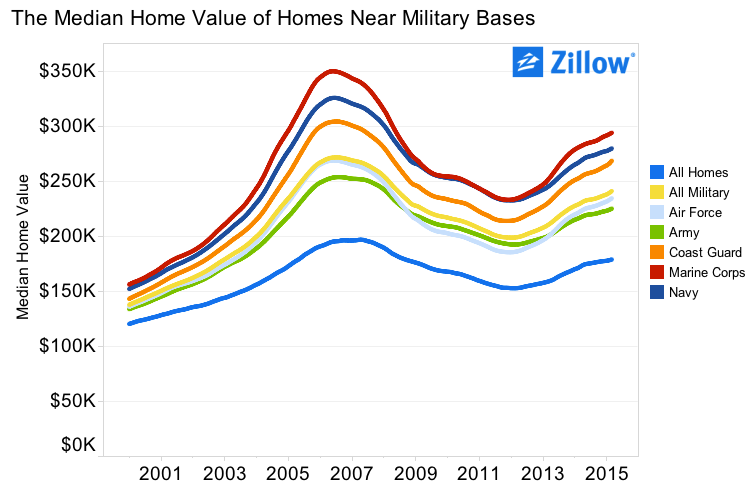

San Diego military families also have it hard when it comes to home prices. The median home value near military bases is $588,000, according to Zillow. This is 24% higher than the San Diego County average media home value of $475,000.

This same analysis shows home prices are more volatile near military bases regardless of the location:

Source: Zillow

How do military bases support home prices?

Given the hardships and uncertainty of homebuying as a member of the military, how do home prices stay significantly elevated in areas dependent on a large military population?

It’s possible the high turnover rate of military homebuyers — on top of the reliable income provided by military jobs — give home prices an extra boost.

Further, each active duty military member receives a basic housing allowance. The housing allowance acts as a subsidy inflating local home prices.

Basic housing allowance amounts are based on the servicemembers’s duty location, pay grade and whether or not the member has dependents. This housing allowance is meant to cover a family’s housing expenses typical to the area. The housing allowance is usually adjusted annually, based on changes in the local economy.

Current housing allowance amounts are available here.

This housing allowance is a helpful yardstick, and not just for military homebuyers. It’s also used by military homebuyers-turned-landlords when they move away from their duty stations.

For example, when a military family finds out they are scheduled to move, finding a renter is as easy as contacting their network to find another military family that has orders to that duty station. Looking up the housing allowance gives the military landlord an easy way to determine how much rent to charge.

The agent’s role

Real estate agents in areas with large military populations ought to take advantage of the opportunities presented. These include serving as the:

- buyer’s agent for military families new to the area;

- property manager for families choosing to rent out their homes when they move away; and

- seller’s agent when the military family eventually sells.

Since military turnover is continuous, make sure you let current military clients know you’re happy to help their military colleagues who are new to the area. The military community is tightly knit. One military referral goes a long way.

Having trouble getting your foot in the door? Try these steps:

- familiarize yourself with the ins-ands-outs of U.S. Department of Veterans Affairs (VA) mortgages;

- advertise your willingness to work with military families on your real estate website and marketing materials; and

- specify that you are a relocation specialist for active-duty military.

Are you already “in” with the military community? What are your tips? Share them in the comments!

Related article:

Related topics:

department of veterans affairs (va), home prices, military,

CALIFORNIA LAW AND THE MFDRA EXTENSION: WHO ESCAPES TAXABLE INCOME?

CALIFORNIA LAW AND THE MFDRA EXTENSION: WHO ESCAPES TAXABLE INCOME? somebodyPosted by Amy Thomas | Aug 25, 2015 | Laws and Regulations, Real Estate, Tax | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Once again, the neck of the Mortgage Forgiveness Debt Relief Act (MFDRA) is in the guillotine. Senators Dean Heller of Nevada and Debbie Stabenow of Michigan intend to rescue the home foreclosure tax relief, advocating the creation of a bipartisan bill to extend the act’s protections through 2016.

This is the second time the MFDRA has come before Congress for an extension. The last extension in 2014 squeaked by to pass on December 31, 2014. The new extension is likely destined for the same fate – several months have already crawled by with no action from Congress for underwater homeowners – those exposed to short sales and foreclosures.

Another bill attempting to permanently exclude mortgage forgiveness debt from taxable income has been introduced, but the likelihood of either coming into effect is wishful thinking.

Is the MFDRA extension a big deal in California?

The effect of the MFDRA extension on California residents depends on whether a mortgage is a recourse or nonrecourse debt. California law determines purchase-assist debt secured by a one-to-four unit principal residence and discharged on a short sale (or foreclosure) is nonrecourse debt.

Discharge of indebtedness income due to the discount (short pay) on the short sale of a property encumbered by a nonrecourse debt is exempt from taxation as income under federal tax law. This protection is separate and unaffected by the outcome of the battle over another MFDRA extension. [26 Code of Federal Regulations §1.1001-2(a)(2), Internal Revenue Code §108(e), Calif. Code of Civil Procedure §580(e), Calif. Revenue & Tax Code §17144.5]

The MFDRA (and conforming state bills) would extend the protection for nonrecourse debt forgiveness to recourse debts forgiven through the end of 2014. The current state bill to extend this exemption is currently under consideration, pending budgetary review.

Most mortgaged California homeowners owe nonrecourse debt. Thus they are protected from taxation on discharge-of-indebtedness income on a short sale or foreclosure underbid regardless of the MFDRA and state bill extensions. [Calif. Rev & T C §17144.5]

However, a homeowner facing an underwater property encumbered with recourse debt needs to consider whether a short sale or a foreclosure will benefit them most.

Short sales require the homeowner with recourse debt to negotiate with the lender, who needs to agree to a discount if the sale is to close. The sale price of the home is less than the money owed to the lender, meaning the discount on the debt is still forgiven – a recourse debt which, without the special tax exemptions provided by the MFDRA, qualifies as taxable income.

Without the lender’s agreement to a short sale, a homeowner may still escape recourse debt by allowing the lender to initiate foreclosure of the property through a trustee’s sale. A trustee’s sale ultimately blocks the lender from obtaining a deficiency judgment for the remainder of the recourse debt. [CCP §580d]

However, homeowners who turn to strategic default by allowing lenders to foreclose through a trustee’s sale will take a hit to their credit score. Lower credit scores may raise interest rates homeowners must pay on future mortgages, or make it more difficult for homeowners to obtain mortgages in the first place.

Homeowners with recourse debt need to prepare their finances for the next few years in advance, then take a calculated hit to their credit scores and allow the property to go to foreclosure.

