2022

2022 somebody2022’s new California real estate laws

2022’s new California real estate laws somebodyPosted by ft Editorial Staff | Jan 3, 2022 | Feature Articles, Laws and Regulations, New Laws, Real Estate | 2

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

This article offers an overview of the new laws impacting real estate that were passed and signed into law in 2021.

New laws taking effect in 2022

California’s senate and assembly members have a wide range of legislative agendas that impact firsttuesday readers. In 2021, these included the state’s housing shortage, homelessness crisis, the backlog of rental debt accrued during the pandemic and inequality in real estate. Dozens of new laws were passed in response to these issues and the biggest are examined here.

Editor’s note — Are you interested in becoming more involved in the legislative process as it impacts your career in real estate? Follow our Legislative Gossip page throughout the year to stay informed on real estate related bills. Reach out to your local legislators with concerns and attend local city council meetings for the most impact.

New real estate and appraiser education requirements

Senate Bill (SB) 263 requires real estate licensees and license applicants to complete implicit bias training during their licensing courses and 45-hour renewal courses. These new requirements go into effect beginning in January 2023 and will require real estate licensees and licensee applicants to learn:

- the impact of implicit, explicit and systemic biases on consumers;

- the historical and social impacts of those biases; and

- actionable steps licensees can take to recognize and address their own biases.

Editor’s note — firsttuesday will begin offering the required implicit bias training course later in 2022. Want to get a head start on fair housing and implicit bias topics? Download firsttuesday’s Fair Housing continuing education e-book, which covers many of the topics outlined in SB 263.

For real estate appraisers, Assembly Bill (AB) 948 requires cultural competency and anti-bias training. This new law also makes it unlawful for appraisers to discriminate in their appraisals or in making available their services to members of protected groups.

Further, the Bureau of Real Estate Appraisers (BREA) will be required to include a check box within their existing complaint form, asking the complainant whether they believe the appraisal is below market value. Complainants will have the option to include their demographic information on the form. The BREA will need to study this demographic information and provide a report of their findings to the state legislature before July 1, 2024.

Addressing inequalities in housing

Along with the new anti-bias requirements for real estate licensees and appraisers, legislatures are cracking down on inequalities in real estate in other ways.

AB 491 requires a mixed-income residential building constructed beginning January 1, 2022 to maintain common areas and entrances accessible by all types of units, incorporating all units rather than separating or isolating low-income units to a single floor or wing of the building.

Further, AB 1466 requires a title insurance company involved in a transfer of real property to identify whether any of the documents contain unlawfully restrictive covenants beginning July 1, 2022. When unlawful covenants are identified, the title insurance company will need to record a modification document with the county recorder. Before July 1, 2022, only the property owner may record a modification.

Loosened zoning eases the housing shortage

California’s housing shortage is infamous for causing extremely low inventory, escalating bidding wars and pushing home prices and rents beyond the capabilities of most household incomes. As a result, low- and even moderate-income households have been forced to delay homeownership, move in with roommates or lose their housing altogether. This dynamic has made many look to other states for a more reasonable cost of living, helping cause California’s first ever population decline in 2019.

To add to our state’s limited housing inventory, California’s legislature passed several new laws in 2021, to take effect in 2022. These include:

- SB 10, which authorizes local governments to zone any parcel for up to 10 units of residential density when the parcel is located in a transit-rich area, a jobs-rich area or an urban infill site;

- AB 345, which requires each local agency to allow an accessory dwelling unit (ADU)to be sold or conveyed separately from the primary residence to a qualified buyer;

- AB 571, which prohibits a local government from imposing affordable housing impact fees from being imposed on a housing development’s affordable units;

- SB 591, which permits the covenants, conditions and restrictions (CC&Rs) of a senior citizen housing development to establish intergenerational housing that includes seniors aged 55+ along with caregivers who do not meet the age minimum and transitional age youths, as long as at least 80% of the occupied dwelling units in the development are occupied by seniors;

- AB 1584, which makes any CC&R that affects the transfer or sale of an interest in real estate that effectively prohibits or unreasonably restricts the construction or use of an ADU on a lot zoned for SFR use void and unenforceable. It also requires a common interest development (CID) to amend any governing document that includes a covenant restricting ADUs in this manner by July 1, 2022;

- SB 9, which sets forth what a local agency can and cannot require in approving the construction of two residential units on a single lot, or a single family residence and an ADU. This new law also requires a proposed housing development containing two residential units within a single-family residential zone to be considered without discretionary review or hearing when the proposed housing development meets certain requirements, including that the proposed housing development does not require demolition or alteration of low- or moderate-income housing; and

- SB 60, which raises the maximum fines for violating an ordinance relating to a residential short-term rental which poses a threat to health or safety from $100 to $1,500 for a first violation, from $200 to $3,000 for a second violation of the same ordinance within one year, and from $500 to $5,000 for each additional violation of the same ordinance within one year of the first violation.

Still, loosening zoning restrictions and allowing greater housing density remains contentious. According to a recent firsttuesday poll, 51% of readers believe there ought to be more permissive zoning which allows for higher density construction. However, the remaining 49% advocated for more restrictive zoning which limits the number of units and height allowed for new residential construction.

This razor thin outcome in the polling results parallels the highly contentious nature of zoning more broadly. Yet, without shifting how local governments approve new housing, California’s housing crisis will only worsen.

Addressing COVID-19 rental debt

SB 91 used federal funds to cover 80% of the back-rent accumulated by low-income tenants from April 1, 2020 through March 31, 2021. In return, the landlord is required to forgive the remaining 20% of rent owed.

AB 832 enacted the Rental Housing Recovery Act, which built on previous legislation to keep tenants housed during the recovery from the 2020 recession and COVID-19 pandemic. This Act extended a temporary moratorium on the eviction of residential tenants for the nonpayment of rent that became delinquent between March 2020 and September 30, 2021 due to the tenant’s COVID-19 related financial distress.

Further, landlords may sue their tenants for unpaid rent which became due between March 1, 2020, and September 30, 2021 in small claims court starting March 1, 2022.

Prior to March 1, 2022, courts will only hear an eviction case due to nonpayment of rent when the landlord has attempted to obtain rental assistance, and:

- the application is denied; or

- after 20 days have passed, there is no sign the tenant will cooperate. [Calif. Code of Civil Procedure §1179.11(a)]

Read more about how to access rent relief and what eviction forms to use here: How and when residential evictions will resume in California.

