2018

2018 somebody2018 changes to tax deductions

2018 changes to tax deductions somebodyPosted by Carrie B. Reyes | Feb 12, 2018 | New Laws, Tax | 3

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

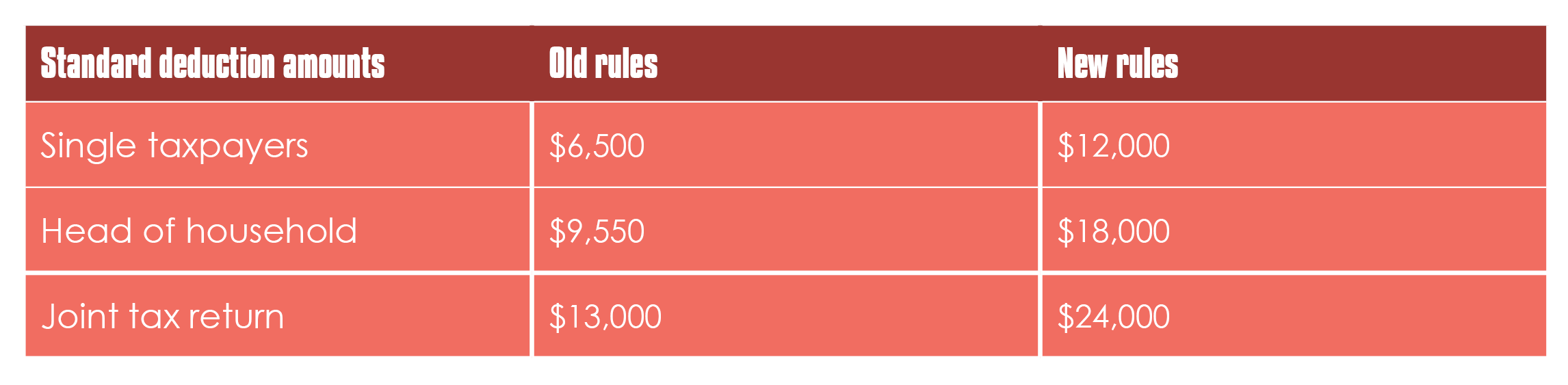

As you prepare 2017 taxes this tax season, take a look ahead to when you pay 2018 taxes next year. The deductions you will be able to take then — and how you take them — will be very different.

First of all, the standard deduction amount will now be about double the size of the 2017 standard deduction.

Standard deduction amounts

The new higher standard deduction amounts have two results:

- Households that typically have taken the standard deduction will see a tax cut since the deduction is now much higher.

- It will now make more financial sense for most people to take the standard deduction rather than itemize, resulting in higher taxes for about half the people who used to itemize under the old rules.

For real estate, this change is particularly important since the mortgage interest deduction (MID) can only be taken if a homeowner itemizes their taxes. Therefore, fewer homeowners will take the MID in future years.

Itemized deductions

For those who itemize their deductions — and will continue to itemize under the new plan — there are some significant changes in tax year 2018, including:

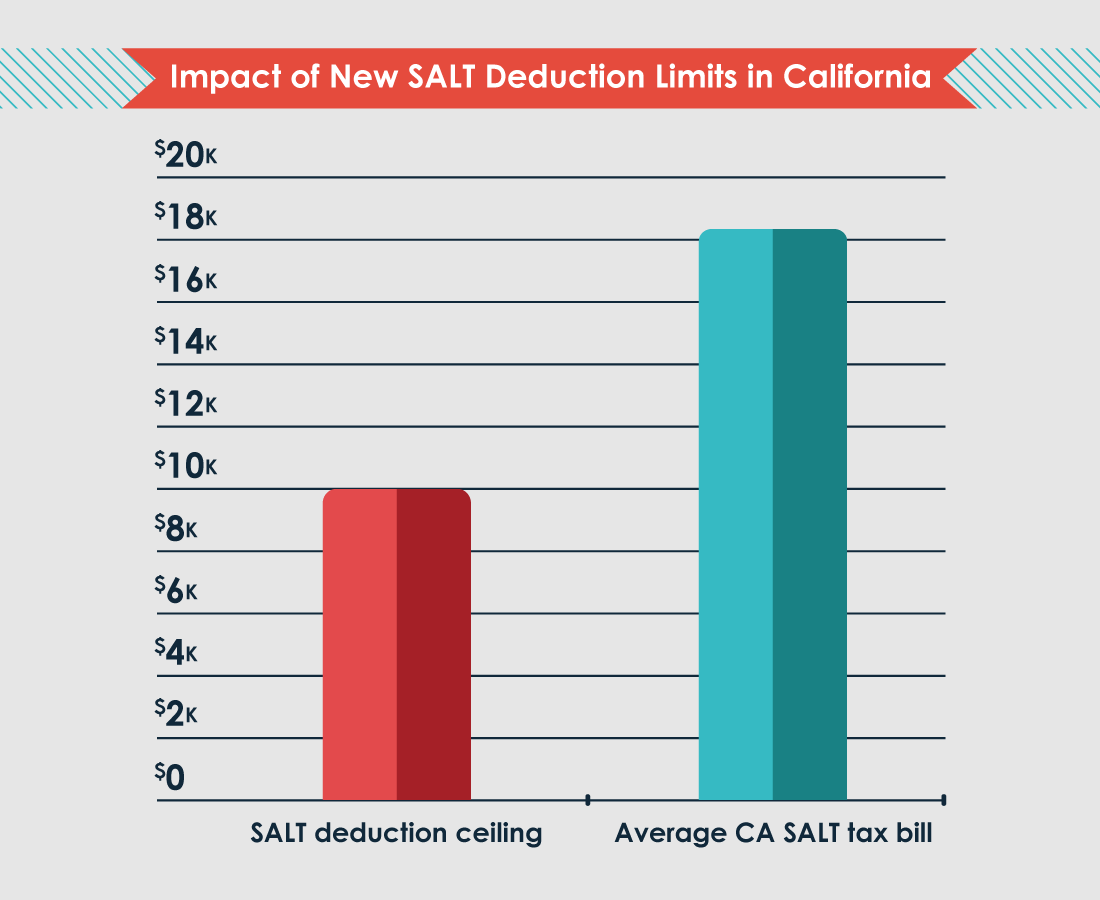

- State and local (SALT) taxes are now limited to $10,000 per tax return, whether the return is for an individual or couple;

- the ceiling for the mortgage interest deduction (MID) is lowered from mortgages of up to $1 million to $750,000 — and interest on home equity loans (HELOCs) can only qualify for the MID if they fund home improvements; and

- the deduction for moving expenses may now only be claimed by military families.

These changes will have a particular impact in states like California, which has the highest home prices in the nation (second only to the District of Columbia). Therefore, SALT taxes and mortgage amounts are both much higher than average here.

In other words, the state’s high standard of living translates to higher tax amounts for residents. But under the old tax rules, SALT taxes used to be fully deductible. Now, they will only be deductible up to $10,000. For reference, the average Californian pays $18,438 in SALT taxes.

The good news for California residents with high SALT bills is state legislators are working diligently on a workaround.

One such workaround was introduced in Senate Bill 227 in January 2018, which would allow residents to make a charitable contribution to the state on SALT bill amounts exceeding the $10,000 deduction cap. Individuals would still pay the same amount to the state, but by classifying whatever payment exceeds $10,000 as a charitable contribution, they are allowed to deduct their full payment.

Check back for details on how this bill pans out in the legislature.

Related topics:

mortgage interest deduction (mid), tax 2018, tax aspects

As California’s coast gentrifies, what’s next?

As California’s coast gentrifies, what’s next? somebodyPosted by Carrie B. Reyes | Jul 16, 2018 | Feature Articles, Laws and Regulations | 2

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Is gentrification such an ugly word, after all?

Gentrification is the process of wealthy residents moving into previously low-income, urban neighborhoods. In the process, these mid- and high-income households displace long-term residents, giving gentrification its bad reputation.

However, a recent article in the Economist claims gentrification actually has more benefits than disadvantages — but does the argument hold up in California?

