2020

2020 somebody2020 ballot initiative seeks to expand rent control in California

2020 ballot initiative seeks to expand rent control in California somebodyPosted by Carrie B. Reyes | Jun 16, 2020 | Feature Articles, Laws and Regulations, Property Management | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

November 2020 update: Proposition 21, which sought to expand local governments’ ability to enact rent control laws, was defeated at the ballot box.

Rent control — the controversial solution to California’s rental shortage and rapidly escalating rents — is up for debate again.

Rent control keeps rents from rising beyond the financial abilities of long-term tenants. In theory, rent control creates more stable neighborhoods since tenants won’t be forced out due to rising rents, especially in neighborhoods where gentrification is occurring.

Rent control laws are broadly governed at the state level through the Costa-Hawkins Rental Housing Act (Costa Hawkins) and adapted through local rent control ordinances by individual cities.

In 2018, voters rejected Proposition 10, which would have repealed Costa Hawkins and allowed local governments to take rent control into their own hands. Just two years later, another ballot measure has qualified to appear on the 2020 ballot, titled the California Local Rent Control Initiative or the Rental Affordability Act. This newest measure seeks to rollback certain parts of Costa Hawkins, while leaving much intact.

Under Costa Hawkins, local rent control measures are prohibited for housing units:

- with single titles, like:

- single family residences;

- condo units;

- townhomes; and

- first occupied on or after February 1, 1995.

Thus, Costa-Hawkins only permits local governments to enact rent control measures on a limited number of older multi-family units. This has become a big problem in recent years, as the number of residents who can benefit from rent-controlled housing continues to rise with our growing population, while the number of units eligible for rent control remains static.

The 2020 ballot initiative changes the law by instituting an active date that moves with the calendar. It allows local governments to enact rent control measures on units:

- first occupied within 15 years prior to the date the landlord seeks to establish the initial or subsequent rent rate; and

- owned by natural persons who own no more than two separate-title housing units, like:

- SFRs;

- condos; and

- some townhomes or duplexes.

This measure is a nod to 2018’s Prop 10, meeting the voters who rejected it halfway.

Rent control’s promises

2020’s ballot measure seeks to add more units to the inventory of rent-controlled housing. Additional qualified housing would help millions of low-income residents who are unable to find affordable housing.

This need is evidenced by California’s worsening housing crisis. For reference, the state is home to 12% of the U.S. population, but 22% of the nation’s homeless population, according to the California Department of Housing and Community Development.

However, rent control is a quick fix to a complex issue. Like most quick fixes, it does not hold up in the long run and can do more harm than good.

Perhaps the biggest issue created by rent control is that landlords of rent-controlled apartments have no reason to maintain or improve their properties. Their only duty is to maintain habitable living conditions, and beyond that, any improvements made won’t provide the landlord any return. This leads to decaying rent-controlled units, blighting neighborhoods and making life harder for tenants.

A 2019 Stanford study looked into the impact of rent control on San Francisco’s rental housing market and found rent control did help low-income renters remain in their homes. But this was achieved at the cost of a:

- 20% decrease in mobility for renters of rent-controlled units; and

- 15% decrease in rental housing stock in the city.

Better than rent control

There is a more desirable alternative to rent control: simply put, more rental housing.

Our state’s rental housing crisis is responding to an acute imbalance between low-tier rental supply and demand for this type of housing.

California’s legislature has made several steps toward increasing the low-tier housing stock in recent years, including:

- adjusting how local governments determine housing need;

- authorizing the creation of accessory dwelling units (ADUs) in areas zoned for SFRs;

- removing parking requirements in areas near public transit;

- tightening rules regarding landlord conduct during Ellis Act evictions; and

- streamlining zoning and permitting approvals for low-income housing developments.

While these steps are all positive moves toward providing more low-tier housing, they have thus far been insufficient — and rent control is not the final answer lawmakers are searching for.

The solution requires a combined effort from builders and government. But local efforts to enact zoning changes are often met with vocal not-in-my-backyard (NIMBY) advocates who seek to preserve their neighborhood’s “character” by restricting building height and density.

NIMBYs tend to be the most vocal — and sometimes the only — voices at city council meetings whenever proposals to increase low-tier housing in the area come up.

Yet, as a real estate professional, you also have an equal stake in zoning regulations and development in your local community. You can help by getting involved and making sure NIMBYs’ concerns are balanced by the real need to increase housing and decrease the strained reliance on outdated rent control measures by:

- attending council meetings;

- discussing the need for zoning changes with other professionals in the industry; and

- showing support for progressive zoning reform.

Related article:

Related topics:

costa hawkins, rent control

2020’s Tenant Protection Act Part I: Just cause eviction

2020’s Tenant Protection Act Part I: Just cause eviction somebodyPosted by ft Editorial Staff | Jun 22, 2020 | Feature Articles, Forms, New Laws, Property Management | 19

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

This article is part I of a two-part series covering California’s Tenant Protection Act. This first part goes over just cause eviction laws. For information on the new rent caps enacted by the TPA, see Part II.

This past fall, Assembly Bill (AB) 1482 enacted California’s Tenant Protection Act (TPA) of 2019. The law made several significant changes pertaining to landlords and tenants, which will impact landlord practice in a big way going forward.

These changes will be effective until they are repealed on January 1, 2030. [Calif. Civil Code §1946.2(j)]

Who the TPA impacts

The applicability of the TPA is comprehensive, covering most multi-unit residential real estate housing in California and those single family residential (SFR) units owned by a REIT, a corporation or an LLC with a corporate member. However, there are numerous, sizable exemptions for multi-family units and conditions for SFRs to be excluded.

Properties exempt from the TPA

Multi-unit residential real estate exempt from the “just cause” eviction procedures include:

- residential units that have been issued a certificate of occupancy within the previous 15 years;

- a duplex of which the owner occupied one of the units as their principal residence at the beginning of the tenancy and remains in occupancy;

- units restricted as affordable housing for households of very low, low, or moderate income, or subject to an agreement that provides subsidies for affordable housing for households of very low, low, or moderate income;

- dormitories constructed and maintained in connection with any higher education institution in California;

- units subject to rent or price control that restricts annual increases in the rental rate to an amount less than that set by the TPA;

- multi-unit transient occupancy housing like hotels and motels;

- accommodations in which the tenant shares kitchen or bathroom facilities with an SFR owner-occupant;

- SFR real estate that can be sold and conveyed separate from the title to any other dwelling unit, like in a SFR subdivision or condominium project, provided:

- the owner is not one of the following:

- a real estate investment trust (REIT);

- a corporation; or

- a limited liability company (LLC) in which at least one member is a corporation; and

- the tenant has been given written notice stating the rental property is exempt from the rent increase caps under the TPA. [CC §1947.12(d); CC §1946.2(e); See RPI Form 550, 551 and 550-3]

- the owner is not one of the following:

To notify the tenant of the property’s exempt status from the TPA, the landlord uses a checkbox in the rental or lease agreement to indicate whether the property is subject to just cause eviction requirements with the following statutory language:

[] This property is not subject to the rent limits imposed by Section 1947.12 of the Civil Code and is not subject to the just cause requirements of Section 1946.2 of the Civil Code. This property meets the requirements of Sections 1947.12(c)(5); (d)(5) and 1946.2 (e)(7); (e)(8) of the Civil Code and the owner is not any of the following:

(1) a real estate investment trust, as defined by Section 856 of the Internal Revenue Code;

(2) a corporation; or

(3) a limited liability company in which at least one member is a corporation. [See RPI Form 550 §10.1 and Form 551 §9.1]

For tenancies entered into prior to July 1, 2020 which do not include the notice, the landlord will provide the notice and, if applicable, indicate their exempt status using the separate Just Cause and Rent Cap Addendum, doing so no later than August 1, 2020. [See RPI 550-3]

When a residential property or tenancy does not meet any of the criteria for exemption, the landlord is to abide by the TPA limiting their ability to increase the rent or evict a tenant to regain possession.