Related page:

Plans to fight the homelessness crisis

California’s homelessness crisis continued to reach new levels in 2021. However, the California Comeback Plan was launched in May 2021 to provide:

- immediate housing to 65,000 people;

- long-term housing stability to 300,000 people;

- 46,000 new housing units; and

- money to clean up public spaces that typically serve as homeless encampments.

While these plans are crucial to address the immediate homelessness crisis, a longer-term fix will be found in providing enough housing to accommodate low- and moderate-income renters and homebuyers. Recently, some of these new laws have included AB 978 and AB 1482, which:

- cap annual rent increases at 5% plus the rate of inflation for much of California multi-unit residential properties and mobilehomes; and

- require “just cause” to evict tenants in place for 12 months or more.

Related article:

Related topics:

california legislation, california zoning, housing shortage

A Dear John to homebuyer love letters

A Dear John to homebuyer love letters somebodyPosted by Kinnedy Kriso | Jun 27, 2022 | Fair Housing, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

In California’s competitive markets, real estate agents depend on an arsenal of creative weapons to secure home sales transactions. But one of those weapons — the buyer love letter — is now coming under fire.

Homebuyer love letters are personal notes sometimes included in an offer, written to appeal to the seller on an emotional level. They often gush about the property (“I love your additions to the living room”), reveal some personal detail in the hopes of making a connection (“I noticed your garden, I have a green thumb too!”) and might even include a picture-perfect family portrait.

A good love letter plucks the seller’s heartstrings in a way that all-cash offers cannot. But even heartstrings wear down and being inundated with love letters in a hot market can cause sellers to tune out. More importantly, the letter might reveal a personal detail about the buyer against which the seller may harbor implicit bias.

The seller loves me, loves me not

Though agents are split on their effectiveness in swaying sellers, love letters come roaring back during competitive markets. In California, home prices rose sharply in response to the pandemic; closing transactions became an industry meme. Up against all-cash offers, California’s real estate professionals pulled out all the stops — including love letters.

In less competitive markets, these letters fall on deaf ears. And such a market is looming; the second half of the double-dip recession is expected to arrive heading into 2023.

California’s housing market stands at the precipice of a downturn, with prices expected to bottom in 2025. In fact, real estate licensees in the state are already seeing steep price cuts at every tier. Shortly, today’s hand wringing over the appropriateness of love letters will become moot. They may not return again until 2026 or 2027, when firsttuesday expects a sustainable recovery.

Editor’s note — Prepare for the upcoming recession by expanding your real estate skills and credentials with firsttuesday’s California Notary Education course.

But there’s a chance love letters may not even return for the next boom cycle. Thanks to increasing scrutiny on discrimination in real estate, some professionals are writing them off altogether. The concern is that sellers will base their decision on a personal detail, possibly discriminating against a stronger offer from a protected group.

The Federal Fair Housing Act (FFHA) prohibits discrimination in the sale, rental, and financing of housing based on:

- race or color;

- national origin;

- religion;

- sex;

- familial status; or

- disability.

California’s list of protected classes is more extensive than federal protections, with discriminatory practices prohibited based on an individual’s:

- race or color;

- religion;

- sex;

- sexual orientation;

- gender identity;

- genetic information;

- marital status;

- national origin;

- ancestry;

- familial status;

- source of income; or

- disability.

Related article:

Some states have gone as far as banning love letters entirely. Oregon House Bill 2550 prevents a seller from accepting love letters (including photographs) from buyers entirely. The bill became effective in 2022 but was recently blocked by a judge, establishing a preliminary injunction that prohibits enforcement of the law until a final decision is reached.

But here in California, love letters are still free to pluck heartstrings. A lawsuit has yet to challenge a seller or a real estate professional on discrimination based on a love letter. Experts rate the likelihood of successful legal prosecution in a love letter case as difficult to impossible. This is because a prosecutor would have to prove beyond doubt that the seller discriminated against a buyer based on their protected group status, and not the myriad other variables in the offer.

Implicit Bias training

For seasoned agents and brokers, the quiet discussion of managing clients’ personal biases is nothing new. But with the passage of California Senate Bill (SB) 263, that discussion has been codified in real estate licensing and education law.

SB 263 requires California licensees to undergo 2-hour course in implicit bias training; and 3-hour course on fair housing. This includes a critical interactive component in which the licensee roleplays as both consumer and real estate professional to explore implicit and explicit biases in the industry. These tools aim to create a better understanding of discrimination’s many facets, including those potentially communicated through love letters.

Editor’s note — firsttuesday is one of the first California real estate schools to develop and submit its own training and to the California Department of Real Estate (DRE) for approval. Sign up for the firsttuesday Newsletter to be notified when the course is available for your license.

Identifying personal biases in the real estate industry is only one step toward creating a fairer and more equitable California. Visit the firsttuesday resource page Legislative steps toward more affordable housing to stay ahead of California real estate’s changing legal landscape.

And let us know in the comments: will you continue to use buyer love letters in California despite their potential liability?

Related Reading:

Real Estate Principles

Chapter 8: California Fair Employment and Housing Act

Related topics:

california home prices, federal fair housing act, implicit bias

Access to Homeownership and the Wealth Gap

Access to Homeownership and the Wealth Gap somebodyPosted by ft Editorial Staff | Oct 3, 2022 | Fair Housing, Feature Articles, Real Estate, Video | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

This is the fourth episode in our new video series covering Implicit Bias principles, and provides a sneak peek into the new continuing education (CE) requirements that apply to real estate agents and brokers with licenses expiring on or after January 1, 2023.

This episode deconstructs the source of the homeownership gap and the corresponding wealth gap. Click for the prior episode in series.

A source of wealth

Homeownership is the main source of wealth for American families. To increase household wealth, the U.S. government subsidizes and encourages homeownership through various tax incentives and mortgage programs, like:

- the mortgage interest deduction (MID);

- Federal Housing Administration (FHA)-insured, low down payment mortgages;

- low ceilings on capital gainstax; and

- Proposition 13 (Prop 13) in California.

Yet despite these incentives, some groups have greater difficulty becoming homeowners than others, which leads to an enormous wealth disparity between racial and ethnic groups.

The median household wealth as of 2019 is:

- $184,000 for white households;

- $38,000 for Latinx/Hispanic households; and

- $23,000 for Black households. [Kent, Ana Hernández & Ricketts, Lowell. (2021) Wealth Gaps between White, Black and Hispanic Families in 2019]

Put another way, for every dollar held by white households, Black households hold only 12 cents, and Latinx households hold only 21 cents.

While all types of asset ownership are greater for white households, the majority of this racial wealth gap can be explained by lower homeownership rates among Black and other minority households.