The benefits cited include:

- rising property values, which benefits long-time homeowners in gentrifying neighborhoods;

- the arrival of more goods and services to the neighborhood, which benefits all residents, old and new; and

- a reduction in crime.

Most importantly, the article claims there is little evidence to support the belief that when high-income residents move in, low-income residents need to move out. In fact, long-term residents are more likely to stay in gentrifying neighborhoods than residents of non-gentrifying, low-income neighborhoods.

How does that work?

Zoning laws are less strict in low-income parts of cities than in neighborhoods where high-income residents already live. Therefore, it’s easier to build up gentrifying neighborhoods than long-standing high-income areas. So, when a high-income household moves into the neighborhood, they aren’t necessarily taking the home of a low-income earner. They’re more likely moving into a newly built, luxury multi-family unit.

At least, that’s how it ought to work — but gentrification isn’t always so neat, especially in California’s vocal not-in-my-backyard (NIMBY) neighborhoods. But more on that in a bit.

Perhaps the biggest benefit of gentrification is its push against income segregation.

Income segregation is bad for real estate

When you hear the phrase income segregation, you probably think about pockets of low-income neighborhoods within your closest urban center. But in practice, income segregation means the isolation of high-income households, resulting in pockets of wealthy neighborhoods in an otherwise low-income cityscape.

Income segregation of wealthy households allows fewer individuals to benefit from a city’s wealth and resources. To translate into real estate terms, it means the majority of a city’s housing stock remains low-tier or simply rentals, while those coveted high-tier home sales are few and far between, accessed by only a select number of real estate professionals.

Income segregation occurs more often in metro areas where there is a high level of local participation in zoning decisions. In contrast, metros located within states that have more top-down state-level involvement in zoning laws see less income segregation, according to a UCLA study.

Here in California, we have a lot of local involvement in our desirable coastal cities. NIMBY advocates are on every block, most infamous in San Francisco.

The number of new jobs in San Francisco has increased at eight times the rate of new housing additions, according to the Economist. Normally, more jobs translates to more real estate transactions. After all, workers need somewhere to live. But San Francisco’s stubborn refusal to add to its existing housing stock has resulted in more people living in crowded situations, along with workers living further away from the city.

Gentrification has been rampant in San Francisco during the past couple of decades. For example, the median value of a home in the Mission District was $278,400 in 1998, compared to $1.49 million in 2018, according to Trulia. That’s an increase of 535% in 20 years.

During those years, the neighborhood has changed dramatically, as the children who grew up in the Mission became priced-out of the area as adults. Even their parents who lived in the neighborhood for decades are no longer able to stay, as renter protections designed to protect long-time residents fail when landlords ignore these laws.

Even though gentrification brings some advantages and improvements, the process is hard on long-term residents, to say the least.

Legislation for more construction

Local regulations have held back new construction and growth for too long now, causing housing costs to soar, holding back economic growth and forcing residents to leave for other states.

The good news: California state legislators have started to pay attention.

In late 2017, a package of bills aimed to increase the affordable housing stock passed in California. Among these bills are new laws that will:

- make it more difficult for local governments to re-zone neighborhoods to reduce density;

- streamline the approval process for new residential construction;

- limit parking requirements, making more efficient use of land near public transportation;

- advance the environmental review process for affordable housing projects; and

- set aside more money for homeless shelters and veteran housing.

Related article:

For residents of gentrifying neighborhoods — and real estate professionals who rely on a steady flow of transactions to make a living — these new laws are a step in the right direction toward more financial stability.

The research tells us gentrification doesn’t have to be as painful or one-sided as it is in places like the Mission District. Ultimately, the diversity of incomes and services gentrification brings with it benefits residents. But only if these residents aren’t forced out of their neighborhoods.

The solution is more construction in these desirable areas, and quickly. Expect to see this happen in the coming years, as California’s legislation finally catches up to demand.

Related topics:

california zoning, gentrification, san francisco

Bonds for affordable housing and farm and home aid for veterans

Bonds for affordable housing and farm and home aid for veterans somebodyPosted by Benjamin J. Smith | Jan 3, 2018 | Laws and Regulations, New Laws, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Calif. Health and Safety Code §54000, 54004, 54006, 54007, 54009, 54010, 54016, 54018, 54026, 54028, 54034, Military and Veterans Code §998.600, 998.601, 998.603, 998.604, 998.608

Added by S. B. 3

Effective date: November 6, 2018

The Veterans and Affordable Housing Bond Act of 2018 will be voted on in the statewide general election on November 6, 2018. If passed, it will create the Affordable Housing Bond Act Trust Fund of 2018. The Housing Finance Committee (HFC) will authorize $3,000,000,000 of bonds to be issued and sold for these purposes. The bonds will have a maturity date of no more than 35 years from the date the bonds were issued. Allocations are set at:

- $1,500,000,000 to the Housing Rehabilitation Loan Fund, to be used for the Multifamily Housing Program for new construction, rehabilitation and preservation of permanent and transitional rental housing for people with up to 60% of the area median income;

- $150,000,000 to the Transit-Oriented Development Implementation Fund to assist in developing high-density uses close to transit stations to promote use of public transportation;

- $300,000,000 to the Regional Planning, Housing, and Infill Incentive Account, which this act also creates, to assist in developing high-density mixed-income housing in locations designated as infill;

- $150,000,000 to the Self-Help Housing Fund for use in the California Housing Finance Agency’s home purchase assistance program;

- $300,000,000 to the Joe Serna, Jr. Farmworker Housing Grant Fund, for the construction or rehabilitation of housing for agricultural employees or for acquisition of manufactured housing to remedy farmworker displacement from existing housing;

- $300,000,000 to the Affordable Housing Innovation Fund for the creation of local pilot programs which create and preserve affordable housing; and

- $300,000,000 to the Self-Help Housing Fund to assist the CalHome Program in the development of multifamily housing units, at least $30,000,000 of which will be used for the rehabilitation or replacement of mobilehomes.

Any funds not used by the program to which they are allocated will be reallocated to the Multifamily Housing Program. Programs will give preference to public works projects.

The Department of Housing and Community Development (HCD) may provide engineering assistance and environmental review for the Multifamily Housing Program, the Joe Serna, Jr. Farmworker Housing Grant Program and the CalHome Program using the bond proceeds allocated to those programs.

All premiums and accrued interest on sold bonds will be transferred to the General Fund as credit to expenditures for bond interest. Amounts derived from premiums may be reserved to pay the cost of bond issuance before transfer to the General Fund.

The state will collect an annual sum of money in addition to ordinary revenue to pay the principal and interest for the bonds, which may be refunded like any other government bond. Any refund bonds are authorized by the passage of the act.

In addition, the Veterans Finance Committee (VFC) may create a debt of the State of California of no more than $1,000,000,000 to provide farm and home aid for veterans.

When the state collects revenue for these bonds, money will be transferred to the Payment Fund to pay the debt service on all the money in the fund, not including refunding bonds. When the money transferred is less than debt service due, the unpaid balance will be transferred to the General Fund, with interest at the same rate of interest as the bonds, compounded semiannually.

Editor’s note — This is one of several bills passed by the California legislature to address the state’s housing shortage.

Related topics:

affordable housing

CFPB adopts new strategic plan, aims to “go no further”

CFPB adopts new strategic plan, aims to “go no further” somebodyPosted by Carrie B. Reyes | Feb 19, 2018 | Laws and Regulations | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Changes at the Consumer Financial Protection Bureau (CFPB) are well underway.

The CFPB released their new strategic plan for 2018-2022. This replaces their last four-year plan, in place from 2013-2017.

The old plan was mostly focused on forging a path for what, at the time, was a new bureau, primed with optimism to change the financial landscape. The new plan is much less ambitious:

| Old goals | New goals |

| Prevent financial harm to consumers while promoting good practices that benefit them. | Ensure that all consumers have access to markets for consumer financial products and services. |

| Empower consumers to live better financial lives. | Implement and enforce the law consistently to ensure that markets for consumer financial products and services are fair, transparent, and competitive. |

| Inform the public, policy makers, and the CFPB’s own policy-making with data-driven analysis of consumer finance markets and consumer behavior. | Foster operational excellence through efficient and effective processes, governance and security of resources and information. |

| Advance the CFPB’s performance by maximizing resource productivity. |

CFPB acting director Mick Mulvaney put it this way in the press release announcing the new plan: “we have committed to fulfill the Bureau’s statutory responsibilities, but go no further.” Ambitious, indeed.

