2016

2016 somebody2016 in review and a look ahead to 2017

2016 in review and a look ahead to 2017 somebodyPosted by ft Editorial Staff | Dec 31, 2016 | Feature Articles, Forecasts, Laws and Regulations | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

What do you believe will most influence real estate sales in 2017?

- Interest rates. (64%, 132 Votes)

- Mortgage bankers and lenders. (12%, 24 Votes)

- Buyer-occupants. (10%, 20 Votes)

- Sellers. (7%, 14 Votes)

- Investors. (4%, 8 Votes)

- Builders. (3%, 7 Votes)

Total Voters: 205

California’s real estate market continued on its long path to recovery and expansion in 2016. This article reviews some of the new laws real estate professionals need to be aware of for 2017, trends that took shape in the housing and mortgage markets in 2016 and a forecast for 2017.

New real estate laws in 2016

California real estate law is an ever-changing landscape. Dozens of new laws impacting the real estate profession were passed in 2016, and the most noteworthy laws are included below. To stay up to date on new laws, see first tuesday’s New Laws section.

New, gender-neutral language has made its way into the CalBRE lexicon. Beginning January 1, 2017, a CalBRE sales agent can refer to themselves as either a salesperson, salesman or saleswoman. [Calif. Business and Professions Code §10013]

New identification requirements will be required for real estate advertisements and purchase agreements.

The California legislature has clarified how brokers are to be identified on signs and advertisements requiring a responsible broker’s identity. Effective August 29, 2016, the broker may be identified by the:

- broker’s name under which they are licensed and do business; or

- both the broker’s name and CalBRE license number. [Bus & P C 10159.7]

Beginning January 1, 2018 — which gives real estate professionals a year to update their materials with the new requirements — licensees will need to provide their name, CalBRE license number, Nationwide Mortgage Licensing System (NMLS) ID number, if applicable, and their employing broker’s identity on advertisements and certain other materials. Read more here. [Bus & P C §10140.6]

Of interest to anyone who has been disciplined by the CalBRE, beginning January 1, 2018, CalBRE licensees may petition the CalBRE to remove the licensee’s disciplinary action from CalBRE’s public record’s page if:

- the disciplinary action has been posted for at least ten years;

- the licensee provides the CalBRE with proof they no longer pose a risk to the public; and

- the licensee pays a fee to the CalBRE with the petition, in an amount to be determined by CalBRE Regulations.

All disciplinary actions will remain on record with the CalBRE and continue to be shared with other licensing and regulatory agencies. [Bus & P C §10083.2]

CalBRE-licensed brokers and sales agents renewing their real estate license now need to fulfill an additional course requirement. The new requirement applies to agents and brokers with licenses that:

- expired on or after January 1, 2016; or

- have previously expired and are within the two-year renewal grace period.

These licensees will need to take either a(n):

- three-hour office management and supervision course; or

- eight-hour survey course which includes office management and supervision. [Bus & P C 10170.5]

Editor’s note—All first tuesday 45-hour continuing education (CE) course enrollments automatically include the mandated three hours of office management and supervision.

To stay up to date on changes at the CalBRE, see our CalBRE Watch page.

Legal aspects to watch in 2017

New legislation is introduced throughout the year in the California senate and assembly. Legislation pending at the end of 2017 includes:

- a tax deduction for amounts contributed to an individual’s homeownership savings account and a tax exclusion for interest income earned from money in this type of savings account [A.B. 53];

- the issuance of $3 billion in bonds to finance existing housing programs, infrastructure and affordable housing grant programs [S.B. 3];

- establishing a $75 fee on the recording of every real estate instrument to fund affordable housing developments. [S.B. 2]

To view the full list of pending legislation that may impact your real estate business, see our Pending Laws page.

Further — not a law change, but still important to our readers — the California Association of Realtors (CAR) found itself in hot legal waters in 2016.

PDFfiller, a digital document management company, has filed antitrust allegations against CAR, claiming CAR is guilty of:

- creating a form monopoly;

- unlawfully tying CAR real estate forms to zipForm® software;

- conspiracy in restraint of trade; and

- violating the Cartwright Act and the Sherman Antitrust Act.

This comes after CAR initially sued PDFfiller for copyright and trademark infringement by use and distribution of CAR forms. CAR has long restricted access to its form library to paying members, only. This exclusivity is why many real estate agents think they are required to be members of CAR (some brokers require it of their agents). However, CAR forms are not mandatory to use. In fact, Realty Publications, Inc. (RPI) publishes over 400 real estate forms that are fully legal for use in California. Read more here and search the full library of RPI forms — free to download — here.

At the time of this writing, PDFfiller and CAR were attempting to settle the dispute outside of court. Stay tuned to first tuesday in 2017 for the outcome.

Interest rates rise

The average 30-year fixed rate mortgage (FRM) rate in California rose from its four-year low of 3.37% in October to nearly 4.2% at year’s end. For a homebuyer with an average household income in California, this represents a loss of $37,000 in buyer purchasing power. In other words, buyers are now able to qualify for significantly less mortgage principal — or need to make up the difference with higher mortgage payments.

The 30-year FRM rate was at an all-time low in 2012, when it was 3.25%. It has remained relatively low since then — until the rapid increase experienced at the end of 2016.

Rates remained low for the past four years primarily due to global economic uncertainty. Facing a lack of safe investments elsewhere, U.S. and foreign investors turned to the safety of U.S. Treasuries. All these Treasury purchases kept Treasury rates low, and in turn FRM rates stayed low, too.

What caused the sudden rate increase in November 2016?

The unexpected election of a Republican caused bond market investors to shift their outlook for future interest rates. Rates tend to inch higher under Republican administrations, and the bond market is preparing for this by demanding higher rates now. To a lesser extent, expectations of the Federal Reserve (the Fed) acting to increase interest rates caused rates to rise, too. The Fed increased the target short-term rate from 0.25%-0.5% to 0.5%-0.75% in mid-December 2016 and projects further, gradual increases ahead.

Forecast — FRM rates will continue to rise going into 2017. But long-term rate movement is less certain. The rate increase might slow when the incoming government increases infrastructure spending. It also might slow if economic progress declines. Either way, don’t expect a return to historically low 30-year FRM rates anytime soon.

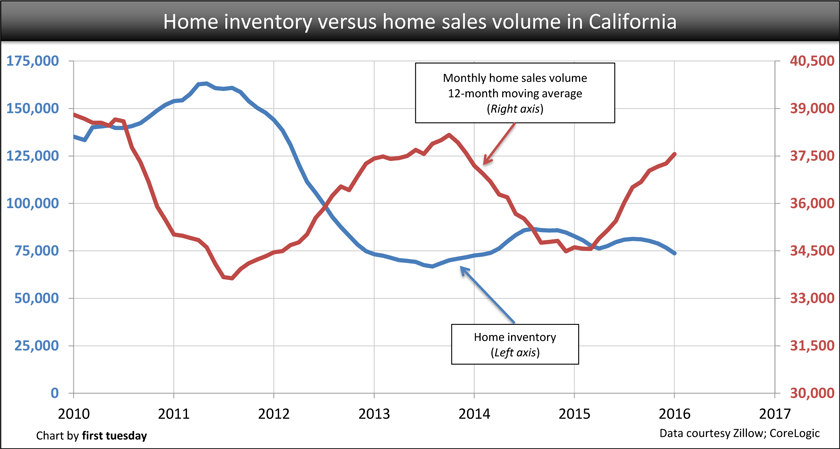

Home sales, prices slow

California year-over-year home sales volume was on an upward trend in 2014 through most of 2015. After year-over-year sales volume peaked at 17% in mid-2015, it reversed direction while still remaining positive through the first half of 2016.