Why minority households steer clear of homeownership

If homeownership is the key to wealth, why don’t more minority households buy homes?

If past experience has taught minority communities anything, it’s that for Black and Latinx households, homeownership is not the “safe investment” many vociferously proclaim it to be.

The National Bureau of Economic Research (NBER) published a study on the impact of the 2008 Millennium Boom and subsequent Great Recession on the homeownership rates of Black and Latinx households compared to white households (Asian households were excluded from the study). [Bayer, Patrick; Ferreira, Fernando & Ross, Stephen L. (2013) The Vulnerability of Minority Homeowners in the Housing Boom and Bust]

It found the 2009 foreclosure crisis had a greater effect on Black and Latinx homebuyer communities compared to white communities. The share of homeowners who lost their homes to foreclosure during this time was:

- over 1-in-10 Black and Latinx households; and

- just 1-in-25 white households.

Why were Black and Latinx homeowners more than twice as likely than White homeowners to lose their homes? Three factors converged to increase the likelihood of foreclosure:

- aggressive subprime or predatory lending;

- high debt-to-income ratios (DTIs) allowed by lenders; and

- high cases of employment instability.

Millennium Boom: the perfect storm for minority homebuyers

The most dangerous factor that increases the likelihood of foreclosure for Black and Latinx homebuyers is predatory lending.

The largest recognized case of predatory lending was settled by Bank of America (BofA) in 2012 for their subsidiary company, Countrywide’s, discriminatory lending practices. BofA paid $335 million to roughly 200,000 victims of Countrywide’s actions.

Countrywide discriminated against minority homebuyers in two ways, by:

- charging higher fees to minorities than white homebuyers with equivalent qualifications; and

- steering minority homebuyers into subprime mortgage products, even though the targeted homebuyers had equal or better credit histories than other white homebuyers who were not shown bad mortgages.

Higher upfront fees and subprime mortgages induced the minorities targeted by Countrywide to ultimately pay much more than similarly qualified white homebuyers. Therefore, when the housing market and the economy went bust following the Millennium Boom, it was more difficult for minority homebuyers to make mortgage payments than the white homeowners who took our mortgages with Countrywide — the mortgages themselves were already less favorable and posed more risk.

Lenders also deliberately encouraged minority homebuyers to take on more debt than they would reasonably be able to carry — in effect, steering them to a mortgage product with a higher DTI that would provide the greatest benefit to the lender. The higher a homebuyer’s DTI, the greater the risk and the less likely the buyer will be able to make future mortgage payments.

Lenders of the Millennium Boom era did not seem to care about this axiom, and knowingly pushed minority homebuyers into mortgages they were unable to pay. This resulted in higher immediate fees for lenders, who jettisoned the risk to other investors by selling the bad mortgages on the secondary mortgage market — out of sight, out of mind.

Lastly, homeowners were more likely to lose their home following the Great Recession due to the statistical fact that the heads of Black and Latinx households are more likely to be employed in professions more susceptible to economic downturns, like manufacturing and other hourly jobs. In other words, the heads of these households are more likely to lose their jobs than their white counterparts.

Job loss and the inability to pay are the biggest reasons homeowners default on their mortgages. Other financial shocks also contribute to the decision to strategically default, which is typically a struggling household’s last resort. [Gerardi, Kristopher; Herkenhoff, Kyle F.; Ohanian, Lee E. & Willen, Paul. (2015) Can’t Pay or Won’t Pay? Unemployment, Negative Equity, and Strategic Default]

The problem for California real estate

California is a large, diverse state. Nearly 40% of the population identifies as Latinx (Hispanic or Latino/Latina), according to the U.S. Census. Roughly 16% identify as Asian and 7% identify as Black or African American. Therefore, discrimination in the mortgage and housing markets has a far-reaching influence on our state.

Another issue for minority homebuyers, not mentioned in the NBER report, is the discriminatory behavior practiced by some real estate agents.

Compared to similarly qualified white clients, the U.S. Department of Housing and Urban Development (HUD) finds real estate agents show fewer rental and for-sale listings to Black, Asian and Latinx clients. [Aranda, Claudia L.; Levy, Diane K; Pitingolo, Rob; Santos, Rob; Turner, Margery Austin; Wissoker, Doug; The Urban Institute. (2013) Housing Discrimination Against Racial and Ethnic Minorities 2012]

Why do some real estate agents tend to show minority homebuyers fewer listings than their white counterparts?

It’s usually implicit bias on behalf of the real estate agent. For instance, some real estate agents may think they’re doing their Black clients a favor by only showing them homes in neighborhoods predominately full of other Black residents (an unlawful practice). Or agents may not realize they’re slower to respond to requests by minority homebuyers, exercising a lesser degree of urgency than they would normally provide.

This perpetuates neighborhood segregation, which limits minority household access to higher quality jobs, better schools and other resources that disproportionately benefit white households.

The only way to stop a California real estate agent from discriminating against minority clients? The California Department of Real Estate (DRE) may enforce anti-discrimination laws. However, the DRE will only pursue an agent for ethics violations after first receiving a formal complaint.

In cases of discrimination, most homebuyers, sellers and renters do not know how to take appropriate action by contacting the DRE. Therefore, it is up to fellow agents and brokers to report discriminatory practices to the DRE. Aggrieved individuals may report complaints on the DRE’s website using their online complaint form.

Editor’s note – firsttuesday was one of the first schools in California to obtain DRE-approval for the new implicit bias training and expanded Fair Housing course.

To enroll, visit the order page.

Related topics:

implicit bias

As California’s rent relief funds run low, fraudsters rush to pilfer cash

As California’s rent relief funds run low, fraudsters rush to pilfer cash somebodyPosted by Amy Platero | Apr 4, 2022 | Laws and Regulations, Property Management, Real Estate, Recessions | 3

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Keeping rental assistance programs churning amid the recession hangover requires California to fuel up on federal funding.

But now, the state is running empty.

For the past 12 months, California’s rent relief program — Housing Is Key — has accepted applications from tenants unable to make rent payments and from landlords submitting applications on their behalf. As of March 31, 2022, the window to apply for rental assistance in California has closed, though many applications are still in the pipeline, awaiting a decision on rent relief.

Related article:

On June 28, 2021, the state passed Assembly Bill (AB) 832, which saw:

- $5.2 billion in federal funds allocated for the state’s rent relief program; and

- tenants and landlords able to receive 100% of the back rent due to them.