Landlords exempt from the TPA requirements may continue to use all existing RPI forms, as these are unchanged by the TPA.

What the TPA does

Broadly, the TPA:

- caps annual rent increases at 5% plus the rate of inflation for much of California multi-unit residential properties; and [See Part II of this series, forthcoming]

- requires “just cause” to evict tenants in place for 12 months or more.

Requiring a just cause for eviction makes it far harder for landlords to evict tenants in order to rent out their properties to new tenants at a higher rate. Further, if a tenant is being evicted at no fault of their own, the landlord may also be required to provide modest financial relocation assistance.

In response this change in tenant notice procedure, RPI (Realty Publications, Inc.) has published a new library of landlord-tenant forms to be used by landlords of properties subject to TPA limitations and procedures.

The new forms include the:

- Just Cause and Rent Cap Addendum [See RPI Form 550-3];

- 60-Day Notice to Vacate Under a No-Fault Eviction – For Properties Subject to Just Cause Eviction Requirements [See RPI Form 569-2];

- 30-Day Notice of Change in Rental Terms – For Properties Subject to Rent Cap Requirements [See RPI Form 570-1];

- Three-Day Notice to Quit – For Properties Subject to Just Cause Eviction Requirements [See RPI Form 577-1];

- Three-Day Notice to Pay Rent – For Properties Subject to Just Cause Eviction Requirements [See RPI Form 575-3];

- Three-Day Notice to Pay Rent with Related Fees – For Properties Subject to Just Cause Eviction Requirements [See RPI Form 575-4]; and

- Three-Day Notice to Perform – For Properties Subject to Just Cause Eviction Requirements [See RPI Form 576-1]

Further, both the residential lease and month-to-month rental agreement have been revised to be compliant for both exempt and non-exempt properties. [See RPI Form 550 and 551]

All new and revised forms are available for free download on the RPI Forms Download page.

“Just cause” required for certain evictions

For tenancies commenced or renewed on or after July 1, 2020, tenants are to be notified of the new “just cause” and rent cap protections extended to residential tenants by the TPA.

The following statutory language is to be a provision in all residential rental and lease agreements, written in no less than 12-point type:

California law limits the amount your rent can be increased. See Section 1947.12 of the Civil Code for more information. California law also provides that after all of the tenants have continuously and lawfully occupied the property for 12 months or more or at least one of the tenants has continuously and lawfully occupied the property for 24 months or more, a landlord must provide a statement of cause in any notice to terminate a tenancy. See Section 1946.2 of the Civil Code for more information.

This is incorporated as a boilerplate notice of tenant rights into RPI Form 550 §10 and Form 551 §9, our residential occupancy agreements.

Further, landlords of property exempt from the TPA need to notify the tenant in writing of their exempt status to qualify themselves for the exemption. The landlord notifies the tenant by using a checkbox in the rental or lease agreement to indicate whether the property is subject to rent limits and just cause eviction requirements. [See RPI Form 550 §10.1 and Form 551 §9.1]

For tenancies entered into prior to July 1, 2020 which do not include the notice, the landlord will provide the notice and, if applicable, indicate their exempt status using the separate Just Cause and Rent Cap Addendum, doing so no later than August 1, 2020. [See RPI 550-3]

Landlords of non-exempt property seeking to evict tenants need to show just cause when:

- all tenants have continuously and lawfully occupied the unit for 12 months or longer; or

- at least one tenant has continuously and lawfully occupied the unit for 24 months or longer. [CC §1946.2(a)]

At-fault just cause evictions

Just cause evictions notices are of two types, based on whether the tenant is:

- at fault, called an at-fault just cause eviction [CC §1946.2(b)(1)]; or

- not at fault, called a no-fault just cause eviction. [CC §1946.2(b)(2)]

An at-fault just cause eviction is further categorized as either:

- curable; or

- incurable.

To qualify for an at-fault just cause eviction, the tenant:

- defaulted on a rental payment;

- failed to enter into a landlord-requested renewal or extension of a lease which terminated on or after January 1, 2020 [See RPI Form 565];

- breached a material term of the lease;

- committed or permitted a nuisance or waste to occur on the property;

- conducted criminal activity on the premises or common areas, or used the premises for an unlawful purpose;

- assigned or sublet the premises in violation of the expired lease;

- refused the landlord’s authorized entry into the premises; or

- failed to deliver possession after providing the landlord notice to terminate the tenancy or surrender possession. [CC 1946.2(b)(1); See RPI Form 576-1]

Also classified as an at-fault just cause eviction is a tenant’s failure to vacate when the tenant was a resident manager or other employee of the landlord and their occupancy was provided in conjunction with their employment status and limited to the period of employment, and the employment has been terminated. [CC §1946.2(b)(1)(K)]

Editor’s note — When occupancy under a lease agreement expires, a landlord may require the tenant to enter into a written extension or renewal, rather than allow the tenancy to remain, converting the fixed-term tenancy to a periodic month-to-month tenancy. However, if the tenant fails to enter into a lease renewal or extension agreement and the landlord has not accepted rent for a holdover period, this is considered an at-fault just cause for eviction. [CC §1946.2(b)(1)(E)]

When the tenant under an at-fault just cause tenancy breaches a nonmonetary performance provision of a rental or lease agreement, the landlord of a non-exempt property serves the tenant a Three-Day Notice to Perform – For Properties Subject to Just Cause Eviction Requirements. [See RPI Form 576-1]

When the failure to perform is incurable – such as when a tenant commits waste to the property or engages in overt criminal activity – the landlord uses the Three-Day Notice to Quit, requiring the tenant to vacate and deliver possession within three days of service. [Calif. Code of Civil Procedure §1161(4); See RPI Form 577-1]

However, when the failure to perform is curable, such as the breach of a lease term which may be fully corrected within a three day period, the landlord uses the Three-Day Notice to Perform to state what the tenant needs to do to rectify or cure the breach in order to remain in possession. [See RPI Form 576-1 §4]

Unique to properties subject to the just cause eviction requirements, when the tenant does not cure the breach by full performance within three days after service of the notice to perform, the landlord may not immediately begin legal proceedings to regain possession by pursuing an unlawful detainer (UD) action.

Rather, if the breach remains uncured on expiration of the Notice to Perform, the landlord is required to prepare and serve the tenant with the Three-Day Notice to Quit. [CC §1946.2(c); See RPI Form 577-1]

Here, the tenant who is served a notice to correct a curable breach and fails to fully perform or quit, is given three additional days to vacate — quit — after service of the final notice. When the tenant then fails to vacate and deliver possession, the landlord’s remaining legal remedy is to file a UD action to regain possession based on the tandem quit notices and seek an award for rent owed and associated costs. [CC §1946.2(c)]

Related, when the tenant commits a curable monetary breach, in order to initiate the eviction, the landlord uses a Three-Day Notice to Pay Rent (with or without related fees). These notices include sections which identify the tenant as being under a lease which requires just cause to terminate the tenancy and indicates their failure to pay rent constitutes just cause for eviction. [See RPI Form 575-3 and Form 575-4]

Once the three days have passed and the tenant has still not paid the appropriate amount(s) – a curable breach – the landlord may serve the tenant with a Three-Day Notice to Quit without the further opportunity to cure the violation. [See RPI Form 577-1]

No-fault just cause evictions

Alternatively, a no-fault just cause eviction exists when the tenant is being evicted under no fault of their own for any of the following reasons:

- the landlord or their spouse, domestic partner, children, grandchildren, parents or grandparents intend to occupy the premises;

- the property is withdrawn from the rental market;

- the property is unfit for habitation as determined by a government agency and through no fault of the tenant; or

- the landlord intends to demolish or substantially renovate the property. [CC 1946.2 (b)(2); See RPI Form 569-2 §3]

An improvement qualifies as a substantial remodel or renovation when any structural, electrical, plumbing or mechanical system is replaced or substantially modified, requiring a permit from a government agency. This includes the abatement of hazardous materials like lead-based paint, mold or asbestos, which cannot be completed with the tenant residing in the unit, requiring the tenant to vacate for 30 days or longer.