Taxable income without the MFDRA

Other states not sharing California’s tax exemption laws rely on the MFDRA’s protection. Without it, federal tax codes treat mortgage forgiveness discounts as taxable income. Thus, the option of a short sale without detrimental taxes is not available on discounts in those states. Taxes on mortgage forgiveness discounts may cost homeowners of properties encumbered with recourse debt tens of thousands of dollars in “income” they never personally received – though they did receive a home on the bet it would not fall in value below the mortgage which funded its acquisition.

Many homeowners who may have escaped heavy debt burdens through short sales and foreclosures opted to stay put for fear of incurring indomitable taxes.

The further we get from the housing crisis, the less likely it is Congress and the government will continue to subsidize forgiveness for recourse debt. If you still have clients in this situation, help them choose what to do sooner rather than later.

Re: “Mortgage debt forgiveness still a taxing issue for many short sellers,” from the Los Angeles Times

Related topics:

strategic default

CASE IN POINT: IS A STATE HOUSING AGENCY LIABLE FOR DISPARATE IMPACT UNDER THE FAIR HOUSING ACT WHEN THEIR ACTIONS RESULT IN CONTINUING SEGREGATION?

CASE IN POINT: IS A STATE HOUSING AGENCY LIABLE FOR DISPARATE IMPACT UNDER THE FAIR HOUSING ACT WHEN THEIR ACTIONS RESULT IN CONTINUING SEGREGATION? somebodyPosted by Amy Thomas | Aug 7, 2015 | Fair Housing, Laws and Regulations, Real Estate, Recent Case Decisions | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Facts: Low-income housing tax credits provided by the federal government are distributed by a state housing agency to encourage local housing investors to accommodate marginalized, low-income residents. The state agency enacted plans for the fair distribution of federal tax credits in accordance with the Fair Housing Act (the Act). A state housing agency allocated these credits according to occupants’ income levels and available state funds for housing developers. The agency’s allocation of the low-income housing tax credits mainly favored inner-city areas with predominantly minority populations over suburban areas with predominantly Caucasian populations.

Claim: A nonprofit organization which helps low-income families obtain affordable housing claims the state housing agency is causing a disparate impact since the agency’s allocation of tax credits contributes to greater segregated housing by allotting more credits to inner-city areas than suburbs, leading to a concentration of low-income housing in minority neighborhoods and perpetuating segregated housing patterns in violation of the Act.

Counterclaim: The state housing agency claims it is not liable for disparate impact resulting from their allocations since it did not intend to promote segregated housing patterns and its allocation of tax credits is not motivated by race but based on government interests.

Holding: The U.S. Supreme Court holds the state housing agency is liable for creating a disparate impact and needs to alter its allocation process since, intended or not, the agency’s allocation of tax credits concentrates low-income housing in minority neighborhoods which perpetuates segregated housing patterns in violation of the Act. [Texas Department of Housing and Community Affairs v. Inclusive Communities Project, Inc. (June 26, 2015) ___ U.S. ___]

Disparate impact, housing patterns and the federal Fair Housing Act

The issue of disparate impact is brought to light by this US Supreme Court ruling that a state housing agency is liable for inadvertently magnifying segregated housing patterns in the above 2015 case of Texas Department of Housing and Community Affairs v. Inclusive Communities Project, Inc.

Disparate impact is the perpetuation of segregated housing in a community caused by any agency’s actions, regardless of intent to discriminate.

The question answered by the Supreme Court’s decision is whether state agencies are liable for disparate impact under the Federal Fair Housing Act of 1968 (the Act). No explicit wording in the Act condemns agencies for unintentionally causing disparate impact; rather, the Court interpreted the Act’s provisions to include the consequences of an agency’s actions regardless of the agency’s intentions.

Unintended consequences under the Fair Housing Act

State agencies distribute federal tax credits to landlords, who are required to designate units for low-income housing in their communities. Low-income occupants – a protected class of tenants – are provided vouchers to obtain housing from landlords who receive those credits. Thus, when a state agency distributes federal tax credits unequally across a community, limiting low-income tenants to specific areas (a concept related to steering), the agency’s action creates a disparate impact.

The Court relies on two of the Act’s provisions:

-

- “[It is unlawful] to refuse to sell or rent after the making of a bona fide offer, or to refuse to negotiate for the sale or rental of, or otherwise make unavailable or deny, a dwelling to any person because of race, color, religion, sex, familial status, or national origin” [Federal Fair Housing Act §804(a)]; and

- “It shall be unlawful for any person or other entity whose business includes engaging in real estate-related transactions to discriminate against any person in making available such a transaction, or in the terms or conditions of such a transaction, because of race, color, religion, sex, handicap, familial status, or national origin.” [FFHA §805(a)]

The phrase “make unavailable” is the Court’s focus in these sections. The Court determined that phrase to equivocate disparate impact by encompassing the effects of an agency’s actions regardless of intent.

Perhaps the best parallel to disparate impact is implicit discrimination, which is defined as actions which are not openly discriminatory but in fact result in discriminatory effects. Implicit discrimination may occur if a lender offers financing only to qualified buyers (a legal practice), but those qualified buyers in turn populate what becomes a community of a sole demographic – the result being segregation, balkanization, ethnic enclaves and ghettos, you name it.

Disparate impact is a slippery slope

Disparate impact cases work to oppose the perpetuation of segregated housing. However, the nebulous terminology of the Act makes disparate impact a difficult disease to diagnose in agency activities.

Victims of disparate impact – segregation by implication – are required to file a complaint with the California Bureau of Real Estate (CalBRE) for any appropriate administrative discipline on guilty licensees (brokers and agents). Thus, the CalBRE evaluates any disparate impact consequences of the licensee’s behavior on a case-by-case basis.

Diversity quotas are the main concern for dissenters of the Court’s decision. How may an agency be certain it is not imposing disparate impact on a community unless it fills a specific diversity quota? Also, housing agencies may fear the Court’s disparate impact ruling which disregards discriminatory intent will subject them to judicial action despite active efforts to assist protected groups in the greatest need of funding or housing, as occurred in the Texas case.

Litigation is another fear for housing agencies. Disparate impact opens housing agencies to liability when tenants feel slighted by the adverse segregation result of a practice proper on its face. If housing agencies are not protected under the Act when legally allocating resources which eventually produce unintended tangential consequences of continuing segregation, how are they to defend against what may potentially be mobs of victims?

Such fears may foster paranoia and drive housing agencies to double-up their defenses. This may raise the cost of funding for those who are vulnerable and in need of financial assistance — the very class of people these agencies were created to protect. However, fear of litigation is a classic response to nearly all cases that protect members of the public from corporate or government action.