The last few months of 2016 saw fewer home sales than the same time a year earlier. However, since the year started off with a higher (though declining) sales volume than 2015, the sum total of 2016 sales volume was level with 2015.

Home price movement tends to follow sales volume movement within 9-12 months — the delay is due to the “sticky price” phenomenon, when sellers continue to demand yesterday’s prices in today’s market. Therefore, while sales volume began to falter in mid-2015, home prices started to level off in mid-2016.

While fourth quarter (Q4) numbers aren’t in at the time of this writing, in Q3 2016 prices remained 9% higher than a year earlier in low-tier sales, 6% higher than a year earlier in mid-tier sales and 5% higher than a year earlier in high-tier sales.

However, on a month-to-month basis mid- and high-tier prices have displayed little to no upward movement in the second half of this year.

Forecast — When this slowing trend continues, prices will decline below their point a year earlier likely in mid- to late-2017— 9-12 months following the sales volume decline into negative territory.

Ahead for 2017

It’s been over a decade since the housing market went south, with sales volume dropping in 2006 and prices following in 2007. Since then, we’ve been in recession or recovery mode. 2017 will be no exception, and will likely to be another modest year for home sales.

When will the recovery turn into the next housing boom?

Obstacles to a sustainable recovery include:

- deregulation of mortgage lenders;

- rising mortgage rates;

- insufficient residential construction to meet the demand for housing in California’s urban areas; and

- home prices which have increased at a rate far higher than raises in income.

Deregulation of mortgage lenders is likely in 2017 and in the years to follow as the next administration makes its political mark. President-elect Trump has indicated he will take down the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2008, including dismantling the Consumer Financial Protection Bureau (CFPB). If he is successful, agents need to be extra vigilant to protect their clients against the poor lending practices and bad mortgage products that led to the Millennium Boom and bust that occurred following the last era of deregulation.

When mortgage rates continue to rise in the coming years, prices will be pulled down to meet the decrease in buyer purchasing power. For homebuyers desperate to qualify at today’s prices, the price drop will be largely counteracted by higher mortgage rates. Thus, home sales volume will continue to struggle immediately following the rate increase and price decline.

However, some light is on the horizon. California’s jobs recovery continues at a healthy pace going into 2017. We surpassed the number of jobs held prior to the recession in mid-2014. But with the intervening working-aged population increase of 1.2 million individuals, the real jobs recovery won’t take place until around 2019.

At that time, the next generation of first-time homebuyers will have gained enough confidence in the market and savings to make the leap into homeownership. Also at the end of this decade, Baby Boomers will begin to retire en masse, seeking to downsize and buy replacement homes that are more manageable and more centrally located — condominiums will likely receive a surge of interest.

The California legislature and local city councils will need to prepare for the next wave of home sales by allowing residential construction to reach its full potential. Currently, outdated and over-restrictive zoning regulations are keeping builders from responding to homebuyer demand. This is part of the reason why housing costs have outstripped incomes in California’s desirable coastal cities (San Francisco’s housing crisis quickly comes to mind).

Some of this effort is already underway in California, with accessory dwelling units and granny flats having a particularly good year in the 2016 legislature. Expect to see more zoning changes in the coming years to keep housing costs from expanding out of the reach of first-time homebuyers.

Continue to check in with first tuesday throughout the year for a heads up on changes to your real estate practice and California’s constantly shifting housing market.

Related topics:

california home prices, california legislation, california real estate, homes sales volume

Address discrepancy rules for credit reports

Address discrepancy rules for credit reports somebodyPosted by Sarah Kolvas | Jun 20, 2016 | Finance, Laws and Regulations, Real Estate, Your Practice | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

This article discusses the address discrepancy rules which mortgage loan originators (MLOs), mortgage loan brokers (MLBs), landlords and property managers who are subject to credit reporting rules implement on their receipt of an address discrepancy notice.

The address discrepancy rule

To ensure the security of consumer credit report information, the Federal Trade Commission (FTC) enforces an address discrepancy rule. [15 United States Code §1681c(h); 16 Code of Federal Regulations §641.1]

Consumer credit reports are ordered by users and received from credit reporting agencies. The users of consumer credit reports are broken into two classes: those who do and those who do not report on applicants to credit reporting agencies.

A user of consumer credit reports is any individual and business which orders and uses credit reports as a basis for setting the terms of a consumer mortgage or the terms of a residential rental or lease agreement. Credit report users include:

- mortgage loan originators (MLOs);

- mortgage loan brokers (MLBs);

- lenders and banks;

- landlords; and

- property managers. [See RPI Form 202, 302, 550 and 551]

In application, the address discrepancy rule has two separate compliance aspects for users of consumer credit reports:

- confirmation of an applicant’s address; and

- reporting an applicant’s corrected address to credit agencies.

To confirm an applicant’s address, all individuals and businesses using consumer credit reports need to implement office management policies to administratively establish the accuracy of an applicant’s address on their receipt of an address discrepancy notice from a national credit reporting agency (NCRA).

The second aspect of the address rule places a further burden on users who also regularly report credit information to credit agencies. Those users who provide credit agencies with financial information on their clients must also report an applicant’s corrected address to the credit agencies. This aspect of the rule typically only applies to:

- lenders and banks with consumer mortgage portfolios; and

- MLOs who also service consumer mortgages.

The address discrepancy notice

Users who order consumer credit reports receive an address discrepancy notice from a credit reporting agency when an applicant’s address stated on the credit application substantially differs from the address the agency has on file for that applicant. [15 USC §1681c(h)]

The rule does not clarify when an address is considered to “substantially differ” from the address on file, leaving this distinction up to each credit reporting agency to determine when providing address discrepancy notices. Presumably, a submitted address may substantially differ from the address the agency has on file when the address contains a different street number, street name or zip code.

Receipt of a notice subjects the user who ordered the credit report to determine whether the credit report correctly relates to the named buyer or tenant applicant.

Importantly, the rule only applies to address discrepancy notices received by users from the three existing NCRAs — either directly or through a third party acting on their behalf. NCRAs include:

- Experian;

- Equifax; and

- [15 USC §1681a(p)]

Again, the address discrepancy rule only applies to consumer credit reports, thus exempting credit reports for business mortgage lenders and commercial landlords.

However, best practice by anyone relying on a credit report is to first confirm an applicant’s address, whether or not you receive an address discrepancy notice from any credit reporting agency for any type of mortgage or rental. Receipt of the notice indicates an ambiguity exists concerning the applicability of the credit report to the applicant.

Further, address discrepancy notices are red flags an MLO or MLB company evaluates as part of their identity theft prevention protocols.

Responding to address discrepancies

Users of credit reports need to create office management policies to reasonably establish and ensure a credit report relates to their applicant upon receipt of an address discrepancy notice.

Policies to confirm the credit report is for the applicant include:

- verifying the accuracy of the information in the credit report with the applicant themselves; or

- comparing information in the consumer credit report with information the user:

- typically uses as part of their customer identification program to verify an applicant’s identity;

- maintains in its records, such as mortgage applications; and

- obtains from third-party sources, such as the applicant’s real estate agent. [16 CFR §641.1(c)]

Reasonable office management procedures to confirm a credit report properly identifies the applicant ensure the user has correct credit information for that buyer or tenant applicant — preventing them from issuing a mortgage or entering into a rental or lease agreement premised on someone else’s credit information.

When a credit report user determines the report they received does not relate to their applicant, the user then runs the applicant’s information again to pull the correct credit report and resolve any further discrepancies with the applicant.

Rules for users who report credit information

In addition to the above requirements, consumer credit report users who regularly report information to credit agencies are subject to address reporting requirements.