Cosmetic improvements like painting or minor repairs that don’t require the tenant to vacate to ensure their safety are not considered substantial remodels. [CC §1946.2 (b)(2)(D)(ii)]

Recall that the notice to quit discussed above is used in the context of an at-fault eviction — the tenant has materially breached the terms of a rental or lease agreement and the landlord is using the breach to terminate the lease or rental agreement. [See RPI Form 577-1]

Alternatively, a notice to vacate is used in the context of a no-fault eviction to terminate a rental agreement and interfere with the automatic renewal of the periodic tenancy when a breach of the rental agreement has not occurred or is not an issue. [See RPI Form 569-2]

To terminate the tenancy of a residential tenant who has resided on the property for one year or more, residential landlords are required to give the tenant a 60-day notice to vacate.

Relocation assistance

Further, when a no-fault just cause eviction occurs for a non-exempt property, the landlord is required to provide relocation assistance to the tenant. Relocation assistance is equal to one month’s rent and is to be made:

- as a direct payment within 15 calendar days of the notice to vacate; or

- in exchange for the landlord’s waiver of the payment of rent for the final month before it becomes due. [CC 1946.2(d)(1); See RPI Form 569-2 §7]

Further, the landlord needs to notify the tenant of their right to relocation assistance in writing. This notice is provided within the body of the specialized 60-Day Notice to Vacate required for tenants who have resided in the property for 12 months or longer. [CC §1946.2(d)(2); See RPI Form 569-2 §7]

If the landlord fails to provide relocation assistance, the notice to vacate is void. [CC §1946.2(d)(4)]

Further, if the tenant receives the relocation assistance and then fails to vacate at the end of the notice period, the landlord is able to recover the relocation assistance as part of the damages in their action to retake possession. [CC §1946.2(d)(3)(B)]

If it was through the actions of the tenant that the property was rendered unfit for habitation, the tenant is not entitled to relocation assistance. [CC §1946.2(b)(2)(C)(iii)]

Tenants may not waive their rights provided to them under the just cause eviction laws. Any waiver made in the agreement is void as contrary to public policy.

Related topics:

eviction, tenant

2020’s Tenant Protection Act Part II: Rent caps

2020’s Tenant Protection Act Part II: Rent caps somebodyPosted by ft Editorial Staff | Jun 25, 2020 | Feature Articles, Forms, New Laws, Property Management | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

This article is part II of a two-part series covering California’s Tenant Protection Act of 2019. This second part goes over the new rent cap laws. To learn about the Act’s just cause eviction rules, see Part I.

This past fall, Assembly Bill (AB) 1482 enacted California’s Tenant Protection Act (TPA) of 2019. The law made several significant changes pertaining to landlords and tenants, which will impact landlord practice in a big way going forward.

These changes will be effective until they are repealed on January 1, 2030. [Calif. Civil Code §1946.2(j)]

Who the TPA impacts

The applicability of the TPA is comprehensive, covering most multiple unit residential real estate housing in California and those single family residential (SFR) units owned by a REIT, a corporation or an LLC with a corporate member. However, there are numerous exemptions for multiple family units and conditions for SFRs to be excluded.

Properties exempt from the TPA

Multi-unit residential real estate exempt from TPA rent caps include:

- residential units that have been issued a certificate of occupancy within the previous 15 years;

- a duplex of which the owner occupied one of the units as their principal residence at the beginning of the tenancy and remains in occupancy;

- units restricted as affordable housing for households of very low, low, or moderate income, or subject to an agreement that provides subsidies for affordable housing for households of very low, low, or moderate income;

- dormitories constructed and maintained in connection with any higher education institution in California;

- units subject to rent control that restricts annual increases in the rental rate to an amount less than that set by the TPA;

- multi-unit transient occupancy housing like hotels and motels;

- accommodations in which the tenant shares kitchen or bathroom facilities with an SFR owner-occupant;

- SFR real estate that can be sold and conveyed separate from the title to any other dwelling unit, like in a SFR subdivision or condominium project, provided:

- the owner is not one of the following:

- a real estate investment trust (REIT);

- a corporation; or

- a limited liability company (LLC) in which at least one member is a corporation; and

- the tenant has been given written notice stating the rental property is exempt from the rent increase caps under the TPA. [CC §1947.12(d); CC §1946.2(e); See RPI Form 550, 551 and 550-3]

- the owner is not one of the following:

To notify the tenant of the property’s exempt status from the TPA, the landlord uses a checkbox in the rental or lease agreement to indicate whether the property is subject to rent limits and just cause eviction requirements. [See RPI Form 550 §10.1 and Form 551 §9.1]

For tenancies entered into prior to July 1, 2020 which do not include the notice, the landlord will provide the notice and, if applicable, indicate their exempt status using the separate Just Cause and Rent Cap Addendum, doing so no later than August 1, 2020. [See RPI 550-3]

When a residential property or tenancy does not meet any of the criteria for exemption, the landlord is to abide by the TPA limiting their ability to increase rent.

Landlords exempt from the TPA requirements may continue to use all existing RPI forms, as these are unchanged by the TPA.

What the TPA does

Broadly, the Tenant Protection Act of 2019:

- caps annual rent increases at 5% plus the rate of inflation for much of California multi-unit residential properties; and

- requires “just cause” to evict tenants in place for 12 months or more. [See Part I]

In response this change in tenant notice procedure, RPI (Realty Publications, Inc.) has drafted a new library of landlord-tenant forms to be used by landlords of properties subject to TPA limitations and procedures.

The new forms include the:

- Just Cause and Rent Cap Addendum [See RPI Form 550-3];

- 60-Day Notice to Vacate Under a No-Fault Eviction – For Properties Subject to Just Cause Eviction Requirements [See RPI Form 569-2];

- 30-Day Notice of Change in Rental Terms – For Properties Subject to Rent Cap Requirements [See RPI Form 570-1];

- Three-Day Notice to Quit – For Properties Subject to Just Cause Eviction Requirements [See RPI Form 577-1];

- Three-Day Notice to Pay Rent – For Properties Subject to Just Cause Eviction Requirements [See RPI Form 575-3];

- Three-Day Notice to Pay Rent with Related Fees – For Properties Subject to Just Cause Eviction Requirements [See RPI Form 575-4]; and

- Three-Day Notice to Perform – For Properties Subject to Just Cause Eviction Requirements [See RPI Form 576-1]

Further, both the residential lease and month-to-month rental agreement have been revised to be compliant for both exempt and non-exempt properties. [See RPI Form 550 and 551]

All new and revised forms are available for free download on the RPI Forms Download page.

Rent caps enacted by the TPA

The TPA enacts a limitation on rent increases for non-exempt residential rental properties.

For rent increases occurring on or after March 15, 2019, an owner of residential real property may not, over the course of any 12-month period, increase the gross rental rate for a unit more than the lesser of:

- 5% plus the percentage change in the applicable Consumer Price Index (CPI); or

- 10% of the lowest gross rental rate charged for that dwelling or unit at any time during the 12 months prior to the effective date of the increase. [CC §1947.12(a)(1); CC §1947.12(h)(1)]

How does a landlord go about properly raising rents under the TPA?

The landlord provides the tenant of a month-to-month rental agreement with a 30-day Notice of Change in Rental Terms – For Properties Subject to Rent Cap Requirements. Notice of the limitations on rental increases is included in this variation of the 30-Day Notice of Change. [CC §1947.12(e); See RPI Form 570-1]

Calculating rent increases

When calculating rent increases, rent discounts or credits are not included. [CC §1947.12(a)(1)]

The cost of living adjustment is considered to be from April 1st of the previous year to April 1st of the current year in the regional CPI for the region where the rental property is located. This information is published by the Bureau of Labor Statistics.

When a regional index is not available — as is the case for rentals located in smaller metros and rural areas — the index used is the California Consumer Price Index for All Urban Consumers for all items, published by the Department of Industrial Relations. These numbers can be found on the California Department of Industrial Relations’ website, here.