Disparate impact ruling is an opportunity for expansion

Excessive litigation will not be a problem for those housing agencies willing to expand their practices equally among all sections of the community to disseminate previously neglected populations – the low-income families. Many minority buyers and tenants are perceived as high-risk due to allegedly “unstable” circumstances, like working multiple jobs to make ends meet. If housing agencies, lenders and landlords kick their preferential penchant for single-income sources, chances are perceptions of their disparate impact will dissolve on their own.

For brokers, disparate impact liability is easy to eliminate by supporting equal treatment as an enduring real estate practice. Brokers who educate their agents on Fair Housing conduct will enjoy the unhindered business of equal opportunities provided to buyers of all demographics. All buyers want is shelter, and MLS brokers and agents provide access to shelter; a perfect match without the noise of archaic societal bias. Simple practices like thinking about and asking only questions pertinent to the housing transaction at hand will minimize brokers’ risk of liability.

The Act prohibits discrimination of any kind in:

- the advertisement, sale or rental of a residential space;

- brokerage services offered or performed;

- the origination of mortgages to purchase, build, improve or repair a residence;

- purchase-assist financing; and

- real estate appraisals. [See first tuesday Fair Housing Chapter 1: The Federal Fair Housing Act]

Check your habits as an agent or broker. Confirm you are allowing an equal shot at buying or renting to all persons inquiring about satisfying their housing needs, and adjust your practice where necessary.

Disparate impact may seem like a shapeless threat, especially for licensees with deep-felt beliefs about different classes of protected individuals. But those beliefs only threaten those licensees desperate to conserve outdated social mores and perspectives, unwilling to expand their business into all demographics and enhance their potential to flourish.

Related topics:

implicit discrimination, liability

CFPB crackdown: Marketing Services Agreements (MSAs) with brokers

CFPB crackdown: Marketing Services Agreements (MSAs) with brokers somebodyPosted by Amy Thomas | Dec 28, 2015 | Fundamentals, Laws and Regulations, Real Estate, Your Practice | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Dubious real estate brokers are slicking their pockets in yet another way, as exposed by the Consumer Financial Protection Bureau’s (CFPB) recent bulletin.

The latest fad for California Bureau of Real Estate (CalBRE) licensed professionals, mostly employing brokers, looking to sidestep the Real Estate Settlement Procedures Act (RESPA) prohibitions is the use of marketing services agreements (MSA).

Brokers enter into MSAs with companies that provide services their buyers and sellers need to close real estate transactions involving a consumer mortgage origination, such as:

- mortgage lenders and loan brokers, known as mortgage loan originators (MLOs);

- title insurance companies;

- escrow companies;

- appraisal services;

- home warranty insurers; and

- home inspection companies.

When used lawfully, sales transaction providers use MSAs to employ third parties, generally marketing agencies, to advertise and promote their services. For example, promotional or educational events and services may be performed by a third party on behalf of a mortgage loan broker or lender or other provider so long as the third party, say a multiple listing service (MLS) broker for purposes of this RESPA avoidance scheme, is actually rendering services of equal value to the amounts paid under the MSA.

However, brokers and their agents often believe that by not asking for a referral fee, an agent is “leaving money on the table.” Thus, MSAs are created by brokerages with third-party providers to a sales transaction to drive brokerage-generated business exclusively to the provider in exchange for a referral fee. This activity is illegal under RESPA when the transaction includes the origination of a consumer mortgage.

Payment is limited to the value of the actual services provided as promotional, educational or rental activities. Specifically, the amount paid may not be received by the broker or agent in exchange for or contingent upon the broker or agent’s referral of a buyer or seller to an MLO, escrow or title insurer, or other provider in a transaction in which a consumer mortgage is originated. [12 Code of Federal Regulations §1024.14(vi)]

However, the CFPB has received an increase in complaints made by consumers, competing MLOs and other providers, and real estate professionals who are yet uncorrupted and do not take these illegal referral fees. These complaints claim MSAs are a cover entered into by providers for payment of kickbacks to real estate agents in violation of RESPA’s anti-kickback regulations. Further, a second fee for the agent’s referral of their client to a provider in expectation of some manner of payment which is not reported to the client violates CalBRE real estate law.

Lenders, MLOs, real estate licensees and title companies are among the top exploiters of MSAs as a disguised method of paying and receiving these unlawful referral fees, or kickbacks. Brokerages pass good leads on to mortgage companies and title reps for referral fees in various forms.

Kickbacks may be disguised by providers and brokers as payment in a form other than a referral fee, such as an office holiday party, catered lunch for the brokerage office or the rental of a cubby for the provider’s representative when the values involved are nowhere near the amount of the money paid to the broker.

RESPA prohibitions: How kickbacks work

Kickbacks in consumer mortgage transactions – sales with financing for a buyer-occupant of a home – have been prohibited since the inception of RESPA in 1974. However, it seems many real estate brokers and their agents are simply unable to grasp the concept of “forbidden.” They cannot break the illegal habit of juicing up the fees in a sales transaction that includes financing by a consumer mortgage in which they are receiving a fee.

RESPA specifically prohibits any kickbacks or referral fees, including gifts, special privileges or payments implicitly contingent on referrals, paid to or received by any participants in a sales transaction unless the broker receiving the payment actually performs additional services of equal value to the payment of the second fee beyond activities they were hired to perform for their seller or buyer client in the single real estate transaction. [12 United States Code §2601(b)(2)]

In plain language, any sum of money paid to a broker or their agent by a lender, title insurance company, escrow or other provider of real estate sales related services is unlawful when:

- the transaction includes the origination of a consumer mortgage at closing, usually contingent on the purchase of a home by a buyer-occupant;

- a real estate licensee receives payment for their brokerage services as a transaction agent on the sale from the seller or the buyer;

- the broker or agent refers or directs the buyer to a mortgage loan broker or lender, or the buyer or seller to other providers in the transaction such as title insurer or escrow;

- the MLO broker, lender or other provider involved is paid by the buyer or seller for the services they render to close the sales transaction; and

- the provider pays the broker (or their agent, illegally circumventing their broker) directly or indirectly a fee for the referral in the transaction.

Thus, the real estate broker or their agent is paid twice on one purchase: once lawfully as a transaction agent for negotiating a sales transaction including a federally-controlled consumer mortgage, and once unlawfully for – what exactly?

That’s right: nothing. A broker’s referral of a client to a provider is an integral part of the services a transaction agent performs for the fee on the purchase transaction. The agent who does not perform additional services beyond the referral on behalf of the provider paying the kickback fee has not earned the right to an additional fee on a sales transaction negotiated on behalf of their client.

Motivations and consequences for creating MSAs

Many brokers enter into MSAs with providers to maintain a “closed office” – a brokerage office which exclusively (and illegally) refers clients to a specific provider, such as an MLO broker, in exchange for a referral fee. Competitors of the fee-paying provider are not permitted to access agents in the office, and thus the office is closed to competitors.