However, the reality has fallen far short of the goal. As of March 2022, the statewide rent relief program has:

- received $7.1 billion in requests for funds; and

- allocated $2.5 billion in rent relief, paying on average $11,443 per household, according to Housing Is Key’s interactive dashboard.

To bridge the deficit between amounts received from the federal government and amounts requested from California tenants and landlords, the California Department of Housing and Community Development (HCD) formally requested an additional $1.9 billion from the U.S. Treasury.

The Treasury responded by granting the state just $62 million — far below what is needed, according to the HCD. The U.S. Treasury also released $136 million in its second round of emergency rental assistance (ERA), according to the U.S. Treasury.

These additional funds are a drop in the bucket compared to what the state’s tenants need to remain in their homes. Worse, what little funds are left may be at the mercy of fraudsters attempting to access what they view as a free lunch.

Related article:

Fraudulent claims for emergency rental assistance

Although the funds have fallen short, of the tenants who have been successful at receiving ERA, more than 84% are very low- or extremely low-income households, earning less than 50% of their area’s median income, according to the HCD.

While the state is working to distribute ERA funds to these tenants at greatest risk of eviction, tenants who have applied for ERA on or before the March 31, 2022 deadline may stave off eviction while their ERA decision is pending.

Related article:

In contrast, there’s the risk that some of the relief money will go towards paying out fraudulent claims.

The CEO of a risk solutions firm estimates 25% to 30% of claims for rent relief are filed fraudulently by individuals using personal identifiable information to pretend they are a tenant, according to ABC News.

In one case, a homeowner in Alameda County received a letter from the state addressed to someone who claimed to be renting his home, despite not being a landlord or owning any rental properties.

Officially, the state reports a much more conservative estimate of ERA fraud cases in California: 1,800 fraudulent rental assistance applications identified out of 500,000 statewide, or less than 1%, according to the HCD, as reported by ABC News.

Of course, there’s no way to know whether those identified cases represent the whole or if more are slipping through the cracks in the state’s investigations.

For example, in 2021, two California residents from Tulare County were arrested for attempting to defraud the rent relief program. The couple was charged with forgery and fraudulent personation, according to NBC news.

The HCD is confident fraud claims are under control, unlike at the beginning of the pandemic when unemployment fraud claims made up nearly 10% of all unemployment claims, according to the California Employment Development Department.

But the underpinnings of these two programs were much different, as states scrambled to distribute unemployment benefits during the 2020 recession. With so little time to prepare, fraud screening measures were not fully implemented.

That scramble was not so prevalent with the state rental relief program, which had months to prepare and continues to act slowly in approving applicants and distributing its funds, while also using greater security measures the state learned to be vital through its handling of unemployment benefits.

The pandemic and 2020 recession have been tough teaches, but it appears, at least from the state’s perspective, that it’s gotten ahold of fraud claims surrounding its rent relief program.

Now, it’s just a matter of getting ahold of funds.

Related article:

Related topics:

2020 recession, california landlords, emergency rental assistance (era), fraud, unemployment

As mortgage interest rates rise, concessions return

As mortgage interest rates rise, concessions return somebodyPosted by Amy Platero | Dec 12, 2022 | Buyers and Sellers, Finance, Interest Rates, Loan Products, Mortgages, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Mortgage rates in 2022

Mortgage interest rates have earned their spot as 2022’s news story of the year. In fact, 71% of respondents in a recent firsttuesday poll singled out interest rates as the biggest challenge in today’s housing market — and many are turning to old transaction tricks to salvage their sales volume.

In response to 40-year high consumer price inflation, mortgage interest rates swung upwards in 2022. In turn, buyer purchasing power has plummeted for California homebuyers. As of the third quarter (Q3) of 2022, homebuyers with the same income are able to borrow 31% less purchase-assist money than a year prior when interest rates were distorted at near-historic lows during the Pandemic Economy.

In step with purchasing power, one-to-four unit single family residential (SFR) mortgage origination volume has also fallen back significantly from 2021 levels, when they totaled $4.44 trillion, according to the Mortgage Bankers Association (MBA). This is a far cry from the MBA’s forecast of $2.26 trillion in SFR originations for 2022, and $2.05 trillion in 2023.

This slowdown in mortgage origination is forcing layoffs in the mortgage industry, with more to come over the next two years. Savvy mortgage loan originators (MLOs) have already begun to prepare for the downturn in origination fees with MLO side hustles.

In the meantime, buyers looking to recoup lost purchasing power are dusting off old strategies to secure a more comfortable monthly mortgage payment. The most popular strategies include builder concessions in the form of points or buydowns, adjustable rate mortgages (ARMs), interest-only mortgages and, of course, shopping with multiple lenders for the most competitive offer.

Mortgage points

Mortgage points draw in buyers by offering a lower interest rate over the life of the mortgage. With points, the buyer (or seller, when offered as a concession) pays an upfront fee to the lender in exchange for a lower rate.

Typically, each mortgage point is equal to 1% of the total mortgaged amount. For example, on a $100,000 mortgage, one points equals $1,000. Two points are 2% of the mortgage amount, or $2,000. On a $300,000 mortgage, one point is equal to $3,000.

Paying mortgage points is essentially prepaying mortgage interest upfront. For points to be a sound investment, buyers need to plan to stay in the home for several years.

Related article:

Buydowns

Seasoned agents and brokers might recognize temporary buydowns, a mortgage product widely used through the 1970s and 80s when mortgage interest rates also zoomed upward. Now, it’s experiencing a revival.

A temporary buydown reduces the homebuyer’s monthly payments in the first year (sometimes in the first two or three years) before resetting to the higher market rate. Instead of making the mortgage’s full monthly payments right away, the homebuyer makes discounted payments for the first year or more, depending upon which type of buydown the buyer secured.

The 3-2-1 and 2-1 temporary buydowns are among the most common. In the 3-2-1 buydown, a seller or builder pays an amount of money upfront to buy the rate down. For instance, the rate would go from about 6% — the current average 30-year fixed rate mortgage (FRM) rate — to 3% at the start of the payment period. The next year, the rate would go up to 4%; the following year 5%; and then finally 6% for the remaining years left on the mortgage.

The 2-1 temporary buydown works similarly, except it has two periods of adjustment instead of three — for example, it will begin at 4%, then reset to 5% after a year, then back to 6%.

Related article:

ARMs

ARMs provide lenders with periodic increases in their yield on the principal balance during periods of rising and high short-term interest rates. They enjoy greater demand when interest rates or home prices rise quickly, leaving fewer buyers able to qualify for FRM financing. A graduated payment schedule allows buyers time to adjust their income and expenses in the future to begin the eventual amortization of the loan.