A user who confirms an applicant’s address is different than the one given in the consumer credit report which prompted the discrepancy only needs to submit the correct address to the credit reporting agency that issued the notice when:

- the credit reporting agency is an NCRA (or a third party acting on behalf of one);

- the user holds a reasonable belief the credit report is that of the identified applicant;

- the user establishes a continuing relationship with the applicant; and

- the user regularly furnishes information to the credit reporting agency in the ordinary course of business. [16 CFR §641.1(d)(1)]

Editor’s note — The requirement to report a correct address will most often apply to lenders and banks, not property managers, landlords or MLOs and MLBs who merely originate mortgages. However, an MLB who services mortgages and regularly reports a homebuyer’s credit information will need to include the corrected address in the information they report.

Office management policies set by a user (who reports) for confirming a consumer’s address and providing a corrected address to credit reporting agencies include:

- verifying the address with the applicant;

- reviewing their own records they have on the applicant; or

- other reasonable means. [16 CFR §641.1(d)(2)]

The user who reports to credit reporting agencies submits a confirmed address as part of the information they regularly provide to those agencies on an applicant (e.g., a buyer’s credit limit, delinquencies and late payments).

Following these procedures under the address discrepancy rule enhances the accuracy of credit reports used by all, and further ensures an MLO, MLB, landlord or property manager is alerted when they do not have the correct credit report for an applicant.

Noncompliance penalties

Credit report users for consumer mortgages and residential tenancies who do not comply with address discrepancy rules are subject to action by the FTC. The maximum penalty that may be recovered by the FTC is $3,500 per violation. [15 USC §1681s(a)(2)(A); 17 CFR §1.98]

The FTC also has the authority to:

- investigate the person or business in violation;

- enforce compliance through issuing procedural rules to be adopted for detecting suspicious activity; and

- require the filing of reports, the production of documents and the appearance of witnesses. [15 USC §1681s(a)(a)]

Credit report users are also exposed to litigation from the Consumer Financial Protection Bureau (CFPB), state government and consumers.

Related topics:

consumer protection, federal trade commission (ftc), landlords, mortgage origination, property manager, tenants

Air quality in the San Joaquin Valley

Air quality in the San Joaquin Valley somebodyPosted by Carrie B. Reyes | May 23, 2016 | Bakersfield-Fresno, Buyers and Sellers, Feature Articles | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

This article analyzes the problems poor air quality causes for residents of the San Joaquin Valley and describes the critical rules residents and real estate agents need to be aware of to mitigate the deleterious effects of air pollution.

The proverbial armpit of California

What region of California comes to mind when you envision an undesirable area wreaked by the ill-effects of a poor climate? Let us paint the scene for you.

The San Joaquin Valley starts south of Sacramento, encompassing Stockton and Modesto, and stretches south to Modesto, Fresno, Visalia and Bakersfield. The San Joaquin Valley bears the unpleasant moniker of “the armpit of California” due to the way the air collects pollution from other parts of the state and stagnates (with the smell of livestock) in the Valley. Further, its hot, dusty climate is a far cry from the pleasantness of nearby coastal climates with greater circulation.

The Sierra-Nevadas are the geographic issue which causes much of the Valley’s climate problems. Mountains stop wind from reaching the region, which causes pollution and dust to become stale, confining all the bad air so that it accumulates and becomes stifling.

Image courtesy U.S. Environmental Protection Agency (EPA)

The American Lung Association ranks the top metropolitan areas with the highest level of air particle pollution. The top seven in the nation are in California, most in the Valley:

- Bakersfield;

- Visalia-Porterville-Hanford;

- Fresno-Madera;

- Los Angeles-Long Beach;

- El Centro; and

- San Jose-San Francisco-Oakland and Modesto-Merced both tied for sixth.

The American Lung Association estimates 70% of Californians live in designated poor air quality areas. (The only cities in California with high-ranked air quality are Salinas and Redding.)

Aside from being unpleasant, the Valley’s poor air quality can cause Valley Fever — coccidioidomycosis — which the Center for Disease Control (CDC) claims is endemic in the Valley. This fever is caused by fungus in the soil getting trapped in the air and inhaled by residents. It can cause pneumonia and is especially dangerous for seniors. The CDC estimates 200 or fewer deaths occur per year in the U.S. due to Valley Fever.

In Bakersfield of Kern County, which has the dubious distinction of having the most polluted air in the country, 9% of children have diagnosed asthma, slightly higher than the national average. 8% of adults have asthma, also slightly higher than the national average, according to the CDC.

In addition to Valley Fever and asthma, poor air quality can cause:

- lung cancer;

- heart attack;

- stroke;

- reduced breathing capacity; and

- other respiratory illnesses.

Improving air quality

The good news is the Valley’s air quality is better today than in recent decades. For example:

- in Kern County, there are on average 73 fewer high ozone (smog) days and 25 fewer high particle pollution days each year compared to 2000;

- in Fresno and Madera, there are 68 fewer high ozone days and 27 fewer high particle pollution days each year compared to 2000; and

- Modesto-Merced sees 36 fewer high ozone days per year, but particle pollution has increased by 15 days per year compared to 2000, according to the American Lung Association.

Even after these improvements, the Valley is still by all accounts the worst region in the U.S. for air quality. Lower than average home values are also the norm here, though it’s difficult to prove the region’s poor air quality is the cause.

Wood-burning rules in the Valley

Despite its reputation, it’s not all gloom and doom for the San Joaquin Valley. Today’s (slightly) better air quality comes thanks to:

- a reduction in vehicle emissions;

- increased use of renewable energy; and

- local laws against wood burning.

Households residing in the San Joaquin Valley Air Pollution Control District are subject to Rule 4901, which bans wood burning in areas below 3,000 feet elevation and with access to natural gas service. To check if your client resides in the air district, look up the zip code at the California Environment Protection Agency’s (EPA’s) website.

This rule took effect in 2003, and has significantly improved air and life quality for residents in the winter months, when air particle pollution is at its worst. A Fresno State study finds this rule has not only decreased health suffering due to air pollution, but has also had a positive economic effect. Residents now spend cumulatively less on healthcare associated with lung diseases to the tune of hundreds of millions of dollars a year — savings which percolate back into the local community.

Pursuant to Rule 4901, sellers of real estate in San Joaquin Valley need to ensure any woodstoves or fireplace inserts are EPA Phase II certified. These certified appliances are identified by a permanent, metal label on the back or side. Any non-certified woodstove or fireplace insert needs to be removed from the property or, if it is decorative, made inoperable. [See Wood-Burning Heater Statement of Compliance]

In Kern County, developers may not install wood burning fireplaces in new subdivisions consisting of 10 or more dwellings. [See Rule 416.1]

Further, residential water heaters may not be installed in Kern County unless they are certified to meet the American National Standard. [See Rule 424-1]

What residents can do

If you live in an area with poor air quality, follow these tips to help improve the air you breathe:

- Pay attention to air pollution levels, which change on a daily basis. Enter your zip code at AirNow.gov to find out your area’s air quality today. On bad air days, stay inside.

- Don’t burn wood or trash, as this creates air particle pollution. While dust masks block large particles, they don’t protect against dangerous smoke particles and gases. If you have a wood-burning appliance, switch to gas or pellets. If you must burn wood, then ensure it is dry.

- Avoid spending time along busy roads during periods of heavy traffic, since vehicle exhaust is worse in these areas.

- Set your air conditioning to “recirculate” as this does not pull in air from outdoors. If you have a whole house or attic fan, only operate it on good air quality days.

- If you develop symptoms such as consistent cough, irritated eyes, shortness of breath, itchy throat, headaches or frequent sinus infections, visit your doctor.

Related topics:

drought, environmental law

All-cash sales of high-end homes need to be reported in major California counties

All-cash sales of high-end homes need to be reported in major California counties somebodyPosted by Carrie B. Reyes | Aug 15, 2016 | Buyers and Sellers, New Laws | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

In an attempt to quell money laundering in several U.S. cities, the Financial Crimes Enforcement Network (FinCEN), part of the U.S. Department of Treasury, will temporarily require title insurance companies to report the identities of people using all-cash to purchase high-end homes.