By maintaining closed offices, brokerages are trying to create a second profit center arising out of one purchase transaction. Providing the aforementioned special privileges, gifts or money is explicitly forbidden by RESPA but taken illegally in the interest of creating a second profit center on a single sales transaction.

The surge in complaints to the CFPB suggests many brokers and their agents see MSAs offered by providers for referrals as an easy scapegoat for suspicious and undisclosed fees. Agents beware – violators of RESPA regulations are subject to punishment in the form of:

- up to $10,000 in fines;

- a prison sentence of up to one year; and

- liability to the buyer in an amount equal to three times the amount of the kickback fee received. [12 USC §2607(d)]

To date, the CFPB has collected $75 million in violation penalties due to the use of MSAs as disguised kickbacks. Additionally, the CFPB may prohibit violators from working in the MLO industry in any aspect for a period of five years. [See Consumer Financial Protection Bureau Bulletin 2015-05]

Even brokers who attempt to enter into MSAs adhering to RESPA guidelines to receive additional fees on a sales transaction they have negotiated are at risk for noncompliance. Brokers and their agents need to brush up on fee distribution requirements in real estate transactions to ensure every fee is accounted for as received by the broker and in payment only for the service rendered to their buyer or seller client on a single transaction – the referral being part of that service and not one entitling them to an additional fee.

Source: “CFPB provides guidance about marketing services agreements,” from the CFPB Newsroom

Related topics:

consumer financial protection bureau (cfpb), department of real estate (dre), kickbacks, real estate settlement procedures act (respa), referral fees

CFPB releases mortgage shopping tools for your buyers

CFPB releases mortgage shopping tools for your buyers somebodyPosted by ft Editorial Staff | Nov 16, 2015 | Buyers and Sellers, Finance | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

If you haven’t checked out the website of the Consumer Financial Protection Bureau (CFPB) lately, you and your clients are missing out on some seriously helpful — and free — information.

The CFPB provides many more services than its name suggests: in addition to “protecting consumers” from financial fraud and malpractice, it has taken preventative measures to ensure homebuyers are well-informed about the homebuying process. The educational tools available on the CFPB’s Owning a Home website mitigate the risk of homebuyers falling prey to fraudsters, or biting off more mortgage than their finances can sustainably handle.

The best part of all these tools is that they are easy to understand, for both real estate insiders and average homebuyers.

The CFPB’s Owning a Home site features the most innovative tools released by the CFPB to date. Real estate agents can use this site in two ways:

- study it themselves to become more familiar with the new Know Before You Owe rules; or

- forward, post or print out the CFPB’s various booklets and infographics on the homebuying process and share them with clients.

One of these valuable tools is the “Your Home Loan Toolkit.” This toolkit includes a step-by-step guide to the mortgage process and easy-to-use checklists and worksheets. Homebuyers can reference this toolkit as they go through the homebuying process, in conjunction with the steps outlined in the Owning a Home site.

Before beginning the homebuying process, a homebuyer may first visit the first stage of the CFPB’s site: Owning a home: Prepare to shop. Here, homebuyers are instructed to go through a list of necessary activities and analyze their financial motivations to prepare them for taking out the most compatible mortgage available. These simple but critical introductory activities include:

- checking their credit score;

- assessing their spending habits; and

- budgeting and pulling together the material necessary to submit mortgage applications to multiple lenders.

Next, the homebuyer visits: Owning a home: Explore loan choices. At this page, they are guided through the different types of mortgages widely available on the open market and the estimated fees and costs associated with each type of mortgage product. It also directs the homebuyer to select three or more lenders to submit their loan application to in order to find the most competitive offer and terms. [See RPI Form 312]

Next on the topic of mortgage finance, the homeowner visits: Owning a home: Compare loan offers. Here, they are instructed how to weigh the loan estimates received from each lender they contacted. This page also assists the homebuyer choose the best mortgage for their housing needs. They are instructed to get a prequalification letter from their lender of choice.

After the homebuyer has selected their lender and mortgage they would like to close on, they graduate to the last section of the page: Owning a home: Get ready to close. This section guides them through the closing process, which includes:

- scheduling a home inspection;

- shopping for homeowner’s insurance and title insurance; and

- reviewing and understanding final mortgage documents.

Real estate agents can send their homebuyer clients to each of these pages as they navigate through the intricacies of the homebuying process.

Toolkits like these are important to maintaining informed homebuyers, particularly as we emerge from the biggest housing crash in a generation. The crash was caused by numerous factors, chief among them the convergence of unrestrained banks (wolves) and over-confident homebuyers (sheep). As we move forward, lenders now need to follow new Dodd-Frank rules and consumers need to complete various checklists and in some cases counseling before they can take out a mortgage.

Still, an “information gap” remains between homebuyers and lenders, according to CFPB Director, Richard Cordray. That’s simply because lenders originate mortgages for a living and homebuyers will only take out a mortgage a few times in their lives, if that. Enter the CFPB’s many tools to rebalance this asymmetry of information.

Related topics:

consumer financial protection bureau (cfpb)

CID manager regulations extended

CID manager regulations extended somebodyPosted by Sarah Kolvas | Feb 23, 2015 | Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Calif. Business and Professions Code §11506

Amended by S.B. 1243

Effective date: January 1, 2015

The sunset date for laws regarding common interest development (CID) managers has been extended from January 1, 2015 to January 1, 2019. Generally, these laws control the:

- certification and education requirements for becoming a CID manager;

- disclosures CID managers need to provide to the board of directors of a homeowners’ association (HOA); and

- prohibited business practices for CID managers.

Read more:

Related topics:

CalBRE may issue citation for unlawful advertisements

CalBRE may issue citation for unlawful advertisements somebodyPosted by Sarah Kolvas | Feb 23, 2015 | Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Calif. Business and Professions Code §149

Amended by S.B. 1243

Effective date: January 1, 2015

Unlawful advertisements

If an unlicensed person publishes an advertisement in any medium offering real estate services requiring a license, the California Bureau of Real Estate (CalBRE) may issue a citation requiring the person to:

- cease the unlawful advertising; and

- notify the telephone company providing service to the person to disconnect service to the phone number used in the unlawful advertisement.

If the violating person fails to comply, CalBRE may inform the Public Utilities Commission to require the telephone servicer to disconnect service to the phone number in the unlawful advertisement.

Read more:

Related topics:

CalBRE meeting notices

CalBRE meeting notices somebodyPosted by Sarah Kolvas | Feb 23, 2015 | Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Calif. Business and Professions Code §101.7

Amended by S.B. 1243

Effective date: January 1, 2015

The California Bureau of Real Estate (CalBRE) is now required to provide written notice of CalBRE public meetings by e-mail, regular mail or both to anyone who requests it.