ARMs averaged a rate of 5.70% as of November 2022, compared to 6.49% for the average 30-year FRM rate as of December 2, 2022.

The low teaser rate on ARMs makes the risk more appealing to homebuyers set on taking back the purchasing power they lost to rate hikes. It also helps break down resistance to home price reductions — dissolving the sticky pricing phenomenon among your seller clients.

As the undeclared recession intensifies going into 2023, expect the ARM rate to rise and exceed FRM rates, likely in the first half of 2023. This inversion will slash homebuyer appeal of ARMs instantly.

Related article:

Interest-only mortgages

With an interest-only ARM, the buyer’s monthly payments are applied only to the interest due on the loan, not to the loan principal. This interest-only payment schedule is typically for three to 10 years.

After the interest-only period expires, the buyer’s monthly payments are adjusted to include both interest and principal. However, because the buyer did not make any principal payments during the first few years of the mortgage term, the principal payments are amortized over a shorter period of time.

For example, a buyer enters into a mortgage agreement with a lender for an ARM which amortizes over 30 years. The terms of the mortgage provide for the buyer to make interest-only payments for the first three years of the mortgage. After the three-year period expires, the lender will adjust the interest rate according to the terms of the mortgage and recast the mortgage to amortize the buyer’s payments over the remaining 27-year period.

Some interest-only mortgages also have periodic adjustments to the interest rate during the interest-only period.

Buyer beware: the longer the interest-only period, the greater the payments will be when the loan recasts.

Consider a buyer taking out a 30-year ARM with a five-year interest-only feature. The buyer’s monthly payment during the first five years of the mortgage is $625. However, after the initial teaser period, the lender recasts the mortgage, raises the interest rate to 5% and amortizes the mortgage balance over the remaining 25 years of the mortgage. The buyer’s monthly mortgage payment jumps to $1,461 in the sixth year of the mortgage, more than double the amount of the buyer’s early payments.

Related Video: Types of ARMs

Click here for more information on ARM variations.

Shopping around

No matter the interest rate environment, the best way a buyer may secure the most competitive interest rate is to mortgage shop between lenders.

When choosing a lender, buyers need to cast a wide net and consider different types of institutions — such as an online lender, a bank and a credit union.

Different lenders offer different closing costs and interest rates, which may save (or cost) a homebuyer thousands over the life of the mortgage.

Real estate professionals: your buyers need to apply with at least three lenders to find the lowest rate, lowest fees and most favorable terms. Homebuyers are largely unaware interest rate quotes vary significantly between lenders.

Once your client has applied to multiple lenders, take advantage of our Mortgage Shopping Worksheet to quickly compare the rates, costs and terms of each lender. [See RPI Form 312]

Although mortgage interest rates are in the midst of a long-term rising cycle, real estate professionals can still count on these strategies to squeeze more transactions out of a slowing housing market.

Subscribe to Quilix, the firsttuesday newsletter, for more weekly news and updates on tailoring transactions to a recessionary market.

Related topics:

adjustable rate mortgage, mortgage, mortgage interest rates

Avoid Discrimination Risks When Advertising

Avoid Discrimination Risks When Advertising somebodyPosted by ft Editorial Staff | Oct 17, 2022 | Fair Housing, Feature Articles, Real Estate, Video | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

This is the sixth episode in our new video series covering Implicit Bias principles, and provides a sneak peek into our new DRE-approved continuing education (CE) requirements that apply to real estate agents and brokers with licenses expiring on or after January 1, 2023.

This episode provides actionable guidance for advertising to a wide, diverse audience. The prior episode covers the economic drawbacks of implicit bias.

Implicit signaling

In advertising, a company needs to target audiences effectively and directly. For example, goods marketed toward women are stereotypically packaged in pastels, identifying them as engineered for a feminine audience before you can even say “For Her.”

While that might pass muster in retail, applying such a strategy in real estate may amount to implicit discrimination or worse – explicit discrimination.

For an example of implicit discrimination in advertising, consider an agent who directs Black homebuyers only to neighborhoods with a large Black population. While they may believe they are acting in their client’s best interest by guiding them to a community with a similar population, the impact is discriminatory and this activity is unlawful.

Of course, some neighborhoods are not a good fit for every homebuyer. But when selling and renting properties, it is risky to limit your marketing blitz to a single group — even when that group is protected under fair housing laws.

Relatedly, when you are going to use models or stock photography in any of your marketing materials, be mindful to use images of all types of people. Do not single out one group in particular, even when the group you choose to single out is a protected group. By relying on just one type of person in your marketing, whether premised on race, gender or other protected class, you are implicitly signaling the property is not a good fit for others who are not in this group.

Federal protections under the Federal Fair Housing Act (FFHA)

The printing or publishing of an advertisement for the sale or rental of residential property that indicates a wrongful discriminatory preference is a violation of the Federal Fair Housing Act (FFHA). [42 United States Code §3604(c)]

A property sold or leased for residential occupancy is referred to as a dwelling. The discriminatory preference rule applies to all brokers, developers and landlords in the business of selling or renting a dwelling. [42 USC §3603, 3604]

Real estate advertising guidelines are issued by the Department of Housing and Urban Development (HUD). The guidelines are the criteria by which HUD determines whether a broker has practiced or will practice wrongful discriminatory preferences in their advertising and availability of real estate services.

HUD guidelines also help the broker, developer, and landlord avoid signaling preferences or limitations for any group of persons when marketing real estate for sale or rent.

Wrongful discriminatory preferences in advertising

The selective use of words, phrases, symbols, visual aids and media in the advertising of real estate may indicate a wrongful discriminatory preference held by the advertiser. When published, the preference can lead to a claim of discriminatory housing practices by a member of the protected class.

Words in a broker’s real estate advertisement that indicate a particular race, color, sex, sexual orientation, handicap, familial status or national origin are considered violations of the FFHA.

To best protect themselves, a broker – as gatekeeper to real estate – refuses to use phrases indicating a wrongful preference, even when requested by a seller or landlord.

Preferences are often voiced in prejudicial colloquialisms and words such as restricted, exclusive, private, integrated or membership approval. Words or phrases indicating a preference in violation of the rights of persons from protected classes include:

- white private home;

- perfect for newlyweds;

- Jewish (or Christian) home;

- country club nearby;

- Black home;

- walking distance from the synagogue;

- ideal bachelor pad;

- spacious master bedroom;

- Hispanic neighborhood; or

- adult building.