Title insurance companies will need to report these types of transactions beginning August 28, 2016, and — unless the order is extended — will continue to report through February 23, 2017.

The affected counties include three in New York, Florida and Texas, as well as the following expensive California counties:

- Los Angeles;

- San Diego;

- San Francisco;

- San Mateo; and

- Santa Clara.

In California, all-cash sales of $2 million or more need to be reported.

The requirement’s goal is to reveal the people behind “shell companies” who use large amounts of cash to purchase real estate. These shell companies might be legal, but they also might be hiding funds obtained illegally, which is what the FinCEN is interested in.

For instance, when purchasing a property through a limited liability company (LLC), the bank only requires the account holder of the LLC to be identified. Others with ownership interests in the LLC are of no interest to the bank. This dynamic makes an LLC a perfect place to park and hide money anonymously.

The reporting requirement was issued earlier this year, originally limited to counties in New York and Florida. But the success of the data collected so far has led the FinCEN to believe they will catch more financial criminals in other all-cash hotspots, like upscale coastal California. This also follows crackdowns by the Internal Revenue Service (IRS) on those with ownership in LLCs.

The title insurance company will use FinCEN Form 8300, Report of Cash Payments Over $10,000 Received in a Trade or Business, to report the sale within 30 days of the transaction closing. The title insurance company will file Form 8300 using the Bank Secrecy Act E-filing system.

For most California real estate brokers and agents, it’s business as usual. The new requirement will impact very few transactions, since it is limited to very high-end properties and only to those buyers using all-cash. However, for those active in those markets, be sure to advise your affected clients to this increased scrutiny.

Questions? Read the full order here.

Related topics:

all-cash buyers, cash buyer, limited liability company (llc)

Arbitration in real estate contracts: Will you sign away your right to your day in court?

Arbitration in real estate contracts: Will you sign away your right to your day in court? somebodyPosted by Carrie B. Reyes | May 2, 2016 | Buyers and Sellers, Feature Articles | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Have any of your real estate clients refused to initial the arbitration provision found in many purchase agreements?

- Yes. (59%, 26 Votes)

- No. (41%, 18 Votes)

Total Voters: 44

Arbitration: the good and bad

When a dispute arises in a real estate transaction, instead of taking it to court, the people involved may grant an arbitrator the authority to hear and resolve their dispute.

Arbitration is less costly and quicker than allowing the dispute to go to court. It’s also the form of dispute resolution most consumers agree to abide by at some point or another — including in most real estate transactions. However, there are some major disadvantages:

- Binding arbitration — the type of arbitration included in a provision of the purchase agreement published by the California Association of Realtors (CAR) — requires the buyer and seller to give up their rights to a trial by jury and prohibits them from appealing the arbitrator’s decision.

- The arbitrator’s award is final, even if there was an egregious error or if they applied the law incorrectly. [Hall Superior Court (1993) 18 CA4th 427]

- The arbitrator does not need to apply legal precedent, thus their final decision is unpredictable, or “arbitrary.”

- The arbitration proceedings are not required to be published like court cases, thus it’s impossible for an outsider to know when disputes are decided fairly, or whether their assigned arbitrator is likely to be fair.

- Arbitrators are not required to be unbiased or lack connections to an individual in the case, as many arbitrated disputes have assigned an arbitrator who is a long-time friend or acquaintance of one of the individuals in the dispute.

- The arbitration provision is still enforceable as a separate agreement, even if the purchase agreement is unenforceable. [Prima Paint Corporation Flood & Conklin Mfg. Co. (1967) 388 US 395]

However, many homebuyers and sellers — and even some agents — assume they need to initial the arbitration provision in order to submit the purchase agreement. But this is not true.

Don’t initial that arbitration provision

As a matter of policy, Realty Publication, Inc. (RPI) forms do not contain boilerplate arbitration provisions. But when you are faced with an arbitration provision elsewhere — most commonly found in CAR’s forms, as well as credit card, auto and medical agreements — you are more than justified to steer clear.

The Consumer Financial Protection Bureau (CFPB), the watchdog standing between consumers and any potentially malicious financial systems, found most consumers have no idea what arbitration is, despite agreeing to arbitration agreement at one time or another.

The New York Times refers to arbitration agreements as “get out of jail free” cards for large corporations, since individuals can’t combine resources to bring a corporation to court for a fair hearing. This “opting out” of the legal system is rarely in the best interest of the consumer who has been wronged.

That’s because large arbitration companies are inherently biased, as they need to stay in business. To do this, they need to keep the businesses for which they arbitrate happy, since businesses are more likely than the individual to need to hire an arbitrator in the future. In other words, deciding in favor of big companies is always in the arbitrator’s best interest — never in the best interest of the consumer.

Next steps

If you’re convinced arbitration is the wrong approach to settle real estate disputes, consider informing clients about the risks of arbitration, before they agree to it. Download Client Q&A: What is arbitration? to distribute to clients prior to signing a purchase agreement that may include the provision.

Explaining the arbitration provision to clients does not constitute an unauthorized practice of law. In fact, it’s the agent’s duty to fully explain transaction details to their client. This includes informing them of the potential consequences of agreeing to arbitration.

Likewise, consider only using real estate forms which do not include the arbitration provision. RPI forms include a mediation provision for settling disputes. Unlike arbitration, clients who undergo mediation may later take the case to court if the dispute is not resolved to their liking. [See RPI Form 150]

first tuesday readers can download RPI forms, which are legal to use in California real estate transactions, for free here.

As a point of law, arbitration provisions are not included in trust deeds, consumer mortgage agreements or rental or lease agreements. [12 Code of Federal Regulations §1026.36(h)]

So why should your clients’ purchase agreements include such a provision?

For more reading on arbitration, see: Arbitration, explained.

Related topics:

arbitration, arbitration provision, legal advice

Are mortgage holders monetarily liable for failure to notify a borrower of their mortgage transfer when the transfer occurred prior to the implementation of a notification requirement?

Are mortgage holders monetarily liable for failure to notify a borrower of their mortgage transfer when the transfer occurred prior to the implementation of a notification requirement? somebodyPosted by Amy Thomas | Feb 8, 2016 | Laws and Regulations, Recent Case Decisions | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Talaie v. Wells Fargo Bank, NA

Facts: A mortgage holder transfers a borrower’s mortgage to a successor mortgage holder. Neither mortgage holder notifies the borrower of the transfer. Three years later, a statutory amendment is established requiring mortgage holders to notify borrowers within 30 days of the transfer of their mortgages, or they may be monetarily liable to the borrower.

Claim: The borrower seeks punitive damages from both mortgage holders, claiming they are liable for failing to notify the borrower of the mortgage transfer according to the statute since they did not notify the borrower within 30 days of the mortgage transfer.

Counterclaim: The mortgage holders claim they are not liable for failure to notify the borrower of the mortgage transfer and do not owe the borrower punitive damages since the statute was implemented after the transfer occurred, thus they were not required to notify the borrower of the transfer as it predated the requirement.

Holding: The United States court of appeals holds the mortgage holders are not liable for failure to notify the borrower of the mortgage transfer and do not owe the borrower punitive damages since the statute was implemented after the transfer occurred and the requirement does not apply retroactively. [Talaie v. Wells Fargo Bank, NA (December 14, 2015) ____ F3d ____]

Related topics:

assignment, truth in lending act (tila)

CFPB increases foreclosure protections

CFPB increases foreclosure protections somebodyPosted by Carrie B. Reyes | Nov 17, 2016 | Mortgages, New Laws | 2

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

The Consumer Financial Protection Bureau (CFPB) has released new rules for mortgage servicers to follow when responding to mortgage delinquencies and pursuing foreclosure.