CalBRE is also required to include in the meeting notice any plans to web cast the meeting if it intends to do so.

Editor’s note — Currently, CalBRE posts all public meeting notices to their web site. CalBRE’s public meetings allow it to educate members of the real estate industry on new laws, receive feedback from real estate professionals about the current marketplace and answer questions from the public.

Read more:

Related topics:

CalBRE prohibited from denying license due to dismissed conviction

CalBRE prohibited from denying license due to dismissed conviction somebodyPosted by Sarah Kolvas | Jan 5, 2015 | Laws and Regulations, New Laws, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Calif. Business and Professions Code §480

Amended by A.B. 2396

Effective date: January 1, 2015

The California Bureau of Real Estate (CalBRE) may not deny a license to an applicant based solely on an applicant’s dismissed conviction if:

- the applicant has fulfilled all conditions for probation and received a certificate of rehabilitation; or

- the conviction has otherwise been dismissed or set aside by a court.

The applicant is to provide CalBRE with proof of dismissal.

Editor’s note — All applicants are also required to disclose all past convictions and criminal activity. For a more in-depth discussion about licensing requirements and the application process, please see the first tuesday article, Eligibility for a CalBRE salesperson license

Read more:

Related topics:

California’s zoning pioneers

California’s zoning pioneers somebodyPosted by ft Editorial Staff | May 13, 2015 | Commercial, Feature Articles, Investment, Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Let’s play a quick word association game. The word is: zoning.

Zoning is associated with many negative aspects of the housing market, including: red tape, regulations, height restrictions, parking restrictions, stifled growth and angry neighbors. A poor, outdated zoning code can cause a multitude of problems for local housing. But zoning doesn’t always have to be a problem: zoning can be a good thing for housing growth, if it is molded with the right goals in mind.

How can zoning change make a positive difference? Consider one of the biggest problems facing California’s urban areas: a lack of multi-family housing. In the aftermath of the 2008 recession, tens of thousands of homeowners lost their homes to foreclosure and became renters.

This spike in demand coincided with the influx of new young adult renters from Generation Y (Gen Y), who have only recently left the nest and are now looking for rentals near jobs in the city.

The lack of sufficient rental housing is causing rents and home prices to shoot up beyond the rate of income growth. In turn, the homeownership rate for these urban areas continues to decline as renters pour more than their share of income into rent, cutting out potential down payment savings.

Zoning to allow more multi-family housing developments alleviates the rental crush, and frees up funds for down payment savings.

But too often, zoning is decided by vocal not in my backyard (NIMBY) advocates. These residents have a stake in keeping their neighborhood just the way it is – meaning low density. A classic example is San Francisco, with its severe building height restrictions and its impossibly high cost of living.

Fighting NIMBYism is an uphill battle. As a result, zoning change, when it happens, is a slow process.

But it is getting done. This article outlines three organizations working to make successful zoning change to better meet the demands of local residents. Each of these organizations is working to change zoning in their own way, and you can get involved, too.

San Francisco – SPUR

Source: SPUR

Location: SPUR (formerly the San Francisco Planning and Urban Research Association) has offices in San Francisco, Oakland and San Jose.

What they do: SPUR is a non-profit organization focusing on advocacy and research for city planning and governance in the Bay Area. It has existed since the 1906 San Francisco fire and has fostered a lot of change over the years, including shaping the Bay Area Rapid Transit (BART) system and several downtown and recreation areas.

Current projects include instituting laws to allow for in-law apartments, and creating Affordable-by-Design living units.

SPUR’s focus is on eight areas:

- Community planning;

- Disaster planning (earthquakes);

- Economic development;

- Good government;

- Housing (affordability, including more multi-family housing, fewer parking requirements);

- Regional planning (focusing on how to help their city grow, not suburban growth);

- Sustainable development (reducing San Francisco’s ecological imprint and responding to climate change); and

- Transportation (making public transportation accessible and affordable).

How to become involved: SPUR is a non-profit organization, funded by individual donations. The easiest way to donate is to become a member (which starts at $35/year for low-income individuals or $75 for everyone else) and in turn you get an annual subscription to their magazine, The Urbanist, and discounted or free admission to their many events.

Los Angeles – re:code LA

Source: re:code LA

Location: re:code LA operates out of the Los Angeles Department of City Planning.

What they do: This is a project of the City of Los Angeles to streamline and simplify the city’s bloated 600-page monster of a zoning code.

The current code consists of base zones such as R-1, R-2, C-1 etc., plus special overlay zones and site-specific conditions, resulting in 60% of the property in the city having at least two different types of land use controls (many with more).

Thus, a C-1 property (general commercial) will have not just the typical siting, density and design requirements of that particular zone type, but also potentially:

- a location-specific floor-area ratio (FAR) restriction;

- a district height restriction;

- an overlay zoning prohibiting additional uses otherwise allowed in the C-1 zone;

- a neighborhood-specific ordinance triggering additional public review/approval for certain uses;

- special district parking requirements; and much more.

This can make developing or improving properties an expensive, drawn-out struggle, and it chokes back the provision of needed housing units and other services.

re:code LA’s mission is to eliminate this confusion. The project aims not to change zoning designations but to flatten and consolidate the layers of regulation adhering to a particular property into one single zoning designation, with all its requirements and limitations spelled out in an intuitive and uniform way.

The re:code team has outlined the following steps to a successful rewrite of LA’s zoning code:

- Develop an outline for the new zoning code;

- Review and incorporate external material (neighborhood and specific plans, etc.) into the new zoning code;

- Consolidate existing zones and their overlays into base zones;

- Draft new zones to implement future planning (requiring public review and council action);

- Prepare new standards that improve the quality of development; and

- Strategically amend the zoning map (requiring public review and council action).

re:code is piloting this project in the Downtown neighborhood council district. Downtown is already densely built and contains a relatively small residential population, making change in this neighborhood less likely to run afoul of NIMBYism.

With recommendations and analysis in hand, DCP is now developing the redesigned and rewritten code for the Downtown neighborhood. DCP will release the code in the summer or fall of 2015. After that, the revised zoning code will be released in geographic chunks on a rolling basis.

How to get involved: The act of actually changing a zoning designation (rather than simplifying the layers of regulation applying to it and giving it a different name) requires both community input and Council approval. Some of re:code’s work will involve zone changes, although it is their stated goal to limit this. The need for more multilateral approval in those cases may prove difficult.

The Zoning Advisory Committee of the City Planning Commission meets monthly for updates on the process, and these meetings are open to the public. Formal public hearings and virtual and neighborhood forums are also planned. Funding comes from the DCP’s budget as approved by the LA City Council.

San Diego – San Diego Housing Federation

Source: San Diego Housing Federation

Location: Their office is located in downtown San Diego.