Beyond just words

Words are not the only way to discriminate. Selectively using symbols, images, human models, visuals and other forms of media indicate preference too. Examples of symbols and other visual aids used in advertising include:

- sexuality pride flags;

- religious images such as a cross or Star of David;

- gender symbols;

- handicapped signs; and

- flags representing nationalities.

As previously discussed, aiming an advertisement at a particular class may lead people outside the group to believe they are not welcome in the area. Also, it may make the seller and their agent look like they only want to do business with a few select groups, which is never the desired intent in good brokerage practice.

The phrases above directly target protected classes, so it is best to leave them out of your practice – period. This includes listings and marketing materials, as well as applications and deeds. While some may not sound aggressively prejudiced, even the seemingly harmless phrase “spacious master bedroom” is to be avoided due to the historical underpinning of the expression.

Regardless of what the advertiser meant, these problematic phrases can alienate clients and welcome a discrimination lawsuit.

Further, these phrases may not directly reference protected classes. Words like “exclusive,” “private” and “restricted” indicates the neighborhood has a barrier to entry, such as income, religion or ethnicity. Phrases like “membership approval” raise all sorts of loaded questions, like what makes someone qualified for a membership and how members are approved. It’s best to avoid these red herring words and focus on the property facts, of which there are many.

Protect against discrimination lawsuits

As a matter of best practices, real estate professionals – gatekeepers – need to avoid using discriminatory language or images in their practice, keeping in mind the ostensibly welcoming advertisement examples discussed here. Further, to create a favorable impression which induces the most people to contract for real estate services with the brokerage, real estate professionals need to avoid all language that is politically charged or can be construed of carrying an unintended loaded meaning.

No matter how well-intentioned the specifications may be, good intentions will not protect brokers and agents against fines and potential litigation.

Brokers may not direct potential buyers or renters to areas the broker thinks are suitable for them based on their protected status.

Prior to 2022, a loophole in the Real Estate Regulations allowed agents to decide which properties to show clients with disabilities, based on what the agent believed to be suitable or unsuitable properties due to the client’s disability. For example, a broker representing a client in a wheelchair may have skipped showing their client any properties with stairs, believing they were doing their client a favor.

However, agents cannot fully understand their clients’ needs or abilities, even despite their best intentions. Therefore, a 2022 update requires real estate professionals to provide all clients an opportunity to view, rent, sell or finance any property the client believes will suit their needs, closing the disability loophole. [DRE Reg. §2780(b)]

It is best to cast a wide net in real estate when advertising homes as using discriminatory ads may lower turnover rates – and in turn, reduce fees. Brokers are better off making listings sound inclusive, not like they’re trying to appeal to a niche.

Fair housing is not a niche, and neither is getting paid.

Editor’s note – firsttuesday was one of the first schools in California to obtain DRE-approval for the new implicit bias training and expanded Fair Housing course.

To enroll, visit the order page.

Related topics:

advertising, implicit bias, marketing

Avoid Discrimination Risks in Rental Practices

Avoid Discrimination Risks in Rental Practices somebodyPosted by ft Editorial Staff | Nov 7, 2022 | Fair Housing, Feature Articles, Real Estate, Video | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

This is the seventh episode in our new video series covering Implicit Bias principles, and provides a sneak peek into our new DRE-approved continuing education (CE) requirements that apply to real estate agents and brokers with licenses expiring on or after January 1, 2023.

This episode covers fighting implicit bias in the screening of tenant applicants. The prior episode covers avoiding discrimination risks in advertising.

Ask the same standard questions of all tenants

A good rule of thumb is to simply not ask a potential or current tenant questions regarding their protected status.

For example, since landlords may not discriminate based on a tenant’s national origin, landlords may not ask prospective tenants what country they were born in as this can never be a factor in deciding the terms, conditions or privileges for their rental of a dwelling.

To avoid discrimination, landlords need to ask all potential tenants the same standard questions to ensure equal treatment. Landlords also ought to limit inquiries to matters that are directly applicable to the potential renters’ tenancy or the maintenance of the rental property.

For example, landlords may ask:

- about the presence of pets;

- how many tenants will occupy the property;

- how many parking spaces will be required;

- whether their present landlord will provide a favorable reference;

- whether any of the tenants smoke; and

- whether any of the tenants intend to use a waterbed in the premises.

This allows landlords to screen tenants effectively and limits vulnerability to a lawsuit from a potential tenant who believes they were treated unfairly. For example, a landlord may not ask questions about the tenant’s:

- marital status;

- religious practices;

- intention to have children;

- national origin;

- disability status; or

- any other protected status.

Some common fair housing violations more broadly include:

- refusing to rent, lease or sell housing due to illegal discrimination;

- sexual harassment, particularly demanding sexual favors in return for housing;

- creating documents, such as covenants, conditions and restrictions (CC&Rs) that discriminate against a protected group;

- denying a home loan or insurance for discriminatory reasons; and

- failing to reasonably accommodate a disability.

When a landlord is on shaky ground with fair housing laws, it is best to err on the side of caution. The penalties for violating these laws are serious and can include loss of their license, and awarding money to the aggrieved individuals involved and paying attorney fees.

Removing discriminatory language from CC&Rs

A common interest development (CID) or homeowners’ association (HOA) may not be governed by covenants, conditions and restrictions (CC&Rs) which discriminate against any person due to an individual’s actual or perceived:

- race;

- color;

- religion;

- sex;

- gender;

- gender identity;

- gender expression;

- sexual orientation;

- marital status;

- national origin;

- ancestry;

- familial status;

- source of income;

- disability;

- veteran or military status; or

- genetic information. [Calif. Civil Code §4225(a); Calif. Government Code §12955(a); (m)]

When a discriminatory declaration is included, the board will amend and record the CC&Rs to remove the prohibited declaration regardless of membership approval. [CC §4225(b); (c)]

When a person provides the CID with written notice regarding the discriminatory language included in the CC&Rs, the board has 30 days to remove the prohibited language. When the language is not removed within 30 days, the Department of Fair Employment and Housing (DFEH), the local government in which the CID is located or any person may pursue legal action against the CID. [CC §4225(d)]

Editor’s note – firsttuesday was one of the first schools in California to obtain DRE-approval for the new implicit bias training and expanded Fair Housing course.

To enroll, visit the order page.

Related topics:

implicit bias

Black mortgage applicants denied almost twice as often as white applicants

Black mortgage applicants denied almost twice as often as white applicants somebodyPosted by Carrie B. Reyes | Feb 14, 2022 | Fair Housing, Mortgages, Real Estate | 4

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Bias in mortgage lending is well-documented historically, and it continues today. The result has been lower homeownership rates and less wealth for Black and Latinx households.