- Beginning October 19, 2017, mortgage servicers are to offer homeowners foreclosure protections more than once if the need for protection arises numerous times.

For instance, consider a homeowner unable to make their mortgage payments who submits a complete loss mitigation application and receives a permanent mortgage modification. The homeowner brings the mortgage current. A few months later, they suffer another, unrelated hardship like a job loss or medical emergency, and face foreclosure again. The servicer is required to offer the same protections that were discussed in the first instance, including evaluating options to avoid foreclosure with the owner.

- Beginning April 19, 2018, mortgage servicers are to extend foreclosure protections to surviving family members or heirs — known as successors in interest — upon the death of the homeowner.

Currently, the term successor in interest is somewhat ambiguous. This new rule defines a successor in interest as a person who receives property after the death of a family member or joint tenant, due to a divorce or legal separation, through certain trusts or from a spouse of parent. In defining this term, the CFPB makes certain that the same foreclosure protections granted the original homeowner pass on to the successor in interest.

- Beginning April 19, 2018, mortgage servicers are to provide more information to homeowners in bankruptcy.

Under the new rules, mortgage servicers need to provide periodic statements to homeowners in bankruptcy. These statements are to include information specific to homeowners in bankruptcy, including information about loss mitigation options. Previously, servicers did not have to provide early loss mitigation information to homeowners who asked them to stop contacting them under the Fair Debt Collection Practices Act, but they will now be required to contact them with early loss mitigation notices.

- Beginning October 19, 2017, mortgage servicers are to notify homeowners promptly when their loss mitigation applications are complete. Previously, owners were not always kept appraised of the status of their applications.

- Beginning October 19, 2017, mortgage servicers are to provide additional protections when transferring mortgage servicing of the mortgage of a homeowner pursuing loss mitigation.

When a homeowner pursuing loss mitigation has their mortgage service transferred, the new servicer needs to follow the same timeframe established by the previous servicer for the loss mitigation process. When the homeowner applies for loss mitigation shortly before a transfer, the new servicer needs to send an acknowledgement to the homeowner that their loss mitigation application was received within 10 business days of transfer. When the homeowner’s loss mitigation application is complete before the transfer, the new servicer has 30 days to evaluate and respond.

- Beginning October 19, 2017, mortgage servicers are to take aggressive measures to avoid dual-track foreclosures.

Under current law, servicers are not allowed to simultaneously pursue foreclosure while evaluating a homeowner for loss mitigation. However, some servicers do not take adequate measures to delay foreclosure proceedings after receiving a complete loss mitigation application before the required 37 days prior to the scheduled foreclosure sale. The CFPB clarifies that even if the servicer has delivered the first foreclosure notice, they are to halt foreclosure proceedings while evaluating a complete loss mitigation application.

- Beginning October 19, 2017, the homeowner’s date of delinquency is to be clarified in the context of mortgage servicing.

Servicers currently are unclear on when a homeowner becomes delinquent, which becomes particularly confusing when a homeowner misses a payment and later pays it, only to miss another. This rule clarifies a delinquency begins on the date a homeowner’s periodic payment becomes due and unpaid. When a homeowner later makes a late payment, it is applied to the oldest missed payment and the date of the delinquency advances to that date.

Too late for foreclosed homeowners

These new rules change little about the foreclosure process and will not apply retroactively, so don’t expect these changes to make any headlines in the real estate world.

Further, these small changes do little to help the millions of people who were foreclosed upon during the 2008 recession and ensuing extended recovery.

The nationwide foreclosure inventory was at its lowest in over eight years in mid-2016 at just 1%, according to CoreLogic. It’s even lower in California, where only 0.4% of all mortgaged homes were in some stage of foreclosure in mid-2016.

With the foreclosure crisis definitively over, foreclosures will continue to decline as long as home prices continue to rise, lifting negative equity homeowners above water. This will continue until around late-2017, when the impact of higher mortgage interest rates will catch up with homebuyers and sellers and prices will begin to decline. In 2018, we may see a spurt of foreclosures as underwater homeowners throw in the towel and decide to default to get out from under their black hole assets. But — lacking a nationwide recession — this uptick in foreclosures will likely be shallow and brief.

Finally, with a new presidential administration in power, calls for a curtailing of the CFPB have been frequent from members of the Republican party who want to see less government intervention in the financial world. Some have called for the CFPB to stop making new rules immediately in preparation for the changes to take place once President-elect Trump takes office and appoints a new director to the organization — if the organization is to exist at all under Trump’s tenure. Thus, keep an eye on the CFPB in the coming months, as big changes are ahead.

See the full rule here. Or, view the CFPB’s brief explanation of the new rule here.

Related topics:

consumer financial protection bureau (cfpb), foreclosure, mortgage delinquency

CID unit owners and annual address updates

CID unit owners and annual address updates somebodyPosted by Giang Hoang-Burdette | Nov 29, 2016 | New Laws, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Calif. Civil Code §4041

Added by S.B. 918

Effective date: January 1, 2017

A common interest development (CID) unit owner is required to provide to their homeowners’ association (HOA) an annual written notice of:

- primary and alternate addresses for receiving HOA notices;

- the name of any legal representatives who can be contacted in lieu of the CID unit owner in the event of the CID unit owner’s extended absence; and

- whether the CID unit is owner-occupied, rented, developed but vacant or undeveloped.

An HOA will request this information from each CID unit owner at least 30 days prior to releasing its annual budget report.

If the CID unit owner does not provide an address for receiving HOA notices, the HOA may meet its notice requirements by sending notices to the CID unit.

Read more:

Related topics:

homeowners’ association (hoa)

CalBRE reinforces license requirement for short-term rentals

CalBRE reinforces license requirement for short-term rentals somebodyPosted by Sarah Kolvas | May 23, 2016 | Laws and Regulations, Real Estate, Your Practice | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

A clarification of licensure requirements for paid property services and vacation rental activities was recently published as a licensee advisory by the California Bureau of Real Estate (CalBRE).

The advisory is the CalBRE’s response to complaints against sales agents and unlicensed individuals attempting to apply the “transient occupancy” exemption from real estate licensing to perform rental activities requiring a license.

When is a license required for property management?

An individual or corporation is required to hold a broker license when they perform any of the following services on behalf of another in exchange for a fee:

- listing real estate for rent or lease;

- marketing the property to locate prospective tenants;

- listing prospective tenants for the rental or lease of real estate;

- locating property to rent or lease;

- selling, buying or exchanging existing leasehold interests in real estate;

- managing income-producing properties; or

- collecting rents from tenants of real estate. [Calif. Business and Professions Code §10131(b)]

A licensed sales agent may also perform the above property management activities. However, they are required to be employed and supervised by a licensed broker. [Bus & P C §10132]

As always, real estate sales agents may never act or market themselves as independent agents, whether they are representing a seller or buyer in a sales transaction, referring or acting as a mortgage loan originator (MLO), or performing property management services.

While a broker license is required when performing property management services on behalf of an owner, a broker license is not required of anyone who manages their own rental property.