What happens when anti-regulators are in charge of the CFPB

These changes are the perfect realization of the current administration’s outlook on financial market regulation.

The former director the CFPB, Richard Cordray, was put in place by President Obama to lead the agency in its infancy. Cordray stepped down late in 2017 following several setbacks which had the CFPB butting its head against a regulation-resistant administration.

President Trump appointed Mick Mulvaney to head the CFPB in November 2017. Since then, Mulvaney has taken the initial steps to rollback and soften the significant strides the CFPB has taken in consumer protection. Some of these strides have included:

- making mortgage and other financial forms more accessible by abridging them and translating them into plain English;

- receiving and addressing consumer complaints;

- filing dozens of lawsuits against financial companies for harming consumers; and

- making and enforcing new consumer financial laws.

Now, the CFPB is turning its sights from protecting consumers to protecting Big Banks.

Or, as stated in the CFPB’s press release announcing their new strategic plan:

“… the Bureau will now focus on equally protecting the legal rights of all, including those regulated by the Bureau, and will engage in rulemaking where appropriate to address unwarranted regulatory burdens and to implement federal consumer financial law and will operate more efficiently, effectively, and transparently.” [Italics added for emphasis]

In all likelihood, all of this points to fewer regulations over lenders, appraisers, banks and creditors. And we all know how well that turned out last time — the Millennium Boom was great for everyone — until it burst and plunged the nation into the worst financial crisis and recession since the Great Depression.

Want to weigh in? The CFPB is currently accepting comments on their future regulatory actions. Comments need to be submitted by April 13, 2018. Submit your comments at the Federal Register.

Related topics:

banks, consumer financial protection bureau (cfpb)

CFPB takes first steps to rollback regulations

CFPB takes first steps to rollback regulations somebodyPosted by ft Editorial Staff | Jan 18, 2018 | Pending Laws | 5

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Big changes for financial regulation are on the horizon.

In a press release, the Consumer Financial Protection Bureau (CFPB) announced it will be reviewing its policies, rules and educational materials.

In the release, acting Director Mick Mulvaney says: “Much can be done to facilitate greater consumer choice and efficient markets, while vigorously enforcing consumer financial law in a way that guarantees due process.”

In other words, the CFPB is thinking about rolling back some of its regulation put in place under former leadership, put in place by the Obama administration.

Related article:

The CFPB was created in 2010 by the Dodd-Frank Wall Street Reform and Consumer Protection Act and started formally practicing in 2011. Since then, the CFPB has changed the way real estate agents, lenders, appraisers and consumers do business in the real estate market.

Changes ahead

Some of the most significant transformations to the financial industry the CFPB spearheaded include:

- making mortgage and other financial forms more accessible by abridging them and translating them into plain English;

- receiving and addressing consumer complaints;

- filing dozens of lawsuits against financial companies for harming consumers;

- making and enforcing new consumer financial laws; and

- implementing changes under the Truth in Lending Act (TILA).

But, in keeping with the administration’s stated goals, the CFPB’s newly appointed leadership seeks to turn back the clock.

President Trump recently boasted he has “done more on knocking out regulations than any other president in our history… and we haven’t even started.” As evidence, in July 2017, the Trump administration put a stop to 860 pending regulations, including consumer protections and environmental rules, according to the Los Angeles Times.

Following the administration’s deregulatory agenda, the acting director is gathering information to take the teeth out of the CFPB.

Looking to the future, this anti-regulatory agenda will see a return to the lending environment of the Millennium Boom — think “no doc” loans and zero down payments. It’s very exciting in the moment, when homeownership soars and home prices become untethered from what can be sustained by reasonably qualified buyers. But when the inevitable crash comes, the resulting price plunge and spike in foreclosures will be steep and terrible for housing.

Before any changes are official, the CFPB is requesting public comment on its activities. Comments can be submitted via the Federal Register, with details to be published in the coming weeks. Check back here for links to submit your comments as they become available.

Submit your comments at the Federal Register, here.

Related topics:

consumer financial protection bureau (cfpb), deregulation

CFPB updates revise Closing Disclosure timeline rules

CFPB updates revise Closing Disclosure timeline rules somebodyPosted by Carrie B. Reyes | May 21, 2018 | Finance, New Laws | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

The Consumer Financial Protection Bureau (CFPB) is announcing updates to its Closing Disclosure timeline when significant revisions are made to the Loan Estimate and Closing Disclosure.

This rule takes effect for all lenders handling mortgage documents beginning June 1, 2018.

Some background:

A Loan Estimate is required to be delivered to the homebuyer within three business days of the lender’s receipt of the mortgage application. [12 Code of Federal Regulations §1026.19(a); see RPI Form 204-5]

The final Closing Disclosure needs to be delivered to the homebuyer at least three business days before closing is scheduled. [12 CFR §1026.19(f)(ii)(A); See RPI Form 402]

Upon receiving the Closing Disclosure, homebuyers are instructed to compare their Loan Estimate with the Closing Disclosure to ensure no significant changes have occurred.

Some small variances may occur from the original Loan Estimate to the Closing Disclosure, such as a change in fee charged by a party to the transaction who is not the lender or homebuyer (e.g. a title insurance provider). [12 CFR §1026.19(e)(3)]

When these variances occur on a large scale, sometimes the lender is able to provide a revised Loan Estimate. [12 CFR §1026.19(e)(3)(iv)]

A Loan Estimate revision may only be given to an applicant when:

- a changed circumstance impacts the homebuyer’s eligibility or the real estate’s value;

- the homebuyer requests a change to the mortgage terms;

- a changed circumstance causes the closing costs to increase by more than 10%;

- the interest rate was not locked when the Loan Estimate was provided, and locking the interest rate causes the points or lender credits to change;

- the consumer indicates they will proceed with the transaction more than ten business days after the Loan Estimate was provided; or

- the settlement for a mortgage on a new construction mortgage is delayed more than 60 calendar days and the original Loan Estimate states the lender may issue a revised disclosure 60 days before closing. [12 CFR §1026.19(e)(3)(iv)]

Lenders may not revise Loan Estimates simply due to technical errors or miscalculations of charges. [12 CFR §1026.19(e)(3)(iv)]

Since a Loan Estimate is used to ensure the estimated costs were made in good faith when compared with the final costs in the Closing Disclosure, the revised Loan Estimate may not be delivered on the same day as, or after the Closing Disclosure. [12 CFR §1026.19(e)(4)(ii)]

Thus, once the Closing Disclosure has been issued, the Loan Estimate may no longer be revised to reflect the changes. Instead, any significant changes that occur require a revised Closing Disclosure.

Under the old system, lenders that issued a revised Closing Disclosure needed to provide it to the homebuyer at least four days prior to closing, and within three days of the lender becoming aware of the changed circumstance. [12 CFR §1026.19(e)(3)-(4)]

This created what is known as the TILA-RESPA “black hole”. Changes triggering a revision to the Closing Disclosure that occurred in the last four days of closing leave a gap which can cause some lenders to avoid charging homebuyers higher rates (when they are valid), simply to avoid delaying closing.

The CFPB’s ruling says this has been damaging to lenders. It claims lenders, rather than move closings, may have charged higher fees or raise their mortgage rates as a result, passing on the unclaimed higher costs they are unable to charge in these special circumstances on to the next homebuyers.

Therefore, the new rule allows the Closing Disclosure to show revised costs, without a restriction on when it is provided in relation to closing.

Example

For example, consider a homebuyer taking out a mortgage and preparing to close on a home. Their lender provides the required Closing Disclosure three days before closing is scheduled.

After the homebuyer receives the Closing Disclosure and before they close, they request closing be pushed back more than seven days.