Nationwide, Black mortgage applicants are denied nearly twice as often as white applicants. Here in California, mortgage denial by race is not as starkly unequal as on the national scale, but the difference in denial rates is still apparent. The share of mortgage applications denied by race is:

- 16% for American Indian mortgage applicants;

- 15% for Black applicants;

- 13% for Latinx applicants;

- 13% for Pacific Islander applicants;

- 10% for white applicants; and

- 10% for Asian applicants, according to a Zillow analysis of the 2020 Home Mortgage Disclosure Act (HMDA).

While the share of households unable to qualify for a mortgage is clearly skewed across race and ethnicity, it is not necessarily due to explicit discrimination. The high mortgage denial rates for non-white and non-Asian households can be traced to many observable factors, including:

- down payment size;

- credit history;

- debt-to-income (DTI) ratios; and

- job security.

For example, just over one-third of Black mortgage applicants who didn’t qualify were denied due to credit history. Further, the average Black mortgage applicant listed a 3.5% down payment, well below the 8.9% down payment from applicants averaged across all races.

In these cases, it’s not so much direct discrimination by the lender, but the residual effects of systemic racism on Black and Latinx communities.

For example, redlining and its ongoing impacts have reduced wealth in Black and Latinx communities, limiting generational wealth and reducing access to benefits like down payment gifts and inheritance. Redlining is the practice of denying mortgages and under-appraising properties in minority communities.

While redlining was outlawed in 1977, its impacts continue all these years later. Redlining led to a decline in both the quality and quantity of housing in communities lenders considered to be “risky” investments. Today, these neighborhoods that were subject to redlining have lower homeownership rates, home values and rents — and thus, less wealth.

In fact, parental transfers of wealth like down payment gifts account for 30% of the Black-white homeownership gap, as found in a study by the Consumer Financial Protection Bureau (CFPB). In the U.S., young white households are twice as likely to be homeowners as are young Black households.

The result: the homeownership rate for Black households in the U.S. is just 44% and 48% among Latinx households. By the same measure, the homeownership rate for white households is a whopping 73%.

Related article:

Proactive agents step in

Real estate brokers and agents are well positioned to open the doors of homeownership for all groups of people, including those who have historically been left out of homeownership. Often, a proactive approach is needed.

When a potential homebuyer wants to buy but is unable qualify due to common reasons like a lack of credit history, low down payment or high DTI ratio, their agent encourages them to keep trying.

It’s important for brokers and agents to take the extra step to help these potential homebuyers qualify when they are in a better financial situation, maybe a few months in the future. For example, brokers can inform unsuccessful mortgage applicants about special mortgage programs designed for first-time homebuyers. Some of these programs allow more leeway in qualifying or provide down payment assistance.

In other cases, the client will be able to gain mortgage approval after taking a few steps to pare down debt or build their credit history. Without being pushy, brokers may continue to check in every month or so to see where they are in the process. Clients may be discouraged or embarrassed about being denied a mortgage, but it’s the broker’s job to keep them motivated and on the path to homeownership.

Agents who want to break down the homeownership barrier will take positive steps to ensure they are reaching the broadest range of potential clients, removing obstacles and not leaving any group out of the potential for homeownership.

Editor’s note — firsttuesday’s editorial staff is hard at work preparing content for California’s new implicit bias course requirements. Want to get a head start on fair housing and implicit bias topics? Download firsttuesday’s Fair Housing continuing education e-book.

Related topics:

black homeownership, implicit bias

Buyer breach of contract in a decreasing price environment: Seller remedies

Buyer breach of contract in a decreasing price environment: Seller remedies somebodyPosted by Madison Hart | Jul 15, 2022 | Buyers and Sellers, Home Sales, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

This article helps homebuyers and sellers understand the legal ramifications of a breach of contract.

Market conditions prevent buyers from completing purchases

Since mid-2020, home sellers — and their agents — have had the luxury of their home sales being a sure thing.

Here in California, the housing market continues to experience high competition for a limited inventory of homes for sale, resulting in rising home prices. However, in 2022, home sales volume has begun to slow and price cuts are on the rise.

The historically low interest rates which occurred throughout the pandemic played a big part in allowing buyers to snatch up homes. But interest rates are on the rise now, and a sea change for sellers has already begun.

In other words, what was previously a sure thing — a quick and easy home sale — is now on shaky ground.

With the jump in interest rates and downward sloping home sales volume, home prices are expected to decrease heading into 2023. As prices slide, buyers under contract will spot equivalent homes listed for less and realize they have overpaid. Their reaction will be to pull out and buy the less expensive house — or simply wait for the market to bottom.

Other situations may cause buyers to simply lose their qualifications to buy in today’s slippery housing market, including:

- unexpected job loss; and

- higher interest rates pushing their debt-to-income (DTI) ratio beyond the maximum threshold.

As the above scenarios play out in the next few months, we will see more buyers breaching purchase agreements.

Of course, buyers ought to be mindful of ensuring they do their due diligence before entering into a purchase agreement. This includes allowing a buffer for interest rate increases and being sure of their job security.

But, more importantly, sellers and their agents need to be prepared for when the inevitable happens.

Related poll:

Liabilities and monetary losses for purchase agreement breach

When a purchase agreement is breached, the implications can range from a mild hiccup to a huge loss. Either way, it will be the buyer’s and seller’s agents running into the battlefield to assist their clients.

During an upward price environment, a breached contract is usually no more than a minor headache for the seller, as it delays the eventual sale of the property. It might actually result in a higher sales price, as they can now relist the property at a higher price.

However, the opposite is true in a falling price environment, when a breached purchase agreement often translates to monetary losses for sellers.

That’s because in the intervening weeks or months from when a purchase agreement is agreed to and breached, property prices will have declined. It may also mean lost money due to longer carrying or operating costs.

What are a seller’s options when they experience monetary losses due to a buyer’s breach of contract?

Related article:

Once more unto the breach for liability

Upon a buyer breach of contract, sellers then need to decide their next step. This may include:

- enforcing the purchase agreement;

- remarketing the property for sale; or

- retaining the property.

The seller is generally responsible for value jumping around after the buyer breaches. Thus, for fund recovery, a money loss needs to be accounted for.

There are liability limitations in a purchase agreement, which include a:

- liquidated damages provision; and

- contract limitation on recovery.