What they do: The San Diego Housing Federation is a non-profit advocacy organization, providing resources for low- and middle-income housing in San Diego. They recently advocated successfully for the linkage fee increase, which is basically an added fee of 1.5% of any commercial development costs, with the proceeds going towards low- and middle-income housing. The fee hadn’t been increased since 1996. It’s expected to generate $30 million over the next 20 years to the Affordable Housing Trust Fund. San Diego’s Affordable Housing Trust Fund supports new housing for low- and middle-income households, and maintains existing housing. The San Diego Housing Commission, a public housing organization, administers the Fund.

The San Diego Housing Federation also helped pass Proposition 41, which provided $600 million to help build multi-family housing and provide supportive services to low-income veterans.

How to get involved: They put on an annual affordable housing and community development conference for housing professionals, city officials and residents. Another way to get involved is by participating in one of their many roundtables that bring together local housing professionals to expand their knowledge of low- and middle-income housing in San Diego.

Here’s a sample presentation that outlines some really useful information – applicable in San Diego and the rest of the state – on federal funding for housing programs.

Zoning for long-term housing health

Less restrictive zoning is important to the long-term vitality of your housing market. Builders cannot build if they aren’t allowed to meet rising demand due to outdated regulations. The ultimate result is an unstable housing market, with rents rising well beyond the reach of current residents. The long-term impact can be disastrous for individual communities.

first tuesday will keep you informed of important zoning news in California, but getting involved at your local level is the best way to ensure positive change.

Related topics:

demand, san francisco zoning restrictions, urban living, zoning

Clothesline use may not be barred or unreasonably restricted

Clothesline use may not be barred or unreasonably restricted somebodyPosted by ft Editorial Staff | Nov 30, 2015 | Laws and Regulations, New Laws, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Calif. Civil Code § 1940.20, 4750.10

Added by A.B. 1448

Effective date: January 1, 2016

Homeowners associations (HOA) and landlords may not bar or impose unreasonable restrictions on the use of clotheslines or drying racks in an owner’s or tenant’s backyard or private area.

Balconies, railings, awnings, and other parts of the building do not qualify as clotheslines or drying racks.

A tenant using a clothesline or drying rack needs to:

- obtain the consent of the landlord;

- prevent the clothesline or drying rack from interfering with health, safety and property maintenance; and

- adhere to all reasonable time and location restrictions imposed by landlord.

Restrictions that do not significantly increase the cost of using a clothesline or drying rack are still permitted.

Related topics:

drought, homeowners association (hoa)

Comply with new notary requirements or face rejection

Comply with new notary requirements or face rejection somebodyPosted by ft Editorial Staff | Mar 17, 2015 | New Laws, Your Practice | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Effective January 1, 2015, a new consumer notice is required of all documents requiring a notary certificate in California. The notice needs to be displayed in a box at the top of the certificate, to read:

“A Notary Public or other officer completing this certificate verifies only the identity of the individual who signed the document to which this certificate is attached, and not the truthfulness, accuracy, or validity of that document.” [Calif. Civil Code §1189]

If your document requiring notarization does not adhere to the new requirements, there’s about a 30% chance it will be rejected by the county recorder, according to a recent survey by the Notary Bulletin.

Nearly all of the survey respondents (95%) said they have rejected documents when the consumer notice was simply missing. Other commonly reported reasons for rejection include:

- the consumer notice was in the incorrect location on the form, such as below the signature line (76%); and

- the consumer notice was floating and not anchored in a box separate from the body of the notary certificate (74%).

Less common, though still legitimate, reasons for rejection include:

- the consumer notice was illegible or impossible to read (37%);

- the consumer notice was attached to the recordable document using an adhesive label (16%); and

- the updated language of the consumer notice was manually handwritten onto the face of the document (13%).

There are 58 counties in California, and each interprets the nuances of these new requirements a little differently. Some counties are very stringent and inflexible, such as those who reject a notice that is difficult to read, while others are more accommodating. Thus, the rejection rate across California’s 58 counties is wildly divergent, with some recorders rejecting 30% of documents, and others rejecting as few as 5%.

What’s your best bet to ensure your transaction is not a causality of these new requirements? Get your forms from a trusted source. All first tuesday forms have been updated to comply with the consumer notice requirement. Common forms used in real estate transactions requiring a notary certificate include the:

- Grant Deed [See first tuesday Form 404];

- Deed-in-lieu of Foreclosure [See first tuesday Form 406];

- Request For Notice of Default and Notice of Delinquency By Junior Trust Deed Beneficiary [See first tuesday Form 412];

- Trust Deed and Assignment of Rents Securing a Promissory Note [See first tuesday Form 450]; and

- Notice of Trustee’s Sale [See first tuesday Form 474]

All 26 first tuesday forms containing the new notary certificate may be downloaded at no cost from the View and download new and updated forms tab on the Forms Download page.

Alternatively, if you’re already working on an older, noncompliant form, use the separate first tuesday Form 407, Acknowledgment By Notary Public – Notary Consumer Disclosure, and attach it to any document requiring notarization in lieu of the boilerplate notary acknowledgement. [Calif. CC §1188]

Has your county recorder rejected any of the forms you were trying to record, delaying your transaction? Share your experiences in the comments below!

Related topics:

disclosures, notary

Course provider compliance for CalBRE continuing education

Course provider compliance for CalBRE continuing education somebodyPosted by Sarah Kolvas | Sep 1, 2015 | Laws and Regulations, Licensing and Education, Real Estate | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

How do you find and select your CalBRE continuing education provider?

- Past use (59%, 17 Votes)

- Internet search (21%, 6 Votes)

- Colleague referral (7%, 2 Votes)

- Mailed advertisements (7%, 2 Votes)

- Broker recommendation (3%, 1 Votes)

- E-mailed advertisements (3%, 1 Votes)

Total Voters: 29

Read on so you know how to select a reputable and compliant CalBRE continuing education provider.

The California Bureau of Real Estate (CalBRE) recently released an advisory informing licensees the continuing education provider, The Career Compass, is no longer permitted to offer CalBRE continuing education courses. [See CalBRE Licensee Advisory, August 6, 2015]

The Career Compass violated CalBRE regulations by issuing CalBRE continuing education course completion certificates to licensees without administering final exams – a CalBRE requirement strictly enforced for all course providers. [Calif. Bureau of Real Estate Regulations §§3006(d), 3007.3]

After Career Compass’ accreditation was revoked, it partnered with an approved, third-party course provider, Gold Coast Schools, and continued to violate CalBRE regulations by:

- falsely advertising its courses may be used for CalBRE continuing education credit;

- failing to disclose the course material it offered was approved for and provided by Gold Coast;

- administering exam questions that differed from questions approved for Gold Coast’s material and providing answers before administering the exam;

- claiming that reading the course material was optional, thus failing to ensure licensees devoted the CalBRE-mandated amount of time on reviewing the course material; and

- issuing course completion certificates that named Gold Coast as the provider but were unlawfully signed by a representative from The Career Compass.