They also request a change which results in a higher annual percentage rate (APR), increasing closing costs by more than 10%. A change of this magnitude would normally require a revised Loan Estimate be issued, but the lender is prohibited from providing a revised Loan Estimate at the same time or after the Closing Disclosure has been issued. [§1026.19(e)(4)(ii)]

Therefore, the lender’s correct option is to issue a revised Closing Disclosure. But the lender needs to do this both within three days of the requested changes, and within four days before closing is scheduled. [12 CFR §1026.19(e)(4)(i)]

But since the homebuyer requested closing be pushed back more than seven days, under the old system, the lender is unable to comply with the law and provide the homebuyer with a revised Closing Disclosure within four days of closing and within three days of the requested change.

This is the “black hole” issue lenders which previously forced lenders to either:

- refuse to push back closing so the homebuyer can receive the revised Closing Disclosure within the appropriate timeframe; or

- absorb the additional costs beyond the 10% increase over the original Closing Disclosure caused by the higher APR.

This new rule removes the lender’s calculus, and simply says that when a valid reason causes the Closing Disclosure to change, they may provide the revised Closing Disclosure regardless of the timing, and regardless of when the homebuyer receives the revision in relation to closing.

Related topics:

closing disclosures, loan estimate

California Homeowner Bill of Rights is reenacted

California Homeowner Bill of Rights is reenacted somebodyPosted by Carrie B. Reyes | Dec 11, 2018 | Laws and Regulations, New Laws | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Calif. Civil Code §§2924, 2923.4, 2923.5, 2923.6, 2923.7, 2924.12, 2924.12, 2924.17, 2923.55, 2924.9, 2924.10, 2924.11, 2924.18, 2924.19

Amended and added by S.B. 818

Effective date: January 1, 2018

This bill reenacts many portions of the 2012 California Homeowner Bill of Rights, which expired on January 1, 2018. California’s legislature intends the laws put in place by this bill will take over for the laws which expired January 1, 2018.

When a homeowner becomes delinquent on their mortgage, the lender, mortgage servicer or bank may not record a notice of default (NOD) unless 30 days have passed since contacting or making a diligent effort to contact the homeowner, including mailing a notice and calling at different times of day.

However, when a homeowner makes a written request for the lender to cease communications, the lender is exempt from the telephone contact requirement.

Within five days after recording an NOD, the lender needs to send a written notice to the homeowner regarding any foreclosure prevention alternative it offers, including information on how the homeowner may apply to be considered for these foreclosure prevention alternatives.

The homeowner may submit a complete application for a first lien mortgage modification to the lender. While that application is pending, the lender is prohibited from recording an NOD or notice of trustee’s sale (NOTS), or conducting a trustee’s or foreclosure sale. To qualify for this exclusion, the homeowner’s complete application needs to be submitted at least five business days before the trustee’s sale is scheduled to take place.

To be considered complete, the homeowner’s application for a mortgage modification needs to include all documents required by the lender and be submitted within the reasonable timeframes the lender specifies.

When their application is approved, the homeowner needs to accept the first lien mortgage modification within 14 days of the lender’s offer, otherwise the lender may proceed with the foreclosure process.

Throughout the process, the lender needs to provide the homeowner with a single point of contact.

Once the lender receives the homeowner’s complete application for mortgage modification, it needs to provide the homeowner with written acknowledgment that it has received the application within five days of receipt. At that time, the lender also needs to provide information about the mortgage modification process, including any deadlines the homeowner needs to adhere to in order to be considered for foreclosure prevention.

When a lender approves the mortgage modification application after an NOD has already been recorded, the lender may not complete an NOTS or trustee’s sale as long as the conditions for approval continue to be met. Further, if an NOTS has been issued or a trustee’s sale scheduled, these need to be canceled as long as the conditions for mortgage modification are met.

The lender may not charge a fee for a mortgage modification or other foreclosure alternative on a first lien.

If a mortgage with an approved mortgage modification is transferred to another mortgage servicer, the new servicer needs to honor the agreed-to terms on the modification.

When the lender denies the mortgage modification, it needs to provide the homeowner with a written notice identifying the reasons why the application was denied.

Further, when the homeowner is rejected for a loan modification, the servicer needs to wait at least 31 days after the homeowner is notified before recording an NOD or — if an NOD was already recorded — recording an NOTS.

When the mortgage modification is denied, the homeowner has 30 days to appeal and provide evidence of any errors the lender made in its determination to reject their application for mortgage modification.

During the 30-day appeal period, the lender may not file an NOD. However, if an NOD has already been filed, the lender may not record an NOTS or conduct a trustee’s sale.

California homeowners have the right to sue lenders who do not comply with these laws for up to $50,000.

Read more:

Related topics:

notice of default (nod), notice of trustee sale (nots)

California bill seeks to fill gap left by federal tax changes to help homeless population

California bill seeks to fill gap left by federal tax changes to help homeless population somebodyPosted by Carrie B. Reyes | Jun 25, 2018 | Pending Laws, Tax | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

California’s homeless population has soared in recent years, due in large part to the state’s housing shortage and affordability crisis.

Legislators have been working on various fixes, most notably passing several bills at the end of 2017 aimed at increasing the affordable housing stock and providing funding for more shelters and homeless services.

But this package of bills passed just a few weeks before the 2018 federal tax changes came to light. Buried in the new tax law is a change that reduces the low-income housing tax credit (one of many ways federal legislators chose to pay for some of their hefty tax cuts).

With the reduced tax credit, California will lose $540 million for its low-income housing programs, equivalent to 4,000-5,000 units.

This couldn’t come at a worse time.

Today’s homeless population numbers 134,000 in California, and this population continues to increase each year, according to State Senator Beall’s office. From 2016 to 2017, the state’s homeless population increased 14%.

For an extreme example, consider Los Angeles where the homeless population increased twice as fast as the state — over 30% in the past year alone, amounting to an increase of 13,000 homeless individuals. With shelters overflowing, most of the state’s homeless are literally living on the streets.

The rising tide of homelessness is just one visible reminder of the lack of low- and mid-tier housing available to house California’s growing population. High demand for few units has created today’s runaway home prices, which have kept many out of homeownership, slowing the income stream for real estate professionals.

An attempted fix

State senators are attempting to find a replacement for the missing funding.

Editor’s note — Multiple co-authors are joined together on this effort. Together, they represent various parts of the state: San Jose, Berkeley, San Francisco, Riverside and Santa Barbara.

Their bill, Senate Bill (SB) 912, seeks funding from the 2018-2019 budget to focus on providing services and shelters for vulnerable populations, including:

- the chronically homeless who otherwise may end up incarcerated;

- youth;

- homeless college students;

- families who have previously been homeless;

- survivors of domestic violence;

- veterans; and

- persons who are physically or mentally disabled.

Providing shelter and services to the homeless population actually saves money, as it is much more costly to police and provide emergency care to the homeless than to simply provide shelter that reduces the need for these emergency services. But it does require an upfront investment that many tax-cutting legislators balk at.

Just how much of an investment is California willing to make?

It’s hard to say at this point — the original bill, which has since been amended, called for $5 billion in funding to address the homeless crisis. The amended version of the bill has removed all dollar figures, simply calling for generic “funding.”

While this language provides little guarantee, today’s bunch of state legislators have shown they are serious about doing their part to alleviate California’s housing crisis. We will have to wait and see just how committed they are to fighting homelessness when the final budget is passed later this summer.

Related topics:

homelessness, tax 2018

California passes law easing building restrictions for new developments

California passes law easing building restrictions for new developments somebodyPosted by Carrie B. Reyes | Nov 5, 2018 | Home Sales, New Laws | 3

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Governor Brown recently approved California’s AB 3194, amending portions of the Housing Accountability Act, also known as the anti-NIMBY (not-in-my-backyard) legislation.

This new law closes loopholes left open by previous laws and adjusts zoning standards. But in a nutshell, AB 3194 makes it easier for developers to build affordable housing developments.

This new law builds on 2017’s AB 1515 which considered housing developments and emergency shelters to fall within a local housing plan — as long as there is substantial evidence leading a reasonable person to conclude that it is, in fact, consistent with the plan. This wording clearly left room for a certain level of subjectivity, which AB 3194 attempts to correct.