Importantly for this discussion, CalBRE broker licensure requirements do not apply to:

- a manager of a hotel, motel or auto and trailer park;

- a resident manager of an apartment building or complex;

- employees of a resident manager;

- a person or company that arranges transient occupancies; and

- an employee of a property management company who is supervised by a licensed broker or their licensed sales agent when they:

- show rental units and common areas to prospective tenants;

- provide and accept preprinted rental applications;

- respond to inquiries from prospective tenants about an application;

- accept security deposits, rents and deposits or fees for credit checks and administrative costs;

- provide information about rental rates and terms of a lease or rental agreement;

- accept signed lease and rental agreements from prospective tenants. [Bus & P C §10131.01(a)]

Short-term rental exemption

The “transient occupancy” licensing exemption — the focus of the CalBRE’s recent advisory — does not require a broker license for property managers of short-term occupancies, erroneously also called vacation rentals, in:

- single family residences (SFRs);

- common interest developments (CIDs); or

- apartment units. [Bus & P C §10131.01(a)]

A residential occupancy is a short-term stay, not a rental at all, when the total period of occupancy is for a term of 30 days or less. As a transient occupant, called a guest, the occupancy is subject to the collection, payment and accounting for local occupancy taxes for the stay. [Calif. Civil Code §1940]

The CalBRE reports some unscrupulous sales agents and unlicensed individuals are attempting to use the short-term transient occupancy exemption:

- to enter into property management agreements; and

- manage properties with rental terms longer than 30 days.

All this conduct is done under the guise of a short-term rental — a clear violation of California’s Real Estate Laws.

To best get a sense of the distinction between a rental and a transient occupancy, transient occupants are not tenants and do not rent; they are guests. They check in and check out, and their occupancy is called a stay, never a tenancy which is a rental of any type. Unlike tenants, transient occupants are not evicted since they do not hold a tenancy estate. Rather, the key is changed, they are locked out or the police remove the occupant after the day and hour of check out. [See RPI Forms 592, 593 and 594]

Rental agreements using the language of “short-term rental” do not establish a transient occupancy. Worse, they do not meet the transient occupant exemption’s guidelines when the occupant intends to remain in the premises for longer than 30 days. Thus, property management services for properties rented under these agreements require a broker license.

Penalties for violations

Violations of California’s Real Estate Law expose both unlicensed property managers and the property owners who compensate them to monetary liabilities.

Unlicensed individuals and sales agents who perform property management services without broker supervision are subject to:

- a fine of up to $20,000; and/or

- imprisonment in a county jail for up to six months. [Bus & P C §10139]

Unlicensed corporations performing property management services are subject to a fine of up to $60,000. [Bus & P C §10139]

Property owners who compensate unlicensed and unsupervised individuals are also subject to a fine of up to $100 per offense. [Bus & P C §10138]

In addition to state fines, independent sales agents who perform property management services without an employing broker are also subject to administrative discipline by the CalBRE, such as license suspension or revocation. [Bus & P C §10138]

The CalBRE notes it is open to receiving complaints against unlicensed property management activities and will carefully investigate claims of licensure exemption to ensure property managers meet exemption rules or are adequately licensed.

Related topics:

broker license, department of real estate (dre), real estate license

California Bureau of Real Estate (CalBRE) broker-associate employment to be public record

California Bureau of Real Estate (CalBRE) broker-associate employment to be public record somebodyPosted by Giang Hoang-Burdette | Nov 8, 2016 | Feature Articles, Licensing and Education, New Laws, Real Estate | 3

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Calif. Business and Professions Code §§10083.2, 10161.8

Amended by A.B. 2330

Effective date: January 1, 2018

Beginning January 1, 2018, an associate-broker’s California Bureau of Real Estate (CalBRE) public record will identify their employing broker(s).

Employing brokers will need to notify the Real Estate Commissioner in writing when they commence or terminate employment of a broker-associate, as they currently are required to do for salespersons.

Read more:

Read the bill text.

Related articles:

Related topics:

broker, broker associate, department of real estate (dre), real estate commissioner

California mortgage and foreclosure rights for successors

California mortgage and foreclosure rights for successors somebodyPosted by Giang Hoang-Burdette | Nov 21, 2016 | Mortgages, New Laws | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Calif. Civil Code §2920.7

Added by S.B. 1150

Effective date: January 1, 2017

This new law applies to successors, defined as natural persons who:

- are the spouse, domestic partner, joint tenant, parent, grandparent, adult child, adult grandchild or adult sibling of a deceased owner of a one-to-four unit principal residence;

- continuously occupied the property within the six months prior to the owner’s death;

- currently occupy the property; and

- are not in a legal dispute regarding the property.

This new law does not apply to federally chartered or state-chartered banks that foreclosed on 175 or fewer one-to-four unit California residential properties during the last reporting year.

Before a mortgage servicer may record a notice of default (NOD) on a one-to-four unit principal residence after being notified of the owner’s death by a non-borrowing successor, the mortgage servicer needs to:

- make a written request for proof of the owner’s death and provide at least 30 days for receipt of the proof; and

- make a written request for proof of the successor’s ownership interest and provide at least 90 days for receipt of the proof.

Proof of the successor’s ownership interest may be:

- probate letters, e.g., letters of administration;

- the deceased owner’s will or trust document;

- a revocable transfer on death deed;

- an affidavit of death of joint tenant;

- an affidavit of death of a spouse from a surviving spouse when the property was held as community property;

- a deed from a surviving spouse showing the residence was community property with the right of survivorship; or

- a certification of trust or other trust documents.

Within ten days of receiving the requested proof and determining the successor’s validity, the mortgage servicer needs to provide to the successor information about the mortgage, including the:

- principal balance;

- interest rate;

- interest rate reset dates and amounts;

- balloon payment amount, if any;

- prepayment penalties, if any;

- delinquency status, if applicable;

- monthly payment amount; and

- payoff amount.

The successor retains the deceased owner’s right to:

- all notices and timelines established by foreclosure laws;

- a single point of contact during the foreclosure process;

- foreclosure alternatives; and

- halt the foreclosure and/or pursue the servicer or lender for material violations of laws governing the foreclosure process.

The mortgage servicer will allow the successor to:

- apply to assume the deceased owner’s mortgage; and/or

- apply for a foreclosure alternative offered by the mortgage servicer.

When multiple successors exist, any successors who do not want to assume the mortgage must give written consent to the assumption by the assuming successor(s).

The mortgage servicer may evaluate the successor’s creditworthiness when determining whether to grant the assumption or foreclosure alternative. The mortgage servicer is not obligated to approve the assumption or foreclosure alternative.

These rules sunset on January 1, 2020.

Read more:

Related article:

Related topics:

assumption, death, foreclosure, notice of default (nod)

California real estate and the PATH Act — what you need to know

California real estate and the PATH Act — what you need to know somebodyPosted by ft Editorial Staff | Apr 25, 2016 | New Laws, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

There’s a reason why you probably haven’t heard about the Protecting Americans from Tax Hikes (PATH) Act — its effect on California real estate is almost trivial. While the PATH Act is mostly a giveaway to stock brokers, foreign investors and underwater homeowners who might benefit from changes to tax policy, savvy real estate brokers and agents with an ear to the ground may be able to exploit the law’s milder provisions.

For a small number of real estate owners and investors, the PATH Act provides marginal tax benefits in 2016, including:

- extended relief for underwater homeowners with recourse mortgages from discharge-of- indebtedness income taxes on short sales; and

- investment incentives for foreign investors in real estate investment trusts (REITs).

Discharge-of-indebtedness income on short sales

The amount of debt forgiven on the short sale of a principal residence is generally taxable as discharge-of-indebtedness income — also called phantom income since the seller receives no net benefit — unless the mortgage is a nonrecourse debt. Debt forgiven on a nonrecourse debt is not taxable as discharge-of-indebtedness income. [Code of Federal Regulations §1.1001-2(a)(2)]

Under the PATH Act, phantom income realized on recourse mortgages through the 2016 tax year is now excluded from a homeowner’s federal taxable income. Debt discharged after 2016 will also be excluded from income if the short sale purchase agreement was entered into in 2016.

Mortgage holders advocate for the punishment of delinquent homeowners who rely on the short sale remedy. The lending industry pushes struggling homeowners through a variety of hoops to rectify their inability to pay their mortgage. This is a moral consequence that is deeply ingrained in the world of lending. With the exclusion of phantom income from a homeowner’s tax bill, there is one less obstacle for getting rid of a negative equity home.