The violations resulted in an order from CalBRE for both Career Compass and Gold Coast to cease any marketing that states or implies Career Compass is qualified to provide continuing education to licensees for CalBRE credit or that Career Compass is permitted to act as an instructor for continuing education courses. Gold Coast dropped its affiliation with Career Compass.

More importantly, licensees who took courses through The Career Compass had their continuing education courses rejected when attempting to renew with CalBRE.

Worse, a licensee who receives a course completion certificate without studying and successfully completing an exam or who falsifies information on their renewal application is also subject to disciplinary action by CalBRE. [CalBRE Bulletin, Winter 2014; Calif. Business and Professions Code §§10170.5(d), 10177(a)]

Thus, a licensee’s choice in selecting their continuing education course provider plays an important role in ensuring proper satisfaction of CalBRE renewal requirements.

Editor’s note — As a course provider, first tuesday is also subject to these CalBRE regulations and expects to be held to the same standard by licensees. We encourage licensees to select course providers carefully no matter which course provider they are considering.

Identifying valid course providers

Agents and brokers are required to complete 45 hours of continuing education every four years. To offer the required courses to real estate licensees, course providers first submit their course material to CalBRE for approval. Each approved course provider is issued a four-digit CalBRE continuing education sponsor number identifying them as an approved real estate educator.

Licensees need to look for this sponsor number on advertisements for continuing education courses and provider websites. The absence of the four-digit sponsor number is an indication the course provider is not compliant with CalBRE regulations and likely not authorized to provide courses for CalBRE continuing education credit. [CalBRE Regs. §3007.6(a)(3)]

Upon approval, course providers are subject to well-defined course administration guidelines. This includes ensuring licensees understand the course provider’s policies and continuing education requirements by providing a General Information page prior to enrollment. [CalBRE Regs. §3007(f)]

Licensees are advised to look for this page before enrolling in a course online, as failure to provide this page on the course provider’s website is a violation of CalBRE regulations.

Confirming approved course providers

Want to ensure a course provider is approved by CalBRE before signing up? CalBRE provides real estate licensees a reliable way to search for approved course providers and continuing education on their website. [See CalBRE: Approved Real Estate Education Courses]

The online continuing education search doubles as a way for licensees to both confirm a course provider has CalBRE approval to offer courses and to find approved courses for renewal with topics best suited to the licensee.

To confirm a course provider’s CalBRE approval, licensees may enter a course provider’s name or sponsor number in the search fields. This generates a full list of course offerings approved by CalBRE for that provider.

To search for approved continuing education courses, licensees may tick the check boxes for the types of courses they are seeking. The system will produce a full list of courses from all providers that meet the selected criteria.

Course materials and study time

Upon enrollment, the content and format of a continuing education course are regulated by CalBRE.

When offering a live course, a continuing education course provider needs to ensure licensees are present for at least 90% of the offering time, in addition to the time it takes to complete exams. [CalBRE Regs. §3006(b)]

A correspondence course requires course providers to supply licensees with enough course material to adequately cover 45 hours of education. Also, they are to ensure that licensees devote the required number of hours to reviewing material. [CalBRE Regs. §3006(g)]

Thus, a continuing education course that only provides online material needs to clock a licensee’s study time and reading to ensure they actually complete 45 hours of online education. When books are provided and reading cannot be timed, the course provider still needs to prevent licensees from completing the course sooner than the amount of time CalBRE deems sufficient for the licensee to first review the material and complete quizzes before testing. [CalBRE Regs. §§3006(g), 3007.3(j)]

Noncompliant course providers attempt to bypass these regulations by allowing licensees to review online material without logging in the reading time, or permitting completion of the course before the licensee satisfies all 45 hours, including quizzes. These are some of the violations of CalBRE regulations and are grounds for:

- withdrawal of the course provider’s continuing education approval; and

- denial of a licensee’s renewal application.

Quiz and examination rules

Course providers are required to give licensees incremental assessments, i.e. quizzes, throughout the course to test the licensee’s grasp of the material. Quizzes are mandatory for all licensees. [CalBRE Regs. §3006(p)]

Licensees are then required to pass final exams to receive a valid course certificate. Course providers are only permitted to duplicate up to 10% of the questions used on the quizzes for the exams. Thus, the majority of questions on the exams are mandated to be different from the questions licensees encounter on the quizzes. [CalBRE Regs. §3007.3(l)]

CalBRE imposes stringent guidelines on continuing education course providers to ensure exams:

- are properly timed – no more than one minute per question [CalBRE Regs. §3007.3(f)];

- require a passing score of 70% or more [CalBRE Regs. §3007.3(o)];

- allow a licensee two attempts to pass with two versions of the exam and, when both are failed, require licensees to complete the course hours again [CalBRE Regs. §3007.3(k)];

- only permit a licensee to test on a maximum of fifteen hours of material in a 24-hour period [CalBRE Regs. §3007.3(c)];

- contain a state-mandated minimum number of questions, depending on the number of hours in the course [CalBRE Regs. §3007.3(d)];

- are protected to maintain the integrity of the exams by prohibiting licensees from downloading or printing the exams and automatically timing out after the maximum amount of time has lapsed [CalBRE Regs. §3007(i)]; and

- when administered by a proctor on paper, are monitored by someone who is not related to the licensee by blood, marriage, domestic partnership or other relationship (including work-related) that may influence them to deviate from proper exam administration rules, which the proctor is to certify in writing. [CalBRE Regs. §3007.3(h)]

Thus, licensees need to be aware of any course provider that fails to follow these guidelines by, for example, not administering exams or not timing the licensee’s exams.

Further, licensees who request an exam proctor for paper exams also assume an obligation to conform to CalBRE regulations by only providing a proctor who is not related to them and ensuring their proctor confirms compliance in writing.

Noncompliant course providers

When any continuing education course provider violates the regulations controlling the content of the course or exam administration, CalBRE may revoke the provider’s approval. The withdrawal is effective 30 days after a course provider receives notice of CalBRE’s withdrawal. Thereafter, real estate licensees may no longer submit to CalBRE any courses from that provider completed on or after the effective date of the withdrawal to renew a license. [CalBRE Regs. §3010]

Real estate agents and brokers need to carefully select continuing education course providers and confirm they are approved by CalBRE before enrollment. Course providers who do not properly follow CalBRE regulations put real estate licensees at risk and impact their ability to renew on time with valid continuing education.