Under the new law, proposed housing developments for low- and moderate-income households, including emergency shelters, are considered to meet applicable zoning standards. Previously, the local government may have required re-zoning to occur before approving a proposed housing development.

Further, rather than put the burden on the housing developer to prove it meets local zoning rules, this law requires any local government seeking to reject a proposed housing development to provide written evidence that:

- it has already met its regional need for low- and moderate-income housing;

- the development would have a specific negative impact on the health or safety of residents;

- approving the development would result in a violation of a specific state or federal law;

- the proposed development is situated on and surrounded on at least two sides by agricultural or resource land;

- the proposed site lacks adequate water or wastewater facilities to accommodate the development; or

- the development is inconsistent with both local zoning rules and the general plan at the time of the completed application, and the area has adopted a lawful, revised housing element in compliance with 2015 law to meet statewide housing goals. [Calif. Government Code 65589.5(d)]

The legislative intent of this new law is for local governments to encourage urban infill rather than sprawling development into surrounding agricultural areas that may lack infrastructure. [Gov C §65589.5(c)]

Legislative impacts on affordable housing

This bill is one of many new laws passed in the past year to address the state’s housing crisis. The end result of most of these laws has been to retrieve power from the hands of vocal NIMBYs who seek to limit development in their local communities.

Insufficient new construction of low- and moderate-income housing has left the majority of renters across the state paying close to half their income on rent, and held back the home sales volume recovery.

This new law was sponsored by the California Building Industry Association, which claims the law will stimulate construction, reduce costs for builders and end users, and encourage homeownership. All of this will help grow California’s economy and maintain a healthier housing market.

Expect to see construction of new homes, particularly multi-family units, grow as a result of these combined legislative efforts in the coming years.

Related article:

Related topics:

california zoning

California wants to offer housing to tackle teacher shortage

California wants to offer housing to tackle teacher shortage somebodyPosted by Carrie B. Reyes | Sep 17, 2018 | Pending Laws, Property Management | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

California’s teacher shortage continues to worsen, and one major culprit is lack of affordable housing.

Three-quarters of California school districts are experiencing a lack of qualified teachers available to fill openings. This shortage is due to insufficient numbers of new replacement teachers in the pipeline to replace retiring teachers. Further, in high-cost areas, current and potential teachers are simply unable to afford to live where they work. 29% of school districts experiencing teacher shortages cite high costs of living as a major reason, according to a study by the Learning Policy Institute.

For example, just 1% of teachers in San Francisco and 2% of teachers in San Jose can afford to buy a home in the area, according to a Trulia analysis. As a result, the teacher shortage worsens.

A 2018 bill, AB 224, proposes to work with California school districts to provide affordable housing for teachers and other school district employees. In this case, affordable housing means housing for which low- and moderate-income households are qualified to pay.

The bill allows developers and school districts to borrow from the California Housing Finance Agency to build affordable teacher housing. They will not need to begin paying back the loan until tenants move in and begin making rental payments.

This move follows California’s Teacher Housing Act of 2016, which exempted school district housing receiving state funding from the law preventing tenant discrimination based on profession. [Calif. Health & Safety Code §§53570 et seq.]

Failing California’s most essential residents

Critics of Sacramento’s efforts to provide more affordable rental housing specifically for teachers say it takes resources from other low-income households. After all, the housing shortage isn’t limited to teachers. It impacts workers in the health services, retail, emergency services and restaurant industries, among others.

Related article:

Further, the 2016 law and the 2018 bill open the door for more teacher housing, but they don’t ensure it. That’s because they don’t address zoning restrictions that limit dense development in desirable areas where housing costs are highest. Finding developable land is tough for school districts, and using their own land is often met with local opposition who say school district land ought to be devoted solely to schools, according to Mercury News.

As a result of these many obstacles, very few new teacher developments are likely to result from the 2016 law and this bill, even if it is passed. In fact, just 1% of California school districts plan to use some sort of housing incentives to attract teachers to their district, according to the Learning Policy Institute study.

To truly address the problem, California needs to tackle the lack of low- and moderate-income housing head-on.

Some steps are being taken to add to the affordable housing stock at the statewide level, but local efforts need to be pursued, too. These steps will ideally take the form of loosening zoning restrictions to allow for more low- and moderate-income housing in desirable areas. Only then will multi-family construction increase, and rents and prices will cool off and fall closer in line with local incomes.

Related topics:

affordable housing, housing shortage

California’s Homeowner Bill of Rights is back

California’s Homeowner Bill of Rights is back somebodyPosted by Carrie B. Reyes | Oct 15, 2018 | Mortgages, New Laws | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

California’s Homeowner Bill of Rights was signed into law in 2012 at the tail-end of the Great Recession and foreclosure crisis that forced many residents out of their homes, some unfairly and unlawfully. Its aim was to give qualified homeowners facing foreclosure a meaningful opportunity to obtain a mortgage modification and keep their homes. [Calif. Civil Code §2923.4]

This Homeowner Bill of Rights was automatically repealed January 1, 2018. A new bill, SB 818, has reinstated many of the provisions of the original bills.

The biggest changes the Homeowner Bill of Rights made were to prevent:

- dual-tracking foreclosure, when a homeowner is simultaneously going through the mortgage modification process and the foreclosure process;

- robo-signing of foreclosure documents, heightening the risk for wrongful foreclosure; and

- more than one point of contact for distressed homeowners in the foreclosure process.

These protections are once again in place for first lien mortgages secured by residential property. The main differences between the original Homeowner Bill of Rights and this new version are new exceptions:

- allowing servicers to be exempt from the provisions in SB 818 when an application for a mortgage modification is received less than five days before a scheduled foreclosure sale; [CC 2924.18(a)] and

- exempting servicers from the telephone contact requirements of SB 818 when the homeowner has notified the servicer in writing to cease and desist all communications. [CC 2923.5(e)(2)(C)(ii)]

When a homeowner requests a foreclosure prevention alternative such as a mortgage modification, the servicer needs to promptly establish a single point of contact for the homeowner. This will prevent confusion and help prevent the homeowner from becoming lost in the shuffle of other homeowners considering foreclosure prevention options. [CC §2923.7(a)]

Mortgage servicers may not record a notice of default (NOD) until:

- at least 30 days have passed after initially contacting the homeowner; or

- if the servicer is unable to contact the homeowner, they have satisfied the due diligence requirements made to reach the homeowner, including mailing a notice and calling at different times of day. [CC 2923.5(a)(1)(A)]

Further, servicers may not record an NOD when a homeowner submits a complete application for a loan modification at least five business days before a scheduled foreclosure sale. Once the servicer provides the homeowner with a written decision on the loan modification, the servicer may proceed with the foreclosure process if necessary. [CC §2923.5(a)(1)(B)]

When the homeowner is rejected for a loan modification, the servicer needs to wait at least 31 days after the homeowner is notified before recording an NOD or — if an NOD was already recorded — recording a notice of trustee’s sale (NOTS). [CC §2923.6(e)]

When the homeowner is approved for a loan modification, the servicer may not proceed with the foreclosure process as long as the homeowner complies with the terms of the modification. [CC §2924.18(a)(2)(A)]

Servicers may not charge homeowners any fees to apply or obtain a mortgage modification or other foreclosure prevention alternative. [CC §2924.11(e)]

The bill gives California the right to sue lenders and banks up to $50,000 for violating the laws. [CC §2924.19(b)]

Looking ahead to the next recession

The original Homeowner Bill of Rights was scheduled to expire in 2018, undoubtedly because the 2012 legislature figured the foreclosure crisis would be well over by now.

They were right — foreclosures reached a healthy level in 2016, and have remained low well into 2018. But the cycle of housing boom and bust continues to roll on, and the next recession is approaching on the horizon.

Experts forecast the next economic recession to arrive in 2020. Leading up to that recession, home sales volume will slow (as it is already in the process of doing) and home prices will flatten and drop off, expected to begin in 2019. This is all precipitated by rising interest rates, which have dampened buyer purchasing power and discouraged homebuyers.