If a landlord has already increased the rent by more than is allowed under the TPA between March 15, 2019 and January 1, 2020, the landlord needs to revert the rent amount as of January 1, 2020 to the rent amount charged as of March 15, 2019, plus the maximum permissible increases.

Further, the landlord is not held responsible for any corresponding overpayment in rent. [CC §1947.12(h)(2)]

Further, for tenancies beginning or renewed on or after July 1, 2020, any written notice informing tenants their rental is exempt from the rent increase caps needs to be included in their lease or rental agreement. [CC §1947.12(b)(5)(B)(ii); See RPI Form 550 §10.1 and 551 §9.1]

For new tenancies — when no tenant remains from the prior tenancy — the landlord may establish the initial rental rate as they choose, limited only by current market factors and sound economic reason. However, subsequent increases throughout the duration of the tenancy are subject to the rent increase caps. [CC §1947.12(b)]

Related topics:

landlords and tenants, real estate forms, rent control

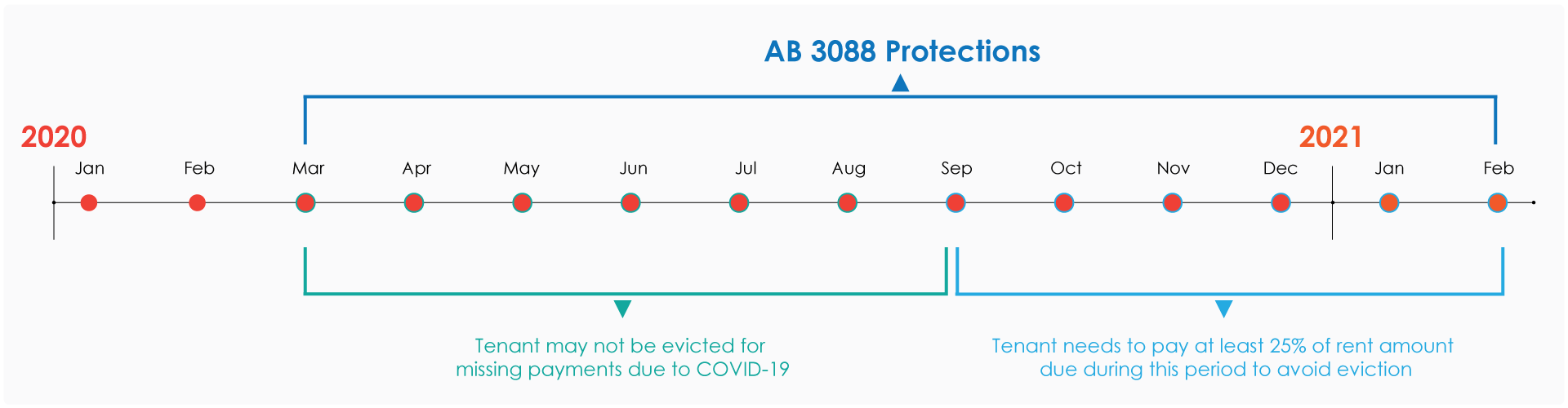

AB 3088: New eviction protections to last through January 2021

AB 3088: New eviction protections to last through January 2021 somebodyPosted by Emily Kordys | Sep 8, 2020 | Laws and Regulations, Real Estate | 3

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

This article is a first in a series covering AB 3088: the Tenant, Homeowner and Small Landlord Relief and Stabilization Act of 2020.

California Governor Gavin Newsom and legislative lawmakers signed a new law to halt evictions for thousands of tenants who are unable to pay rent as a result of the coronavirus (COVID-19) pandemic through January 31, 2021.

Newsom previously issued an executive order in March 2020 placing a moratorium on evictions through the end of May. The order was extended two separate times, with California’s Judicial Council voting in August to end it on September 1, 2020.

Protections for Tenants

AB 3088, also known as the Tenant, Homeowner, & Small Landlord Relief and Stabilization Act of 2020, is helping to provide temporary relief to thousands of Californians. A recent UCLA and USC study found that between 58% and 68% of tenant households in the Los Angeles area lost income since mid-March. Without the new law, renters would have been left more vulnerable since income losses are widespread throughout the state.

The bill protects renters from being evicted if they failed to make rental payments due to COVID-19-related financial distress between March 1, 2020 and January 31, 2021.

Under the new law, a tenant may not be evicted before February 1, 2021 as a result of unpaid rent related to the pandemic between March 4, 2020 and August 31, 2020. Tenants who are unable to pay rent due to COVID-19 between September 1, 2020 and January 31, 2021 must pay at least 25% of the rental payments due in that time period to avoid eviction.

For example, consider a tenant who losses their job in August due to the pandemic and is unable to pay the full amount due for rent. The tenant continues to pay 25% of their rent to their landlord each month. The tenant may not be evicted since they are paying the correct amount due, under the new law. A tenant may pay 25% each month or pay one lump sum by February 1, 2021 to avoid eviction.

Tenants are still responsible for paying all unpaid amounts to landlords.

To be eligible for the new protections, tenants need to provide a declaration of COVID-19-related financial distress to their landlord. COVID-19-related financial distress refers to:

- loss of income caused by the pandemic;

- increased out-of-pocket expenses directly related to performing essential work;

- increased expenses directly related to the health impact of the pandemic;

- child or elder care responsibilities, disabled or sick family member directly related to the pandemic that limits the ability to earn income; or

- other circumstances related to the pandemic which have reduced income or increased expenses.

Before a landlord may evict a tenant under this law, they are required to give tenants a 15-day notice that informs them of the amounts owed and include a blank declaration form to use to comply with this requirement.

Editor’s Note – RPI is currently drafting new landlord-tenant notice forms to comply with these new requirements. The new and updated forms will be posted to the Forms Download page once they are completed.

It is important for tenants to not ignore a 15-day notice to pay rent or quit or a notice to perform covenants or quit from their landlord. If a tenant is served with a 15-day notice and does not submit the declaration form before the notice expires, they may be evicted.

Tenants who make more than 130% of the area income where they live may also be required to provide additional documentation of financial hardship to their landlord.

Protections for landlords

Tenants who failed to pay rent during the specified period will have their rent balance turned into consumer debt, which can be pursued in small claims court starting March 1, 2021.

Landlords who do not follow the court evictions process will face increased penalties.

Evictions not related to unpaid rent – such as nuisance complaints or health and safety violations – may still take place.

Additionally, landlords who own fewer than four units and do not live in them will receive some foreclosure protections under the Homeowners Bill of Rights, which was passed in the wake of the late 2000’s foreclosure crisis. The rights refer to specific guidelines mortgage servicers need to obey when communicating with borrowers. It also prohibits “dual track” foreclosures, in which lenders pursue foreclosures while simultaneously negotiating loan modifications.

The new tenant and landlord protections will help to momentarily stave off the looming foreclosure crisis. More protections and laws will need to be passed as we head further into the recession.

Check back for more updates as the recession continues to impact tenants, landlords and the housing market.

Related article: Foreclosure moratorium extended by FHA, Fannie Mae, Freddie Mac

Related topics:

covid-19 pandemic, landlords, tenants

Brokerage Reminder: Home inspectors – the buyer’s choice

Brokerage Reminder: Home inspectors – the buyer’s choice somebodyPosted by ft Editorial Staff | Dec 15, 2020 | Brokerage Reminder, Buyers and Sellers, Real Estate | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

A competent seller’s agent will aggressively recommend the seller retain a home inspector before they market the property. The inspector hired will conduct a physical examination of the property to determine the condition of its component parts. On the home inspector’s completion of their examination, a home inspection report (HIR) will be prepared on their observations and findings, which is forwarded to the seller’s agent.