Agents and brokers who come across continuing education courses that violate CalBRE regulations may report the course provider by filing a complaint with CalBRE, submitted along with supporting documents. [See CalBRE Form 340: Education Provider Complaint]

CalBRE will investigate the course provider’s continuing education and activities, and later conduct a disciplinary hearing if they discover any violations.

Have you encountered noncompliant and disreputable continuing education course providers? Has your renewal ever been compromised by a course provider that violated CalBRE regulations? Let us know in the comments.

Related topics:

broker, continuing education (ce), department of real estate (dre), sales agent

DOES A SURVIVING SPOUSE’S LIFE ESTATE CONFER OWNERSHIP OF A PROPERTY WHEN THEY OBTAIN A MORTGAGE ON THE PROPERTY?

DOES A SURVIVING SPOUSE’S LIFE ESTATE CONFER OWNERSHIP OF A PROPERTY WHEN THEY OBTAIN A MORTGAGE ON THE PROPERTY? somebodyPosted by Whitney Trang | Aug 3, 2015 | Laws and Regulations, Real Estate, Recent Case Decisions | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Facts: A property owner dies. The property owner’s will grants their spouse a life estate with a power of sale in their separate property, providing the spouse the right to occupy the property for the duration of the spouse’s lifetime. Under the terms of the will, the spouse may sell the property and divide the sale proceeds between the spouse and their two children. Further, if the spouse dies and has not sold the property, it passes to the children. The spouse obtains a mortgage secured by a trust deed on the property. The spouse later dies and the mortgage goes into default. The lender files a Notice of Default (NOD) and attempts to foreclose on the property.

Claim: The property owner’s children seek to cancel the trust deed and quiet title to the property, claiming the lender has no claim to the property after the spouse’s death since the spouse only had a life estate which does not confer ownership of the property.

Counterclaim: The lender seeks to foreclose on the property, claiming the spouse was given fee ownership of the property since they had the ability to sell it.

Holding: A California court of appeals holds the lender may not foreclose on the property and the property owner’s children hold fee ownership of the property free from the lender’s lien since the spouse’s power of sale did not translate into fee ownership of the property and thus upon the spouse’s death the lender is unable to enforce the trust deed. [Peterson v. Wells Fargo Bank, N.A. (May 8, 2015) ___ CA4th ___]

Related topics:

life estate, fee ownership, separate property, notice of default (nod)

DOES SERVICE OF A NOTICE OF DEFAULT TRIGGER THE RUNNING OF THE STATUTE OF LIMITATIONS FOR FILING A QUIET TITLE ACTION?

DOES SERVICE OF A NOTICE OF DEFAULT TRIGGER THE RUNNING OF THE STATUTE OF LIMITATIONS FOR FILING A QUIET TITLE ACTION? somebodyPosted by Whitney Trang | Aug 21, 2015 | Laws and Regulations, Real Estate, Recent Case Decisions | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Facts: The adult child of a commercial property owner forges the owner’s name and obtains a mortgage secured by a trust deed on the property without the owner’s knowledge. The adult child defaults on the mortgage and the property owner receives a Notice of Default (NOD). The owner enters into a forbearance agreement with the lender and agrees to a repayment plan. More than three years after receiving the NOD, the property owner files a quiet title action, but is denied due to the three-year statute of limitations (SOL).

Claim: The property owner seeks cancellation of the trust deed lien by quiet title action, claiming the lien is fraudulent and their quiet title action is not subject to the SOL since the SOL only applies to disputed or disturbed possession, and their possession of the property was not disturbed by the NOD.

Counterclaim: The lender claims the owner may not pursue quiet title action since delivery of the NOD disturbed the owner’s possession of the property and triggered the SOL, which expired before the owner filed the quiet title action.

Holding: A California court of appeals holds the owner’s quiet title action is not barred by the SOL and cancels the forged trust deed lien since an NOD does not dispute or disturb an owner’s possession of property and thus, does not trigger the SOL. [Salazar v Thomas (May 1, 2015) ______ CA4th ______]

Related topics:

notice of default (nod), statute of limitations, quiet title action, commercial real estate, trust deed, forgery

DOES THE HARDSHIP OF REMOVING PATIO FURNITURE GRANT A NEIGHBOR AN EQUITABLE EASEMENT OVER A PROPERTY OWNER’S LAND?

DOES THE HARDSHIP OF REMOVING PATIO FURNITURE GRANT A NEIGHBOR AN EQUITABLE EASEMENT OVER A PROPERTY OWNER’S LAND? somebodyPosted by Whitney Trang | Aug 13, 2015 | Laws and Regulations, Real Estate, Recent Case Decisions | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Facts: A property owner’s neighbor places portable patio furniture on a portion of the owner’s property, believing the portion of property is their own. The owner, aware of the neighbor’s encroachment, allows the neighbor to continue using the land without restrictions. More than three years later, the owner sells their property to a new owner. The new owner is unable to use the portion of their property blocked by the furniture, creating a hardship for them.

Claim: The new owner seeks the removal of the neighbor’s patio furniture, claiming the new owner faces undue hardship and is unable to use their land since the neighbor blocked the new owner’s use with the patio furniture.

Counterclaim: The neighbor seeks an equitable easement over the new owner’s land, claiming they do not have to remove the patio furniture since it is a greater hardship for the neighbor to remove the furniture and they have been using the property for more than three years.

Holding: A California court of appeals holds the neighbor is not entitled to an equitable easement over the new owner’s property and needs to remove the furniture since the hardship experienced by the neighbor to remove their patio furniture from the new owner’s land is not greater than the new owner’s hardship of not being able to use their land. [Shoen v. Zacarias (May 22, 2015) _____CA4th_____]

Related topics:

easement, property dispute, neighbor, balancing equities, balancing hardships, encroachment

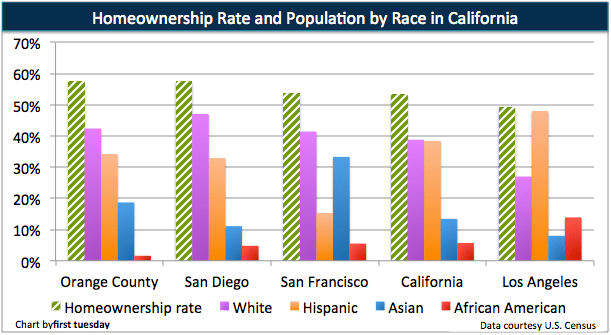

Discrimination harms homeownership

Discrimination harms homeownership somebodyPosted by Carrie B. Reyes | Nov 23, 2015 | Buyers and Sellers, Fair Housing, Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Some facts about the housing market:

- homeowners have more wealth than non-homeowners; and

- white (non-Hispanic) households have a higher homeownership rate than non-white households.