Slowing sales and falling prices inevitably lead to an uptick in foreclosures as fewer homeowners who need to sell are able to. However, the 2020 recession won’t see the same type of foreclosure activity that reached a crisis level in 2008 and the years following. The laws put in place in the recovery years have stemmed the tide of unqualified homeowners, thus more homeowners will be able to continue to pay their mortgage during the coming recession than in 2008.

Still, the common-sense protections provided in the Homeowner Bill of Rights will be needed for those who do face foreclosure in the coming years. Fewer needless foreclosures protects homeowners and the housing market at large, including the real estate professionals who seek to weather the coming recession.

Related topics:

foreclosure, homeowner bill of rights, loan modification

Change the Law: The DRE should auto-exempt eligible 70/30 licensees

Change the Law: The DRE should auto-exempt eligible 70/30 licensees somebodyPosted by Oscar Alvarez | Nov 26, 2018 | Change The Law, Laws and Regulations, Licensing and Education, Real Estate | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Our Proposal: We propose the California Department of Real Estate (DRE) automatically exempt eligible licensees from the required continuing education (CE) using the 70/30 exemption rule.

Why: All California DRE agents and brokers are required to complete 45 hours of continuing education every four years. [Calif. Business and Professions Code §10170.5]

The DRE’s 70/30 continuing education exemption rule exempts licensed agents and brokers from this requirement when:

- the licensee is at least 70 years or older before the expiration of their license’s two-year grace period; and

- their license has been in continuous good standing for at least 30 years. [Bus P & C §10170.8]

Related Article:

If a licensee qualifies, they need to use the Continuing Education Extension/Exemption Request form (RE 213) to apply for the exemption. The form asks licensees to submit:

- a copy of their birth certificate or driver’s license;

- any other supporting documents showing the number of years licensed; and

- and the date first licensed.

This exemption request is unnecessary since the DRE already holds the information needed to qualify a licensee for the 70/30 exemption. In fact, licensees can learn if they qualify through the DRE’s own website, which provides a public licensee information lookup tool.

In addition, the DRE already requests the applicant’s birthdate on the Salesperson License Application forms (RE 400A and RE 435). This piece of information can even be verified at the time of an applicant’s exam, since a government-issued photo ID is required when taking the state exam.

An agent or broker without a lapse in their license or disciplinary actions has shown they have practiced in good faith for their entire career. Why not return this good faith and automate the 70/30 exemption process? Agents and brokers with such spotless records are entitled to this exemption.

The DRE mails a reminder to licensees 60 days prior to their license’s expiration date as a courtesy. This would be a perfect opportunity to exempt licensees from continuing education requirement or at least notify eligible licensees about the exemption.

By not notifying or automatically exempting eligible licensees, the 70/30 rule often goes unnoticed and underused, costing licensees extra fees and time otherwise not required to maintain an active license.

Cutting unnecessary bureaucracy and costs is especially critical now that most active full-time agents are only generating incomes sufficient to support a minimal subsistence, until sales volume increases around 2019.

What you can do: While waiting for the DRE to streamline the exemption process, renewing licensees can check their eligibility for the 70/30 exemption through the DRE’s website.

The DRE recommends agents and brokers stay current on real estate industry changes by voluntarily taking continuing education every four years, even if exempt. Order your first tuesday continuing education course by phone at 951-781-7300 or online at firsttuesday.us.

Related topics:

70/30 exemption, continuing education (ce), department of real estate (dre), dre, license

Change the law: Require a statement disclosing an SFR’s operating expenses

Change the law: Require a statement disclosing an SFR’s operating expenses somebodyPosted by ft Editorial Staff | Jul 30, 2018 | Change The Law, Laws and Regulations, Real Estate, Your Practice | 11

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Our proposal: Mandate sellers disclose to prospective buyers the full cost of owning and operating a single family residence (SFR).

Why: Currently, disclosure of a property’s estimated operating costs are customary for income properties through the Annual Property Operating Data sheet (APOD), but rarely discussed for owner-occupied SFRs. In the context of income property sales, the APOD discloses expected maintenance and operating expenses to help the investor-buyer determine whether the investment is worthwhile.

However, buyers of residential property are not typically provided the same analysis to understand the full scope of their investment as homeowners. Yet, much like an income property, a residential household is a heavy consumer of electricity, gas and other fuel sources. The existence and cost of utilities consumed by a home are material facts a prospective buyer needs sufficient information about to consider before purchasing. Thus, an SFR’s estimated operating and maintenance expenses need to be required as critical information affecting the cost and desirability of the property.

First-time homebuyers transitioning from renting are especially in need of this analysis to understand the full costs of owning and operating a home before committing to a purchase. Utility costs may make a difference for a budget-conscious buyer who is unfamiliar with the costs of maintaining a home.

Further, mandating an operating expense disclosure places little burden on an agent, since operating costs are readily available and providing the disclosure helps an agent meet their duty to a buyer.

What you can do: Though disclosing an SFR’s operating costs is not currently mandated, you can still provide the disclosure as part of the marketing package provided to prospective buyers. Use Form 306 – Property Expense Profile by Realty Publications, Inc. (RPI) to disclose operating costs to buyers. [See RPI Form 306]

The form discloses the costs of:

- utilities, such as gas, water, phone, internet and electricity;

- lawn and gardening;

- homeowner association (HOA) fees;

- property taxes;

- insurance; and

- expected maintenance and repairs.

As a buyer’s agent, discussing the content of the form with your buyer client will provide a more comprehensive analysis of the property and better prepare them for homeownership.

Related topics:

property disclosures, property expense profile

Change the law: Require disclosure of criminal activity on SFR sales

Change the law: Require disclosure of criminal activity on SFR sales somebodyPosted by ft Editorial Staff | Jan 23, 2018 | Change The Law, Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Our proposal: Mandate all sellers of single family residences (SFRs) to disclose to buyers known criminal activity and crime data in the neighborhood for the past two years.

Why: While sellers and seller’s agents are required to respond truthfully and fully to buyer inquiries about their knowledge of criminal activity, current California law does not require the disclosure of known criminal activity or impose a duty on the seller’s agent to seek out this information by checking local sources.

Yet, criminal activity is a material fact that adversely affects the value and desirability of a property, much like natural hazards, environmental hazards and property defects — all of which are legally-mandated to be disclosed to buyers.

Local crime rates are a major consideration for many homebuyers evaluating properties. In fact, a recent first tuesday poll found, according to agents, low crimes rates topped the list as the most important factor for homebuyers searching for a home, even surpassing quality schools and proximity to work.

Failure to disclose known security conditions and criminal activity on or near a property results in asymmetry of information between the seller and buyer. This lack of transparency leaves the buyer knowing less about the property than the seller and the seller’s agent, preventing the buyer from making an informed offer.

Further, local crime data is readily available through local law enforcement and other online sources, such as CrimeReports, NeighborhoodScout and My Local Crime. Giving notice to prospective buyers requires little effort compared to the value of the service to the public and satisfaction of buyers.

What you can do: In the meantime, real estate agents need to be attentive to buyer concerns regarding local crime rates. As a buyer’s agent, you can request sellers to disclose known information about local criminal activity to reduce the risk of deceitful conduct claims by an ill-informed buyer. As a seller’s agent, the best practice for complying with licensing duties is to disclose crime information to a prospective buyer by using a form designed for this very purpose.

RPI Form 321 – Seller’s Neighborhood Security Disclosure — Addendum may be used when preparing a marketing package with information addressing security on or about a property listed for sale or lease. [See RPI Form 321]

For the buyer, the Seller’s Neighborhood Security Disclosure is an addendum to the purchase agreement, attached as part of a contingency provision requesting security information from the seller on their property and surrounding area.

Each section on the form contains a separate principle relating to the security of the occupants of the property, which include:

- a statement from the sellerdisclosing any investigative reports on the adequacy of the property’s security arrangements [See RPI Form 321 §2];

- security precautions already undertaken, including steps taken by the seller or prior owner to prevent security breaches [See RPI Form 321 §3];

- conduct on the property which has endangered another person or the property of another [See RPI Form 321 §4]; and

- any other specific criminal activity occurring during the past two years. [See RPI Form 321 §5]

When a buyer’s agent reviews the Seller’s Neighborhood Security Disclosure with their buyer, the buyer’s agent may discuss disclosures or findings they have made with the buyer, along with any costs of providing additional security for their use of the property.