A home inspector often detects and reports property defects overlooked by the seller and not observed during a visual inspection by the seller’s agent. Significant defects which remain undisclosed at the time the buyer goes under contract tend to surface during escrow or after closing as claims against the seller’s broker for deceit. A home inspector troubleshoots for defects not observed or observable to the seller’s agent’s eye. [Calif. Business and Professions Code §7195]

To greatly reduce the potential of buyer claims and eliminate to the extent possible the risk of negligent property improvement disclosures, the HIR is coupled with preparation of the seller’s Transfer Disclosure Statement (TDS). Both are presented to buyers before the seller accepts an offer.

A home inspector’s qualifications

Any individual who holds themselves out as being in the business of conducting a home inspection and preparing a home inspection report on a one-to-four unit residential property is a home inspector. No licensing scheme exists to set the minimum standard of competency or qualifications necessary to enter the home inspection profession. [Calif. Business and Professions Code §7195(d)]

However, some real estate service providers typically conduct home inspections, such as:

- general contractors;

- structural pest control operators;

- architects; and

- registered engineers.

Home inspectors occasionally do not hold any type of license relating to construction, such as a person who is a construction worker or building department employee. However, they are required to conduct an inspection of a property with the same “degree of care” a reasonably prudent home inspector would exercise to locate material defects during their physical examination of the property and report their findings. [Bus & P §7196]

Hiring a home inspector

Sellers and seller’s agents are encouraged by legislative policy to obtain and rely on the content of an HIR to prepare their TDS for delivery to prospective buyers.

The buyer’s reliance on an HIR at the time a purchase agreement is entered into relieves the seller and their agent of any liability for property defects they did not know about or were not observable during the mandatory visual inspection conducted by the seller’s agent.

However, for the seller’s agent to avoid liability in the preparation the TDS by relying on an HIR, the seller’s agent needs to select a competent home inspector to inspect and prepare the HIR. Thus, the seller’s agent needs to exercise ordinary care when selecting the home inspector.

The inspection and report

A home inspection is a physical examination conducted on-site by a home inspector. The inspection of a one-to-four unit residential property is performed for a noncontingent fee.

The purpose of the physical examination of the premises is to identify material defects in the condition of the structure and its systems and components. Material defects are conditions which affect the property’s:

- market value;

- desirability as a dwelling;

- habitability from the elements; and

- safety from injury in its use as a dwelling.

Defects are material if they adversely affect the price a reasonably prudent and informed buyer would pay for the property when entering into a purchase agreement. As the report may affect value, the investigation and delivery of the home inspection report to a prospective buyer is legislated to precede a prospective buyer’s offer to purchase. [Bus & P C §7195(b)]

The home inspection is a non-invasive examination of the mechanical, electrical and plumbing systems of the dwelling, as well as the components of the structure, such as the roof, ceilings, walls, floors and foundations.

Non-invasive indicates no intrusion into the roof, walls, foundation or soil by dismantling or taking apart the structure which would disturb components or cause repairs to be made to remove the effects of the intrusion.

The home inspection report is the written report prepared by the home inspector which sets forth the findings while conducting the physical examination of the property. The report identifies each system and component of the structure inspected, describes any material defects the home inspector found or suspects, makes recommendations about the conditions observed and suggests any further evaluation needed to be undertaken by other experts. [Bus & P C §7195(c)]

Mandatory inspection by the seller’s broker

A seller’s agent (or seller’s broker) is obligated to personally carry out a competent usual inspection of the property. The seller’s disclosures and defects noted in the HIR are entered on the TDS and reviewed by the seller’s agent for discrepancies. The seller’s agent then adds any information about their knowledge of material defects which have gone undisclosed by the seller (or the home inspector).

A buyer has two years from the close of escrow to pursue the seller’s broker and agent to recover losses caused by the broker’s or agent’s negligent failure to disclose observable and known defects affecting the property’s physical condition and value. Undisclosed and unknown defects permitting recovery are those observable by a reasonably competent broker during a visual on-site inspection. A seller’s agent is expected to be as competent as their broker in an inspection. [CC §2079.4]

However, the buyer will be unable to recover their losses form the seller’s broker if the seller’s broker or agent inspected the property and would not have observed the defect and did not actually know it existed. [CC §1102.4(a)]

Following their mandatory visual inspection, the seller’s broker or agent needs to make disclosures on the seller’s TDS in full reliance on specific items covered in a home inspector’s report the seller obtained on the property. If the HIR is relied on after the seller’s agent property inspection when preparing the TDS and the TDS is later contested by the buyer as incorrect or inadequate in a claim on the broker, the broker and their agent are entitled to indemnification – held harmless – from the home inspection company issuing the report. [Leko v. Cornerstone Building Inspection Service (2001) 86 CA4th 1109]

As the buyer’s agent, remember that home inspection requests and reports are between your buyer and the inspector. Consult, assist and recommend – but leave the selecting to your buyer when you order out that home inspection – even if your buyer is a speculator.

This article was originally published in August 2013 and has been updated.

Related topics:

home inspection

California further extends DRE licensing, exam, continuing education deadlines

California further extends DRE licensing, exam, continuing education deadlines somebodyPosted by ft Editorial Staff | Jun 17, 2020 | Fundamentals, Laws and Regulations, Recessions, Your Practice | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Updated July 19, 2020 to reflect Governor Newsom’s Executive Order N-71-20.

On June 30, 2020, Governor Newsom granted an extension for California Department of Real Estate (DRE) licensees and exam applicants.

The order extends the timelines and deadlines related to:

- exam application expiration dates;

- license expiration dates;

- payment of license application fees;

- payment of renewal fees; and

- continuing education (CE) requirements.

If your license or exam application expiration date occurs after April 16, 2020, your deadlines have been extended through December 31, 2020. Under previous executive orders, the extensions gave an additional 120 days from the licensee’s original deadline or expiration. But now all deadlines have been extended through the end of 2020.

If the order applies to you, there is no need to contact the DRE for an extension, it is automatic.

Visit the DRE’s frequently asked questions page for more information.

Follow first tuesday’s full coverage of how the novel coronavirus (COVID-19) is impacting real estate here.

Related topics:

covid-19 pandemic, department of real estate (dre)

California likely has some of your money — here’s how to reclaim it

California likely has some of your money — here’s how to reclaim it somebodyPosted by ft Editorial Staff | Apr 21, 2020 | Fundamentals, Laws and Regulations, Your Practice | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

The pleasant surprise of finding a crumpled-up bill in last season’s jacket pocket is possible for your business, too. How? Through a legal process called escheat.

Escheat is the process of transferring abandoned property to the state.

For example, banks possessing an individual’s property (read: money) have a duty to return the property to the owner after three years of inactivity. [California Code of Civil Procedure §1513(a)(a)(A)]

Intangible personal property escheats to the state when:

- the last known address of the apparent owner is in California;

- no address of the apparent owner appears on the records of the holder and:

- the last known address of the apparent owner is in California; or

- the holder resides in California and has not previously paid the property to the state of the last known address of the apparent owner; or

- the holder is part of California’s government and has not previously paid the property to the state of the last known address of the apparent owner;

- the last known address of the apparent owner is in a state that does not provide by law for the escheat of such property and the holder is:

- domiciled in this state; or

- a government or governmental subdivision or agency of this state; or

- the last known address of the apparent owner is in a foreign nation and the holder is:

- domiciled in this state; or

- a government or governmental subdivision or agency of this state. [CCP §1510]

Holders of unclaimed property have a duty to notify owners of unclaimed property valued over $50 before reporting it to the state. [CCP §1520(b)]

For more information on notification requirements, holders may see guidance from the State Controller’s Office, here.

To find out if the state has money that belongs to you, visit the lookup tool at the California State Controller’s Office. However, the State Controller warns consumers not to respond to mailings prompting recipients to call a toll-free number, contact an attorney or pay any upfront fees regarding unclaimed property. These types of notices are fraudulent.

To ensure you’re not being defrauded, always go directly through the State Controller’s office. Here, anyone can access the public interface to determine whether the state holds any unclaimed property that has been escheated to the state after a period of inactivity.

Just as one regularly checks their credit score, brokers and other small business owners ought to make it a habit to periodically determine whether they have any unclaimed property with the state so they may get it back.

See additional guidance from the State Controller, here.