However, the PATH Act only provides federal tax relief to short sellers with discharge-of-indebtedness income on recourse mortgages. The California Franchise Tax Board (FTB)’s favorable tax treatment of forgiven recourse mortgage debt expired on January 1, 2014. [Calif. Revenue and Taxation Code §17144.5]

California’s laws will conform to federal guidelines when Senate Bill 907 works its way through the state legislature.

Related article

Investment by foreigners incentivized

Whereas the poem at the base of the Statue of Liberty proclaims, “give me your tired, your poor, your huddled masses yearning to breathe free,” the foreign investor provision of the PATH Act can be best summarized with the words “give me your wealthy, your skilled, your eager to spend.”

Foreign investors may now own up to 10% of a publicly traded real estate investment trust (REIT) without the REIT being adversely taxed. Previously, REITs were penalized when selling shares to foreign owners exceeding 5% of the value of the REIT.

Making REIT ownership more widely available to foreign money allows overseas funds to flow into REITs instead of direct ownership of real estate, stocks, bonds or deposits with the Federal Reserve (the Fed). More funds will then be available for REITs to pay even more for what has become a rather fixed supply of improved real estate – unless they take to building new projects.

Related article

REIT investment: playing the real estate game from the sidelines

This provision of the PATH Act is a kickback to REIT managers and stock brokers. The federal government is stoking the fire of artificial demand with no regard for the health of the economy when the sources of these “hot money” funds disappear (as they always do and inevitably will).

PATH Act footprints?

Despite the hoopla attendant with all politically induced schemes, these provisions will have only a moderate and temporary effect on sales volume, pricing and tax consequences for participants in California real estate transactions. Further, government subsidies for recession recoveries do end. To the extent real estate licensees depend on the transactions generated by these programs, they need to have an exit plan into other types of sustainable transactions before the subsidies run their course.

While government incentives temporarily increase sales volume, they do nothing to stimulate organic end user demand. Further, mortgage rates will rise, probably by late 2016. Thus, expect any sales volume boost from these incentives to fall off with prices following within 12 months.

Real estate agents and brokers know inert and static pricing means the death to sales volume, and thus fees. Those able to understand and exploit the volatility in demand created by tax policy will be able to ride the wave before benefits expire and foreign money dries up, and conditions crash back to a normal pace.

Related topics:

underwater

Case in point: When a buyer and seller are represented by different agents employed by the same broker, does the seller’s agent owe a fiduciary duty to the buyer?

Case in point: When a buyer and seller are represented by different agents employed by the same broker, does the seller’s agent owe a fiduciary duty to the buyer? somebodyPosted by Connor P. Wallmark | Nov 30, 2016 | Laws and Regulations, Real Estate, Recent Case Decisions | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Facts: A buyer’s agent locates a suitable property for their buyer. The seller’s agent is employed by the same broker as the buyer’s agent. The broker’s dual agency status is timely disclosed to the buyer. The listing and marketing materials provided by the seller’s agent to the buyer significantly misstate the square footage of the home and are inconsistent with public records. The seller’s agent does not bring the discrepancy to the buyer’s attention nor recommend any further investigation. After the sale closes, the buyer discovers the discrepancy in the square footage.

Claim: The buyer seeks money losses from the seller’s agent, claiming the seller’s agent breached their fiduciary duty owed to the buyer since the broker was a dual agent and thus the seller’s agent owed the buyer a fiduciary duty to investigate and disclose all information materially affecting the value and desirability of the property, such as the property’s square footage.

Counter claim: The seller’s agent claims they are not liable for the buyer’s money losses since the fiduciary relationship between the broker and buyer does not extend to the seller’s agent, who was acting as the exclusive agent of the seller.

Holding: A California Supreme Court holds the seller’s agent is liable for the buyer’s money losses since, as the employing broker was acting as a dual agent, the seller’s agent was also a dual agent who owed a fiduciary duty to the buyer. [Horiike v. Coldwell Banker Residential Brokerage Company (November 21, 2016)_C4th_]

Agent of the agent and reciprocal duties

A sales agent who provides real estate services is limited to the status of an agent working on behalf of and dependent on their employing broker. An agent, also known as an associate licensee, rendering real estate services cannot independently contract in their own name or on behalf of anyone other than their employing broker. [Calif. Business and Professions Code §10160]

Only brokers may be employed by members of the public to act on their behalf. A broker’s sales agents are therefore accurately described as agents of the agent — i.e., agents of their employing broker. Sales agents render services on behalf of the broker’s clients, and do so exclusively as their broker’s representatives. [Calif. Civil Code §2079.13(b)]

Thus, a sales agent does not have an independent agency relationship with their broker’s clients — the agency relationship of the sales agent is derived from the agency relationship that exists between the broker and the client. Sales agents therefore owe all transaction participants identical duties as the broker on whose behalf the sales agent is acting.

In this case, when the broker elected to act as a dual agent for both the buyer and seller, the seller’s agent, as an associate licensee of the broker in the transaction, assumed equivalent dual agency duties as the broker — including the fiduciary obligation to act with the utmost care, integrity, honesty and loyalty in the dealings with the buyer.

Here, the seller’s agent misinterpreted the bilateral nature of agency relationships. By the seller’s agent’s reasoning, it was a one-way street: if the seller’s agent was a dual agent, then the seller’s broker was necessarily cast as a dual agent; however, if the seller’s broker was a dual agent, this would not automatically trigger dual agency obligations (with attendant fiduciary duties) on behalf of the seller’s agent. This incorrect reasoning misconstrues the power dichotomy between broker and agent — the employing broker is the nexus by which the agency relationships of all the broker’s agents are established. Agency relationships flow from the headwaters of the broker down to the tributaries of their agents — not uphill from the agent to the broker.

Editor’s note — Even in the absence of a fiduciary duty to the buyer, seller’s agents have a general nonfiduciary duty to disclose to prospective buyers all material facts affecting the value or desirability of a property. Thus, even if the seller’s agent did not owe a fiduciary duty to the buyer, they still would have breached their general duty to disclose the significant discrepancy in the property’s square footage.

Dual agency — a double edged sword

Stated simply, a dual agent is a broker who simultaneously represents opposing principals in a transaction, either by themselves or through the agents they employ.

A dual agent owes a fiduciary duty to both principals they represent since each are the broker’s clients. Thus, the dual agency alone creates a conflict of interest, which needs to be promptly disclosed to each client. [See RPI Form 117; CC §2079.17]

Related reading:

The dual agency situation inherently imposes limitations on the benefits obtainable by the principals. Though a dual agent is duty-bound to work diligently on behalf of both clients, they are prevented from actively achieving the full advantages of negotiations for either client. Like the opposing ends of a teeter totter, a natural inability exists to simultaneously negotiate the highest and best price for the seller, and the lowest and best price for the buyer.

Thus, clients of a dual agent generally do not receive the full range of benefits available from an exclusive agent. This environment, even when handled properly, exposes dual agents to breach-of-duty claims.

This client disadvantage holds true even if different agents employed by the same broker each work with different principals in the same transaction, as this case clearly illustrates.

It all comes back to disclosure

Though this case touches on multiple bedrocks of real estate practice — dual agency, fiduciary duty versus general duty, the transmission of legal responsibilities between brokers and their agents — the catalyst which set this case in motion was the seller’s agent’s failure to disclose the discrepancy in square footage to the buyer.

Editor’s note — The discrepancy in square footage is significant. Public records indicate the property measures 11,050 square feet with 9,434 square feet of living area. However, the listing and the seller’s agent’s marketing materials state the home provides “approximately 15,000 square feet of living areas.”