Related topics:

homebuyers, material fact, sellers

Change the law: Require financial literacy for high schoolers

Change the law: Require financial literacy for high schoolers somebodyPosted by ft Editorial Staff | Sep 24, 2018 | Change The Law, Economics | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Our proposal: We propose to require mandatory financial literacy education for California high schoolers. The improved financial readiness will result in better household management, which lends itself to a sounder economy for future generations.

Why: Possessing financial literacy prepares an individual to contribute to society in a financially responsible way. However, California is one of only five states in the nation with no personal finance education requirements, according to the Council of Economic Education.

Students aren’t allowed to graduate entirely ignorant of financial matters, though. Economics is required as a one-semester course in high school, covering a wide range of topics in a short period of time. Topics include macro- and micro-economic concepts, the government’s role in the economy, the impacts of globalization on the U.S. economy and the significance of financial literacy. No specific personal finance topics are required to be covered.

On the other hand, financial literacy education covers a range of necessary skills, from writing a check to saving for retirement and budgeting for a home purchase. The results are beneficial for individuals and the broader economy, as the Council of Economic Education reports students from states with required personal finance courses have higher credit scores and a lower probability of becoming delinquent as young adults.

Further, the connection between financial literacy and the housing market is easy to make. Individuals who know how to save, keep their debt load in check and balance a personal budget are much more likely to become successful homeowners.

What you can do: Other than showing up at the polls, real estate professionals can’t do much to influence state education standards. But agents can make sure their clients are financially informed during their home buying and selling process.

Do this by taking the following steps with homebuyers — especially first-time homebuyers who are completely new to the real estate transaction process:

- Discuss the need for a down payment and the consequence of mortgage insurance when the down payment is less than 20% of the purchase price.

- Go over the mortgage financing options available to the homebuyer, which affect their homebuying budget and monthly mortgage payment.

- Shed light on the effect of other debts on their total debt-to-income ratio (DTI), which influences the amount of home principal for which they qualify. It may make more sense for the homebuyer to pay down some of their other high-interest debt before applying for a mortgage.

- Discuss the cost of utilities, property taxes, homeowners’ association (HOA) fees and home maintenance that are not included in the mortgage payment. Some homebuyers neglect these costs when planning their home purchase, to their great detriment down the road when they can’t keep up with unexpected costs. This is particularly true of first-time homebuyers who aren’t accustomed to covering maintenance costs themselves.

Related article:

Need inspiration, or feel uncertain yourself about certain financial topics? The Consumer Financial Protection Bureau (CFPB) has a variety of clear and simple publications, covering reverse mortgages, refinancing procedures and the homebuying process. first tuesday also has a number of forms free for download for you to complete with your clients, including a mortgage shopping worksheet which assists homebuyers to easily compare mortgage terms. [See RPI Form 312]

Related topics:

financial literacy

Change the law: Require operating expense disclosure for SFR sales

Change the law: Require operating expense disclosure for SFR sales somebodyPosted by ft Editorial Staff | Dec 24, 2018 | Change The Law, Home Sales, Real Estate | 7

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Our proposal: We propose to require a statement disclosing the operating expenses a potential homebuyer may expect when purchasing a specific single family residence (SFR).

Why: Prospective homebuyers — especially first-time homebuyers — need to be informed about the full cost of owning and operating a home prior to purchase.

Some dollar amounts are readily available to a homebuyer, such as their potential mortgage payment, taxes, insurance and any homeowners’ association (HOA) fees. But other information is unknowable without the seller’s willingness to share their personal knowledge of the property. This information includes the average costs of:

- monthly utilities in each season;

- landscaping;

- pool maintenance, if applicable;

- water, sewage and trash;

- any bonds or assessments; and

- optional services present in the home, such as:

- a home security system; or

- a solar lease. [See RPI Form 306]

Since these costs can vary depending on the property, the true monthly cost of homeownership may affect how much a buyer is willing to pay for the property. In other words, these costs ought to be considered material facts and thus disclosed.

In practice, this disclosure would be similar to the Annual Property Operating Data (APOD) Sheet ubiquitous in transactions for income-producing property. [See RPI Form 352]

We propose this disclosure be delivered to a potential homebuyer as soon as practicable, and at latest upon commencement of negotiations.

Under our proposal, it is the seller’s agent’s role to guide their seller client through the process of collecting this information and filling out the disclosure, as well as ultimately delivering it to the prospective buyer.

While the disclosure of operating costs is not currently mandated, real estate agents and brokers may choose to use RPI Form 306: Property Expense Profile to disclose this information in any transaction. Seller’s agents may elect to include it as part of their marketing package to potential buyers. Alternatively, buyers will find it useful to request the seller fill out a property expense profile in order to get a firmer grasp of the true costs associated with owning a particular home.

Greater transparency will ensure more informed — and more successful — homeowners in the future.

Related article:

Related topics:

homeownership costs, homeowners’ association (hoa)

Change the law: Start a down payment savings program for first-time homebuyers in California

Change the law: Start a down payment savings program for first-time homebuyers in California somebodyPosted by ft Editorial Staff | Oct 22, 2018 | Change The Law | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Our proposal: We propose Californian’s legislature create a program to allow future first-time homebuyers to set up savings accounts specifically to be used for down payments.

Why: In the aftermath of the 2008 recession, slow wage growth and high rents have crippled Californians’ ability to save. This is especially true in the state’s most populous coastal cities, where the average renter spends nearly half of their income on rent.

Nationwide, 68% of would-be homebuyers cite saving for a down payment as the biggest obstacle to homeownership, according to Zillow.

Much like a health savings account (HSA) operates, these accounts will:

- accept tax-free income as deposits;

- accrue tax-free interest; and

- have the opportunity for employers to make tax-free contributions.

These types of savings accounts will reduce state tax revenue. But they will promote homeownership for more qualified residents, which is ultimately a boon for a more stable housing market and the state’s economy.

For perspective, California’s homeownership rate is one of the lowest in the nation, averaging below 55% in the decade following the 2008 recession, about ten percentage points below the national average.

Helping renters save up to become homeowners is much preferred to other solutions to California’s low homeownership rate. For example, many first-time homebuyers receive assistance in the form of down payment gifts from relatives. Still others put down as little as 3% of the purchase price on their first home.

These tactics prevent skin-in-the-game, making it more likely for homeowners to fall underwater and default.

But a tax-free down payment savings program allows homebuyers to use their own money. The main difference is that they can grow their savings more quickly so they will be able to put down more money, sooner.

What you can do: Real estate professionals can encourage renters to save for a down payment by using their marketing campaigns to target large rental communities.

Compile a selection of marketing materials aimed specifically at renters and include these rental communities at least once a month on your regular FARM schedule. Unlike current homeowners, renters are essentially “up for grabs” in the real estate world, so becoming known as the local first-time homebuyer expert will steadily increase your clientele in the coming years.

Editor’s note — Members of first tuesday’s CalPaces program for brokers with 16 or more agents have access to the free first-time homebuyer guide, a valuable resource for anyone new to real estate.

Check out first tuesday’s full selection of free, personalized FARM letters here.

Related article:

Related topics:

down payment, first-time homebuyer, savings

Change the law: amend zoning laws to promote multi-family construction

Change the law: amend zoning laws to promote multi-family construction somebodyPosted by ft Editorial Staff | May 21, 2018 | Change The Law, Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Our proposal: Reform zoning regulations to allow for more mixed-use and multifamily housing developments.

Why: California is home to 12% of the U.S. population but only 10% of the U.S. housing stock, according to the U.S. Census. Though the disparity seems relatively small, it translates to hundreds of thousands of missing units needed to meet demand from homeowners and renters.

Strict zoning regulations that limit the amount and type of construction are a significant hindrance to resolving this housing shortage. In California, zoning restrictions result in:

- reduced construction, especially residential;

- failure to meet high demand for housing;

- inflated prices of new and resale homes;

- a diminished quality of life for households as a majority of their income is directed towards excessive housing costs;

- an unstable housing market as home prices rise and incomes are unable to support the housing needs of a growing population; and

- stunted homeownership and home sales.