Related topics:

California’s definition of “essential service” has shifted for real estate professionals

California’s definition of “essential service” has shifted for real estate professionals somebodyPosted by ft Editorial Staff | Apr 28, 2020 | Fundamentals, Laws and Regulations, Market Watch, Recessions | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Even as millions of residents continue to shelter in place across California, a few industries have been identified as critical to keeping life going during the coronavirus (COVID-19) pandemic.

The following real estate and real estate adjacent professionals are classified as essential by the U.S. Department of Homeland Security:

- individuals who provide residential and commercial real estate services, including settlement services;

- government staff who perform title search, notary and recording services in support of mortgage and real estate services and transactions;

- workers who repair, install or service residential and commercial HVAC systems and other heating, cooling, refrigeration and ventilation equipment; and

- workers who provide services necessary to maintaining the safety, sanitation and essential operation of residences and buildings, including:

- plumbers;

- electricians;

- exterminators;

- builders;

- contractors; and

- landscapers.

This list is meant to be used as guidance for individual states to make their own laws about who may continue to practice during the pandemic.

State restrictions are tighter

Here in California, at first Governor Newsom’s shelter-in-place order reflected the above Homeland Security guidelines, including residential real estate service providers under the exception. In fact, most private sources continue to espouse this is still the case, with many real estate agents continuing to give in-person home tours and interact with members of the public despite the change.

However, the most recent guidance from the State Public Health Officer excludes real estate providers, limiting related essential industries to:

- construction workers; and

- workers who provide services necessary to maintaining the safety, sanitation and essential operation of residences and buildings.

However, these statewide rules follow the federal government’s lead, passing the buck along to local governments.

Cities and counties across California have issued their own rules about which professionals are critical to maintaining a safe and healthy community during the pandemic. However, at the time of this writing, most local restrictions reflect those at the state level. For example, the list of essential workers related to real estate for major cities like San Diego and Los Angeles align with the statewide list, which include workers like plumbers, electricians and construction workers, but exclude real estate agents.

Check local guidance for information on what is allowed. Further, even if your city or county allows real estate service providers to continue working during the pandemic, it’s important to follow social distancing precautions, like refraining from holding open houses and conducting virtual tours and meetings when possible.

Anyone with the ability to do so can continue to work from home without physically interacting with the public. This can be done through:

- virtual tours;

- remote signings;

- building out an online presence; and

- advancing career paths by:

- forming real estate syndicates;

- becoming a foreclosure expert;

- getting a mortgage loan originator (MLO) endorsement; or

- becoming a notary public.

Related articles:

Related topics:

covid-19 pandemic, virtual reality

DBO Bulletin Digest August 2020

DBO Bulletin Digest August 2020 somebodyPosted by Emily Kordys | Aug 17, 2020 | Finance, Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

The August 2020 DBO focuses on continuing safety compliance for coronavirus (COVID-19), the California Residential Mortgage Loan Act, additional loan accommodations related to COVID-19 and imposter scams.

The California Department of Business Oversight (DBO) supervises, licenses and regulates a variety of financial institutions, including some real estate mortgage loan originators (MLOs) holding a Nationwide Multistate (or Mortgage) Licensing System and Registry (NMLS) license. Alongside the California Department of Real Estate (DRE), the DBO shares the responsibility for overseeing MLOs depending on their license use.

Licensees, read on for the latest DBO happenings.

DBO monitoring face covering compliance

In accordance with Governor Newsom’s directive on face coverings, the DBO is reminding all licensees to ensure all employees and clients comply with the latest guidance from the California Department of Public Health (CDPH).

All clients and customers are required to wear face coverings in accordance with CDPH guidance. Those who refuse to wear masks or do not meet CDPH exemptions are not allowed to enter places of business.

The DBO conducted drive-by spot checks of branch and storefront locations to confirm compliance. These brief inspections checked for publicly visible notices and greeters providing personal protective equipment at the entrance.

Anyone with questions may email the DBO at Ask.DBO@dbo.ca.gov.

Report on the California Residential Mortgage Loan Act

The 2019 Annual Report of activity under the California Residential Mortgage Lending Act (CRMLA) provides comprehensive information on residential mortgages, rates, foreclosures and consumer complaints. The report consists of data submitted by residential mortgage lenders and servicers.

The report found the number and principal amount of loans originated by licensees increased significantly in 2019 from 2018. The number of loans in this period grew to 552,687, an increase of 51.4%. In addition, the number mortgages originated in 2019 also went up from 2018, by 37.6%.

Additional loan accommodations related to COVID-19

The Federal Financial Institutions Examination Council (FFIEC) issued a statement regarding risk management and consumer protection principles for financial institutions to consider when working with borrowers as the initial coronavirus-related mortgage accommodation periods come to an end.

The Council urges licensees to consider additional accommodations that ease pressure on affected borrowers, improve their capacity to service debt and facilitate prudent management of mortgages. To help avoid delinquencies and other adverse consequences, the FFIEC recommends:

- reassessing risk ratings for each mortgage;

- applying appropriate loan risk ratings and grades; and

- making appropriate accrual status decision on loans affected by COVID-19.

The statement also asks financial institutions to consider additional accommodations for borrowers struggling financially.

The FFIEC is an interagency body which prescribes uniform principles and standards, and reports forms for the federal examination of financial institutions by the Board of Governors of the Federal Reserve System (FRB), the Federal Deposit Insurance Corporation (FDIC), and more.

COVID-19 imposter scams

An advisory alert to financial institutions has been issued by the Financial Crimes Enforcement Network (FinCEN) regarding consumer fraud. The advisory includes descriptions of imposter scams and money mule schemes, financial red flags, and information on reporting suspicious activity.

The alert advises imposters are posing as officials and representatives from the Internal Revenue Service (IRS), the Centers for Disease Control and Prevention (CDC), the Federal Bureau of Investigation (FBI) and the World Health Organization (WHO) to target individuals directly. Some of the red flags discussed include:

- contact from a government agency by phone, email, or social media promising to process or expedite unemployment benefits in exchange for sensitive financial information;

- receiving a document that appears to be a check or a prepaid debit card from the U.S. Treasury with instructions to contact the fraudulent government agency;

- unsolicited communications from trusted sources or government programs related to COVID-19, instructing readers to open or embed links to give personal information; and

- email addresses in COVID-19 correspondence which do not match the name of the sender, contain grammatical errors or do not end in a corresponding domain such as “.gov.”

The advisory is based on COVID-19 related information taken from Bank Secrecy Act (BSA) data, open source reporting and law enforcement.

That’s a wrap on another DBO bulletin digest! As always, you can find the complete DBO bulletin on their website.

Related topics:

covid-19 pandemic

DBO Bulletin Digest January 2020

DBO Bulletin Digest January 2020 somebodyPosted by ft Editorial Staff | Jan 22, 2020 | Finance, Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

The first DBO Bulletin Digest of 2020 gets right to business with a DBO overhaul and fintech initiatives.

The California Department of Business Oversight (DBO) supervises, licenses and regulates a variety of financial institutions, including some real estate mortgage loan originators (MLOs) holding a Nationwide Multistate (or Mortgage) Licensing System & Registry (NMLS) license. Alongside the California Department of Real Estate (DRE), the DBO shares the responsibility for overseeing MLOs depending on their license use.

Licensees, read on to start your decade on the right foot.

Newsom proposes DBO revamp

Governor Gavin Newsom recently unveiled an ambitious plan to overhaul the DBO as part of California’s 2020-21 budget. The proposal is to change the Department’s name to the Department of Financial Protection and Innovation (DFPI) and expand its consumer protection role. According to the proposal, its goal is to provide consumers with more protection against unfair, deceptive and abusive practices when accessing financial services and products.

Currently, the DBO’s regulatory jurisdiction is limited to certain financial services and state-licensed financial institutions like banks, credit unions and money transmitters. Some real estate agents are already well acquainted with the DBO as it also licenses and regulates mortgage lenders, escrow agents and other commercial and consumer lenders.