Related reading:

Here, the seller’s agent unequivocally remained silent regarding the known discrepancy. Even had the seller’s agent not owed a fiduciary duty to the buyer, the seller’s agent would still have owed the prospective buyer, and also the buyer’s agent, a limited, non-client general duty to voluntarily provide critical factual information on the listed property.

What is limited about the duty is not the extent or detail to which the seller’s agent may go to provide information, but the minimal quantity of fundamental information and data about the listed property which the seller’s agent will hand to the prospective buyer or the buyer’s agent before the seller enters into a purchase agreement.

The information disclosed by the seller’s agent only needs to be sufficient to place the buyer on notice of facts which may have an adverse effect on the property’s value or interfere with the buyer’s intended use.

In this case, the seller’s agent said nothing to put the buyer or their agent on notice.

California’s public policy pursues transparency in property information between sellers and buyers. A seller’s agent’s disclosures inform prospective buyers about the fundamentals of the listed property and act to eliminate the asymmetry of information in sales transactions. Thus, the seller’s agent is severely limited in their ability to exploit the prospective buyer’s lack of knowledge about the condition of the property by use of these disclosures.

A seller’s agent fails to perform the general duty owed to the buyer to disclose knowledge of material facts — such as the actual total square footage of a property — when information that might affect the buyer’s decisions regarding an offer is withheld.

Editor’s note —The broker who employed the buyer’s and seller’s agent will also be pursued. However, the buyer stipulated they did not seek recovery for breach of fiduciary duty based on the buyer’s agent’s conduct.

Related topics:

agency, dual agency, fiduciary duty, general duty

Consumer Financial Protection Bureau (CFPB) to impose arbitration restrictions on consumer financing products and services

Consumer Financial Protection Bureau (CFPB) to impose arbitration restrictions on consumer financing products and services somebodyPosted by ft Editorial Staff | Dec 5, 2016 | Finance, Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

The Consumer Financial Protection Bureau (CFPB) recently proposed new regulations that expand the prohibition of arbitration agreements in consumer financial products and services. Arbitration provisions are already prohibited in residential mortgage agreements. However, the proposed rules significantly broaden these consumer protections, shifting focus to other consumer financial products and services overseen by the CFPB, including providers of consumer:

- credit and checking accounts;

- car leases;

- debt management services;

- credit reports;

- payment processing services; and

- debt collection.

The proposed rules will:

- prohibit consumer finance companies from using mandatory binding arbitration agreements that block consumer class action lawsuits; and

- require companies that use arbitration provisions in their agreements to submit arbitration claims, awards and records to the CFPB for abuse monitoring purposes.

The CFPB’s proposal is a response to its study on the use of mandatory arbitration provisions in consumer finance agreements. The study found most consumers are unaware their finance agreements contain arbitration provisions. And of those who are aware of the provision, the majority do not understand what the provision entails — or its very significant legal ramifications.

Further, the study found consumers were less likely to pursue a finance company through individual actions and more likely to obtain relief when taking part in a class action. Many finance companies leaned heavily on the arbitration provision as a method of keeping disputes out of court and saving money in the process.

Thus, the CFPB intends the rules to protect consumers’ rights to seek relief in court through class action lawsuits and curtail the over reliance of finance companies on arbitration as a means to block a proper hearing. The regulations are also expected to dissuade misconduct by holding finance companies accountable and providing increased transparency through the CFPB’s collection and monitoring of arbitration records.

Why focus on arbitration?

A closer look at how arbitration provisions function in finance agreements reveals the reasoning behind the CFPB’s tighter controls.

A mandatory arbitration provision in a consumer finance agreement grants a third-party arbitrator the authority to hear and resolve a dispute arising from the agreement. The arbitrator issues a binding award in favor of either the consumer or finance company as a remedy for the dispute.

In return for agreeing to arbitration, the opposing parties to the agreement relinquish their rights to settle their disputes in a court of law.

While these arbitration agreements offer a less costly and quicker alternative to a court trial, they also pose major disadvantages to consumers, including:

- the critical loss of a consumer’s rightsto a trial by jury and to appeal the arbitrator’s decision;

- the potential for egregious errors or incorrect application of the law by the arbitrator when issuing an award, which remains final and binding [Hall v. Superior Court (1993) 18 CA4th 427];

- no requirement for legal precedence, thus risking unpredictable, “arbitrary” awards;

- a lack of accountability as there is no requirement for arbitration proceedings to be published like court cases;

- the risk of a biased arbitrator since arbitrators are not prohibited from having a connection to an individual in the case; and

- the prevention of class action lawsuits by multiple consumers experiencing the same misconduct from a finance company, which reduces the likelihood of consumers obtaining relief.

Due to the risks arbitration poses to consumers and the need for a judge to protect the public, arbitration provisions are no longer permitted in trust deeds, consumer mortgage agreements and rental or lease agreements. [12 Code of Federal Regulations §1026.36(h)]

Editor’s note — Arbitration provisions have always been excluded from (RPI) Realty Publications, Inc. forms as a matter of policy since their creation in 1978.

The CFPB’s latest attention to other financial products and services is an attempt to broaden protections to ensure more consumers obtain relief when confronted by misconduct from a finance company — which is, after all, they very purpose of the CFPB.

Awaiting the next step

With the CFPB now hanging in the balance following the recent presidential election and talks of dismantling the agency, it is uncertain when or if these proposed rules will actually take effect.

According to the CFPB’s latest statement of regulatory priorities, the CFPB has received an influx of comments on the proposal and may develop a final rule in spring 2017.

In the meantime, opponents have issued rebuttals seeking to prevent implementation of the arbitration restrictions, claiming the rules will elevate costs to finance companies and consumers alike. However, the proposed rules remain a top priority for the CFPB and a critical step in protecting consumers from unscrupulous companies that seek to limit consumer access to thorough legal aid.

Related topics:

arbitration, consumer financial protection bureau (cfpb), consumer protection

DRE licensees may petition for removal of disciplinary actions

DRE licensees may petition for removal of disciplinary actions somebodyPosted by Giang Hoang-Burdette | Nov 1, 2016 | Licensing and Education, New Laws | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Calif. Business and Profession Code §10083.2

Amended by A.B. 1807

Effective date: January 1, 2018

A California Department of Real Estate (DRE) licensee may petition the DRE to remove the licensee’s disciplinary action from DRE’s public records page if:

- the disciplinary action has been posted for at least ten years;

- the licensee provides the DRE with proof they no longer pose a risk to the public; and

- the licensee pays a fee to the DRE with the petition, in an amount to be determined by DRE Regulations.

All disciplinary actions will remain on record with the DRE and continue to be shared with other licensing and regulatory agencies.

Read more:

Read the bill text.

Related topics:

Disclosures on residential earthquake insurance policies

Disclosures on residential earthquake insurance policies somebodyPosted by Giang Hoang-Burdette | Dec 23, 2016 | New Laws, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Calif. Insurance Code §§10083, 10087

Amended by A.B. 499

Effective date: January 1, 2017

An insurance provider’s offer to renew a residential earthquake insurance policy with reduced coverage or substantially different coverage than that provided in the current policy triggers the need to provide to the homeowner a standalone disclosure of the changes.

If a renewal application or disclosure connected with a residential earthquake insurance policy is hand delivered, a signed acknowledgement of receipt is sufficient to prove the insurance provider met their disclosure requirement.

Read more:

Related topics:

homeowners insurance

Do extensive pre-eminent domain tests and studies constitute a taking of property?

Do extensive pre-eminent domain tests and studies constitute a taking of property? somebodyPosted by ft Editorial Staff | Aug 26, 2016 | Laws and Regulations, Real Estate, Recent Case Decisions | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Property Reserve, Inc. v. Superior Court