California now has the second-highest home sale prices in the nation, exceeded only by the District of Columbia, according to Trulia. Further, California’s homeownership rate averaged a low 54.4% in 2017, well below the U.S. average homeownership rate of 64%.

Allowing for more residential construction will help meet excess demand and organically keep rents from escalating beyond the reach of long-term neighborhood residents. Additionally, more residents moving to the area is a boon to local businesses, local tax revenues and commercial startups.

The solution to the inventory shortage is progressive zoning reform to pave the way for increased construction. Zoning amendments need to include:

- higher density and height parameters to allow for larger multi-unit properties;

- more residential zones in urban areas; and

- expansion of mixed-use zoning to promote residential development in close proximity to commercial and retail properties.

Changing zoning ordinances to allow for the construction of high-rise residential properties in city centers will bring both rents and prices down. These changes will further facilitate economic growth as residents are able to live where they work, and gain access to a wide array of services and amenities.

What you can do: Though the solution requires a combined effort from builders and government, one significant factor is the support and opposition from community members. Local efforts to enact zoning changes are often met with vocal not-in-my-backyard (NIMBY) advocates who seek to preserve their neighborhood’s “character” by limiting density and building height.

NIMBYs tend to be the only ones who let their voices be heard by attending city council meetings and opposing proposed developments.

Yet, as a real estate professional, you also have a stake in zoning regulations and development in your local community. It is imperative to get involved in making sure NIMBYs are not the only ones heard by:

- attending council meetings;

- discussing the need for zoning changes with other professionals in the industry; and

- showing support for progressive zoning reform.

New housing development is needed to revive and sustain California’s housing market — and your success as a real estate licensee. Make sure it doesn’t get blocked by neighborhood residents who have not seen the full picture.

Related topics:

construction, demand, development, homebuyers, housing, housing crisis, housing shortage

Change the law: apply use of the Agency Law Disclosure to all property transactions

Change the law: apply use of the Agency Law Disclosure to all property transactions somebodyPosted by ft Editorial Staff | Jun 19, 2018 | Change The Law, Fundamentals, Laws and Regulations, Real Estate, Your Practice | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Our proposal: Mandate use of the Agency Law Disclosure on all property transactions, including the sale of properties with five or more residential units.

Why: In 1988, the California legislature enacted the agency disclosure law to address misconceptions long held by licensees and the public about the duties real estate licensees owe to members of the public, including:

- the general dutiesowed by each broker and their agents to all owners and users in the transaction, requiring them to be honest and avoid deceitful and misleading conduct with those who are not their clients; and

- the special or primary agency dutiesowed by a broker and their agents to their client, known as fiduciary duties.

Real estate agents are now required to provide the Agency Law Disclosure to all participants when listing, selling, buying or leasing for a term greater than one year:

- property containing one-to-four residential units;

- mobilehomes; and

- commercial property. [Calif. Civil Code §§2079.13(j), 2079.14]

The Agency Law Disclosure form restates pre-existing codes and case law on agency relationships of licensees acting on behalf of another person in real estate transactions. [See RPI Form 305]

Further, the disclosure defines and explains the universal words and phrases used in nearly every transaction in the real estate industry to express:

- the agency relationships of brokers to the owner and user in the transaction;

- broker-to-broker relationships; and

- the employment relationship between brokers and their agents.

The real estate agency disclosure law previously applied only to one-to-four unit residential sales and leases. It was expanded to include commercial real estate sales and lease transactions effective January 1, 2015.

However, multi-family apartment sales of five or more units remain outside the agency disclosure law. Yet, agency is an integral component of these transactions and necessitates the same disclosures as residential and commercial sales.

The expansion of agency law disclosures to sales transactions involving multi-family apartments adds a new layer of protection for participants in these excluded transactions.

Use of the Agency Law Disclosure form for all property types ensures a participant in a transaction knows whether the individual agent handling the transaction is a dual agent, their agent exclusively, or the owner’s exclusive agent with no duty to advise or act on the participant’s behalf.

Further, including the Agency Law Disclosure in transactions for all property types – apartments included – works in the best interests of clients and their agents. Written disclosures eliminate later disputes over agency that may arise. More importantly, written disclosures have a far greater effect on agent conduct to better inform clients on other issues.

Related article:

https://journal.firsttuesday.us/agency-law-for-commercial-brokers-shedd…

What you can do: While the Agency Law Disclosure is not required for the sale of multi-family apartments, consider voluntarily providing the disclosure to participants in these transactions to ensure greater transparency. Use of the form will not only keep your clients informed about the agency relationships in their transactions, but will also help eliminate later disputes over agency duties.

Further, ensure you meet your legal duty to provide the Agency Law Disclosure in all covered transactions, including the sale of one-to-four unit residential and commercial properties.

Be aware that failure to provide the Agency Law Disclosure form prior to entering into the listing agreement for the sale or lease of a covered property is a violation of real estate law. As a consequence, your broker stands to lose their fee on a sale or lease when challenged by a client prior to closing, and faces disciplinary action by the California Department of Real Estate (DRE).

Remain compliant with agency disclosure laws through use of RPI (Realty Publications, Inc.) Form 305 – Agency Law Disclosure. To cover the distinctions in terminology between sales and leasing transactions, RPI publishes two different versions of the Agency Law Disclosure form to enhance comprehension.

Each version contains language engineered to best identify the participants involved in the two sets of transactions:

- the sale or exchangeof any real estate [See RPI Form 305]; or

- the lease for a period exceeding one year[See RPI Form 305-1 and 550-2]

Editor’s note —Two identical versions of the Agency Law Disclosure exist for leasing to place the form in both the “disclosure” and “property management” series of RPI forms. Either may be used when negotiating a listing, offer/letter of intent (LOI) or agreement for the lease of real estate for a period greater than one year. [See RPI Form 305-1 and 550-2]

Related topics:

agency law disclosure

Change the law: close Prop 13’s corporate loophole

Change the law: close Prop 13’s corporate loophole somebodyPosted by ft Editorial Staff | Aug 20, 2018 | Change The Law, Laws and Regulations, Real Estate, Tax | 6

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Our proposal: Amend Proposition 13 (Prop 13) to trigger property reassessment when an entity owning a property transfers at least 20% of the ownership interest in the entity, thereby ensuring commercial property owners and wealthy investment groups pay their equitable share of local taxes.

Why: Prop 13, also known as the People’s Initiative to Limit Property Taxation, was voted into California’s Constitution in 1978. It caps property taxes at 1% of the property’s assessed value and limits annual increases to 2%.

The property is reassessed upon a change in ownership. Here, the county assessor establishes a new base value equal to the value of the property at the time of transfer, which remains with the property until the next transfer.

However, not all transfers trigger reassessment.

One significant exclusion from Prop 13 reassessment is the change of ownership interest in a limited liability company (LLC) — or other legal entity — which does not constitute a change in ownership of the real estate owned by the entity, unless more than 50% of the membership interest is transferred to a single individual or entity. [Calif. Revenue & Tax Code §64]

Thus, an entity vested in title to real estate may strategically divide the sale of its membership interests to successfully transfer ownership of a property for all purposes, except the vesting, outside of the porous radar of Prop 13.

This allows buyers of property vested in corporations, LLCs and partnerships to avoid paying their fair share of property taxes, depriving communities of millions in tax revenue.

In stark contrast to investors of income properties, homebuyers are bound to pay property taxes based on the current value of a home on the date they purchase it. Unlike investors, homeowners are typically unable to fractionalize their acquisition of ownership.

With change of ownership being a key to property reassessment, amending how a change in ownership is defined under Prop 13 is crucial. For the many income property owners (and their attorneys) privy to Prop 13’s ambiguous change-of-ownership rules, Prop 13 merely acts as an assessment pass-through. Owners take title to a property in the name of a tax-free entity in increments of 50% or less to avoid reassessment — the perfect tax haven for those wealthy and primed on how to exploit tax loopholes, while homebuyers continue to foot the property tax bill. Closing the loophole will ensure corporations and investment owners rightfully pay their property taxes, and contribute to their communities.