To meet evolving consumer needs, the proposal expands the DBO’s regulatory powers into new and under-regulated industries, including debt collection, fintech and credit reporting. If approved by state lawmakers, the DFPI’s new offerings will include:

- consumer education on sound financial protection practices;

- licensing and examinations for new and under-regulated industries;

- market analyses to inform policy and enforcement;

- enforcing legislation that prohibits unfair, deceptive and abusive practices;

- establishing a Financial Technology (fintech) Innovation Office that develops new consumer financial products;

- providing legal support for the administration of the new law; and

- expanding existing administrative and information technology staff to support the Department’s new responsibilities.

If you’re experiencing déjà vu, you may be thinking of the Consumer Financial Protection Bureau (CFPB). In fact, the proposed DFPI is modeled after the CFPB. According to the proposal, the new Department is meant to fill a void at the federal level left by the CFPB’s rollback.

The plan still requires the approval of state lawmakers and details of its implementation are expected by February 1, 2020. In the meantime, you can read the proposal here.

CSBS Accountability Report

This month, the Conference of State Bank Supervisors (CSBS) released an Accountability Report that outlines progress made toward its Vision 2020 fintech initiatives. The Conference, which is made up of financial regulators from all 50 states, acts on recommendations by an advisory panel of fintech leaders as part of the Vision 2020 program.

Vision 2020’s main objective is to modernize state regulation through a networked system of nonbank licensing and supervision. The Accountability Report highlights a few developments toward this goal, including:

- expanding NMLS use for managing an increasing number of license types;

- increasing state regulation transparency through the CSBS State Regulatory Guidance Portal; and

- drafting a model state money services business (MSB) law to clarify activities requiring licensure.

Read the full CSBS Accountability Report here.

Reminders

The DBO issues licensees a few friendly reminders in this month’s bulletin, including one concerning Assembly Bill 857. The bill, which went into effect January 1, 2020, allows local governments to establish public banks. With this new legislation in place, the DBO stresses that establishing a bank under this law requires a DBO certificate of authorization and Federal Deposit Insurance Corporation (FDIC) insurance. Read the full bill text here.

Separately, the DBO reminds licensees that all commercial banks, industrial banks and trust companies need to file with the DBO a list of the offices they maintain and operate.

The deadline was January 1, 2020, but the DBO urges stragglers to file as soon as possible to avoid possible fines and penalties. If you have not done so already, email your filing to Licensing@dbo.ca.gov or mail to:

Department of Business Oversight

Division of Financial Institutions

Attn: Licensing & Information Reporting Office

One Sansome Street, Suite 600

San Francisco, CA 94104-4428

That’s a wrap on the first DBO Bulletin Digest of 2020! Check back next month for February’s DBO Bulletin Digest. As always, you can read the full DBO bulletin on their website.

Related topics:

department of business oversight (dbo), department of financial protection and innovation (dfpi), dfpi bulletin digest

DBO Bulletin Digest July 2020

DBO Bulletin Digest July 2020 somebodyPosted by Emily Kordys | Jul 28, 2020 | Finance, Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

The July 2020 DBO Bulletin focuses on safety compliance for coronavirus (COVID-19), the Responsible Small Dollar Loans Pilot Program and assessment rates.

The California Department of Business Oversight (DBO) supervises, licenses and regulates a variety of financial institutions, including some real estate mortgage loan originators (MLO’s) holding a Nationwide Multistate (or Mortgage) Licensing System & Registry (NMLS) license. Alongside the California Department of Real Estate (DRE), the DBO shares the responsibility for overseeing MLOs depending on their license use.

Continue reading for a rundown of July’s most important DBO happenings.

Compliance with face covering guidance

The DBO is reminding licensees to make sure all employees and customers are complying with the latest guidance on face masks from Governor Newsom and the California Department of Public Health (CDPH) in regards to COVID-19.

Anyone who refuses to wear masks and those who do not adhere to the exemptions outlined by the CDPH will not be allowed to enter any places of business, including real estate offices, banks credit unions. If you have any questions about face-mask guidance and enforcement, email Ask.DBO@dba.ca.gov.

New report on Pilot Program for Responsible Small Dollar Loans

The DBO recently published the 2019 Annual Report on the Responsible Small Dollar Loans (RSDL) Pilot Program. It contains detailed information from the RSDL Pilot Program, including data on loan size, annual percentage rates, delinquencies, loan terms and borrower income.

The DBO states lenders approved more than 320,000 loans last year, which represents a 40% increase since 2017 and 8% increase since 2018. The total principal amount of loans created last year was more than $428 million, representing a 30% increase since 2018.

The Pilot Program was created to increase accessibility of responsibility small dollar installment loans ranging from $300 to $7,500. The program provides an alternative to payday loans and other forms of consumer credit.

No assessment rate increases planned

In annual assessment invoices mailed to financial institutions, the DBO approved no assessment rate increases for fiscal year 2020-21. Assessments are due July 30 and payments made via electronic funds transfer (EFT) by August 6.

The DBO also released assessment rates for different financial institutions, including trust companies and money transmitters. The base rate is set at:

- $1.39 per $1,000 of assets for trust companies;

- $0.02 per $1,000 received for money transmissions by a licensee; and

- $0.63 per $1,000 of total payment instruments and stored value sold by a licensed money transmitter.

Any questions regarding assessment payment processing should be directed to AccountingAR@dbo.ca.gov.

That’s a wrap for the July 2020 DBO Bulletin! Don’t miss next month’s update and make sure to subscribe to the first tuesday Newsletter to get the latest real estate news and education straight to your inbox every week.

As always, you can read the full DBO Bulletin on their website.

Related topics:

covid-19 pandemic, department of business oversight (dbo)

DBO Bulletin Digest March 2020

DBO Bulletin Digest March 2020 somebodyPosted by ft Editorial Staff | Mar 24, 2020 | Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

The March 2020 DBO Bulletin focuses on COVID-19 and proposed regulations.

The California Department of Business Oversight (DBO) supervises, licenses and regulates a variety of financial institutions, including some real estate mortgage loan originators (MLOs) holding a Nationwide Multistate (or Mortgage) Licensing System & Registry (NMLS) license. Alongside the California Department of Real Estate (DRE), the DBO shares the responsibility for overseeing MLOs depending on their license use.

Continue reading for a rundown of March’s most important DBO happenings.

Coronavirus update

In light of the recent coronavirus (COVID-19) outbreak, the DBO reminds readers of the Centers for Disease Control and Prevention (CDC) recommendations for staying healthy and slowing the spread of COVID-19 in their course of business. The CDC recommends:

- washing your hands with soap and water for at least 20 seconds;

- practicing social distancing;

- avoiding touching your eyes, nose and mouth;

- staying home when you are sick;

- disinfecting frequently touched surfaces; and

- using protective facemasks only when showing symptoms of COVID-19.

Be sure to bookmark the first tuesday journal for the latest updates on how COVID-19 is impacting the real estate market and your clients.

Related article:

DBO Commissioner

The California State Senate voted to confirm Manuel P. Alvarez as the DBO Commissioner on February 24, 2020.

Alvarez has served as Commissioner since his appointment by California Governor Gavin Newsom on March 28, 2019. With the Senate’s confirmation, Alvarez’s title and role will be made official.

Before his appointment, Alvarez worked as Chief Compliance Officer for San Francisco tech startup Affirm Inc. since 2014. But Commissioner Alvarez is also a seasoned civil servant; he was an enforcement attorney at the Consumer Financial Protection Bureau (CFPB) from 2011 to 2014.

With his confirmation, Alvarez officially succeeds Commissioner Jan Lynn Owen, who served the DBO since its creation in 2013.

NASAA and COVID-19 scams

The fear and economic instability surrounding the COVID-19 outbreak has prompted the DBO and other securities regulators to issue a warning to readers about con artists running sophisticated coronavirus scams. In turn, the North American Securities Administrators Association (NASAA) has provided three rule-of-thumb questions to consider before making a new investment:

- Is the investment guaranteeing a high return with little or no risk?

- Is there a sense of urgency or scarcity tied to the investment?

- Is the person offering the investment unlicensed and unregistered?

If you answer “yes” to any of these questions, the NASAA reminds investors that all investments carry a risk of loss. It’s wisest to walk away from high-pressure sales tactics and to avoid unregistered investment salespeople.

State Examination System

The Conference of State Bank Supervisors (CSBS) announced the rollout of the new State Examination System (SES), a single nationwide platform meant to connect state regulators and companies in the examination process. The CSBS expects the SES to improve transparency and collaboration, state regulator oversight of nonbanks and the examination process for both regulators and companies alike.

The SES rollout is an important milestone of Vision 2020, a CSBS initiative to modernize state regulation of nonbank financial companies. The tools created under this initiative, including the SES, are designed to protect consumers by facilitating greater understanding between regulators and financial institutions.

Comment period

The DBO is accepting comments on proposed regulations that clarify the agent-of-payee exemption in the Money Transmission Act (MTA). The Act exempts money transmitters from the license requirement for the activity of receiving money from a person for payment to another. The agent-of-payee exemption was added in response to new online payment technologies.

You can review the notice, text and initial statement of reasons for this proposition here. Submit your comment to regulations@dbo.ca.dov by the April 20 deadline.

The DBO also seeks comments on the proposed regulations that implement Assembly Bill 857, which allows California cities and counties to establish public banks through the DBO. Banks organized under AB 857 would be regulated by the DBO and FDIC just as privately owned banks are now. Read the full bill text here.

Access the DBO’s public comment request here, and submit your comment to regulations@dbo.ca.gov by the April 4 deadline.

And we’ve come to the end of another DBO Bulletin Digest! Don’t miss next month’s update; make sure to subscribe to the first tuesday Newsletter to get the latest real estate news and education straight to your inbox every week.

As always, you can read the full DBO bulletin on their website.

Related topics:

covid-19 pandemic, department of business oversight (dbo)

DBO Bulletin Digest September 2020

DBO Bulletin Digest September 2020 somebodyPosted by Emily Kordys | Sep 28, 2020 | Finance, Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

The September 2020 DBO Bulletin focuses on new tenant and landlord protections and regulatory assistance for communities impacted by California wildfires.

The California Department of Business Oversight (DBO) supervises, licenses, and regulates a variety of financial institutions, including some real estate mortgage loan originators (MLOs) holding a Nationwide Multistate (or Mortgage) Licensing System and Registry (NMLS) license. Alongside the California Department of Real Estate (DRE), the DBO shares the responsibility for overseeing MLOs depending on their license use.

Continue reading for a breakdown of September’s DBO happenings.

Landlord and Tenant Protections

In September, Governor Gavin Newsom signed a new state tenant protection measure, known as the Tenant, Homeowner, and Small Landlord Relief and Stabilization Act of 2020.

The new statewide tenant protection measure protects millions of tenants from eviction and property owners from foreclosure due to economic impacts of COVID-19. These protections apply to tenants who declare an inability to pay rent due to COVID-19-related financial distress.

The governor additionally launched the “Housing is Key” campaign to accompany the new Act. The campaign, which is coordinated by the Business Consumer Services and Housing Agency (BCSH), is meant to connect renters and landlords experiencing pandemic-related economic hardships with helpful information and resources related to the temporary moratorium on evictions.

On the Housing is Key website, renters and landlords can also use a new app for information on the moratorium. The California COVID-19 Information App for Tenants and Landlords uses a survey to provide a personalized, downloadable report that explains the user’s specific protections and obligations under the new law.

Related Articles:

AB 3088: New eviction protections to last through January

Regulatory assistance provided for disaster areas

The Office of the Comptroller of the Currency, the Federal Reserve’s Board of Governors, the Federal Deposit Insurance Corporation, the National Credit Union Administration and state regulators issued a statement on California’s devastating wildfire season. The statement covers financial institutions’ customers and operations and providing appropriate regulatory assistance.

Banks and mortgage lenders are encouraged to work with borrowers in communities affected by the wildfires. Efforts to adjust or alter terms of existing loans in affected areas may be more lenient due to the wildfires. Modification of existing loans need to be evaluated individually to determine whether they represent troubled debt restructurings. The evaluation needs to be based on the facts and circumstances of each borrower and loan, which requires judgment, as not all modifications will result in troubled debt restructurings.

The statement also provides guidance on facilities, regulatory compliance and reporting requirements for financial institutions. You can read more here.

DBO suggestion box

Licensees are invited by Commissioner Manuel P. Alvarez to submit creative ideas and suggestions to help make the DBO more efficient.

Commissioner Alvarez says the DBO wants to hear how they can ease some of the burdens through regulatory efficiencies and the use of technology while they conduct business during the COVID-19 pandemic.

You can send any ideas by email to efficiencies@dbo.ca.gov by October 16, 2020.

New Sacramento address for DBO

The DBO office in Sacramento has relocated. To ensure mail is property delivered to the Department, please send all mail to:

2101 Arena Boulevard

Sacramento, CA 95834

If you need to reach the DBO by phone, call (916) 576-4941.

That’s another DBO Bulletin in the can! As always, you can find the complete DBO Bulletin on their website.

Related topics:

department of business oversight (dbo), landlords, tenants

Digital advertising: A compliance hot spot for brokers

Digital advertising: A compliance hot spot for brokers somebodyPosted by Guest Author Summer Goralik | Jun 2, 2020 | Laws and Regulations, Real Estate, Your Practice | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Real Estate Compliance Consultant and former Department of Real Estate (DRE) Investigator, Summer Goralik, shares advice on complying with digital advertising regulations in 2020. Visit the original post on her blog here.

While a real estate broker needs to manage and oversee myriad areas of compliance, there is definitely one “hot spot” lurking among them that will quickly garner the attention of the California Department of Real Estate (DRE). That hot spot is digital advertising. A broker’s digital advertisements are out there, everywhere, and can be quickly viewed and analyzed by the DRE at any time.

Digital marketing refers to advertising materials that rely on the internet and online-based technology to promote real estate services and products. This type of advertising includes, without limitation, websites, social media platforms (e.g., Facebook, Instagram), and electronic solicitations. It is precisely this type of technology-fused marketing which real estate brokerages and agents heavily depend upon in order to build their brand, reach consumers and hopefully expand their business.

Low-hanging fruit for DRE investigators

Although the world of digital media has transformed the real estate space in so many ways, ultimately bringing brokerages and the buying and selling public together in a more expedient and efficient fashion, it has not been without some drawbacks. As a former DRE Investigator, I have seen countless examples of real estate licensees running afoul of the real estate law, ranging from minor non-compliance to major violations. In turn, I can tell you that a broker’s digital advertising is “low-hanging fruit” for DRE and may lead to investigations that could have been avoided.

Within just a few minutes, DRE Investigators can examine and discover a broker’s non-compliance on the world wide web, without ever leaving their desks or calling a witness. A problematic digital footprint, which is not always easy to unwind, is all the DRE needs to open an enforcement case, gather supportive evidence in connection with an existing complaint, or even further a larger investigation against the broker involving more serious violations. And with COVID-19 shutting the government’s doors and some DRE Investigators now stationed at home or no longer in the field, I imagine that desk investigations are the current status quo across the state.

Challenges in the digital realm

While a brokerage can prioritize and control the compliance of their “online” presence, ensuring that all of their advertising is 100% compliant, the real challenge seems to be making sure their entire salesforce is doing the same. For example, a corporate broker’s digital advertising is typically being prepared, reviewed, supervised, and essentially controlled from a central source. But how does the responsible broker of the corporation review, supervise and/or monitor all of their agents’ digital media? I picture agents’ advertising like tentacles sprawled out from the corporate center, each one representing potential liability for the brokerage.

If you have one or two agents, this is likely an easy task to accomplish. And honestly, you have no real excuse but to get it right. But it’s the larger brokerages that find themselves, or rather, their agents, in hot water with DRE due to some bad marketing.