The liquidated damages provision sets the cash deposit as the ceiling amount for recoverable money losses. The latter sets the limit for recovery and creates an agreed limit for this amount in the purchase agreement. [See RPI Form 150 §10.7]

The loss is recoverable by the seller, unless the property does end up being sold for the same price — or more.

The buyer’s deposit

A seller is entitled to recover their losses when the net proceeds for the resale transaction equals less than the gain from the original purchase agreement.

However, the seller needs to account for the loss.

Consider a buyer and seller who entered into a purchase agreement during a time when interest rates were lower. As they hike, the buyer is no longer able qualify at the new, higher mortgage payments. The buyer is forced to back out of their agreement. In the meantime, the property’s valued has diminished, impacting the seller’s bottom line.

This is where the collection of the buyer’s deposit comes in.

The buyer’s deposit — also called the good-faith deposit or earnest money — will be offset by the amount of the seller’s losses. Essentially, the seller may have the right to retain the buyer’s earnest money deposit on cancellation of the purchase agreement.

When a breached purchase agreement contains a provision limiting the dollar amount of losses the seller can collect, the losses recoverable are controlled by the agreed-to limit, and the accrual of interest is added on top.

Any interest due accrues at the legal rate of 10%. When the seller agreed to an installment sale, the note rate for the carryback paper is the controlling rate. [See RPI Form 150 ]

Forecast for future purchase endeavors

As we head into the next downturn for home prices, real estate professionals need to focus on the potential liabilities for their clients entering into purchase agreements.

Breaches in purchase agreements will increase as we head into the recession, expected to officially arrive heading into 2023. Expect to see declining sales volumes from 2022-2024, with prices bottoming in 2025.

Real estate professionals: have you seen more buyers breaching contracts? Share your experiences with other readers in the comments below!

Related article:

Related topics:

breach of contract, liability, purchase agreement

California real estate: 2022 in review and a forecast for 2023

California real estate: 2022 in review and a forecast for 2023 somebodyPosted by Carrie B. Reyes | Dec 27, 2022 | Economics, Feature Articles, Home Sales, Interest Rates, Laws and Regulations, Real Estate, Recessions, Your Practice | 4

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

This article provides a bird’s eye view of the legislative changes and economic shifts which impacted real estate professionals during 2022. We then look ahead to the property market in 2023, and beyond.

What do you see as the trend in SFR construction starts in 2023?

- SFR starts will decrease (69%, 63 Votes)

- SFR starts will remain the same (20%, 18 Votes)

- SFR starts will increase (11%, 10 Votes)

Total Voters: 91

The aftermath of Pandemic Economics

After two years of volatile economic waves, California’s pandemic response officially ended in 2022. As the year closes, real estate professionals preparing for 2023’s housing market can start by retracing the Pandemic Economy’s path.

At the state level, the pandemic pushed legislators to enact eviction and foreclosure moratoriums and distribute individual stimulus checks in 2020-2021. Along with the pandemic-induced supply chain disruption, these actions resulted in rapidly escalating inflation — both consumer price inflation and asset price inflation.

Extra money in their wallets emboldened consumers to over-spend (and under-save) during 2021-2022, which also helped prop up the jobs market. Employers continue to hire going into 2023, with jobs surpassing the 2019 peak in October 2022.

For the housing market, perhaps the most influential impact of pandemic era policy was on mortgage interest rates.

Following the Federal Reserve’s (the Fed’s) actions to drop interest rates to historic lows in 2020-2021, the Fed ended its pandemic period monetary policy of funding and setting interest rates on home mortgages by exiting the mortgage-backed bond (MBB) market at the end of 2021.

On exiting, the funding and setting of fixed rate mortgage (FRM) rates returned to the bond market. This resulted in a jump in mortgage rates to match bond market MBB yields which, unlike Fed funding, are based on the 10-year Treasury Note rate plus a risk premium rate presently set at double historic norms in anticipation of a recessionary rise in defaults.

The result of all the pandemic-related fiscal and monetary stimulus caused consumer inflation to exceed the Fed’s target of 2%. To rein in and tamp down excess consumer inflation, the Fed bumped up their benchmark rate several times in 2022. This directly increased interest rates on adjustable rate mortgages (ARMs).

Further, interest rates on long-term debt obligations, such as the 30-year FRM, reflect bond market investor perceptions about the level of success the Fed will achieve in their current fight to lower consumer inflation. When the Fed is succeeding in its fight — as is beginning to appear heading into 2023 — bond market investors accept lower yields, and FRM rates follow.

While mortgage rates skyrocketed in the first three quarters of 2022, they were slashing mortgage borrowing and thus buyer purchasing power. This brought on a cascade of altered behaviors in the marketing of real estate services, to stretch on for the next two-to-three years as buyers now take the reins.

The casualty of rising mortgage rates on sellers of real estate

These toppled dominoes lead us to the year’s leading market fundamental: As buyer purchasing power declines, so goes support for home sales.

Homebuyers qualify for a maximum mortgage amount based on their incomes and shifting interest rates. Thus, any rise in mortgage rates instantly cuts the amount they can borrow, and the price they pay for a home is reduced. The only factor able to move in the triangle consisting of the homebuyer, lender and seller is the seller’s list price.

Following a pandemic-distorted year of high home sales volume in 2021, sales volume peaked early in 2022. While year-end reports are not yet in, sales volume is likely to dip below 2019 levels — the last “normal” year for sales volume — in 2022.

Thus, home prices have fully reversed course from their May 2022 peak, ranging from 6% below the peak in the low tier to a staggering loss of 9% in the mid and high tiers.

Still, average home prices remain a tenuous 5% higher than a year earlier for low-tier prices, 6% higher for mid-tier prices and 8% higher for high-tier prices as of September 2022. This year-over-year spread is narrowing rapidly, with reports expected to show the annual price change turning negative near the start of 2023.

As home values plunge, recent mortgaged homebuyers are falling underwater.

Related article:

Negative equity homeowners are unable to sell their home when unexpected circumstances require them to rid themselves of their asset. These include a job loss — as is common during a recession — a required relocation or household change. Their only solution is to:

- negotiate a short sale with the lender; or

- exercise their put option, forcing the lender to foreclose.

Savvy real estate agents and MLOs will be prepared to handle the coming wave of distressed sales and work with an evolving base of homebuyers and sellers to earn fees, even as the volume of traditional sales slows to a trickle.

Related article:

Pandemic Economics are also removing support in the commercial property market.

Industrial space vacancy rates increased during 2022, on their way to a return to pre-pandemic rates in 2023 — an occupancy level evincing a “fair deal” environment for both landlord and tenant.

This rise in the vacancy rate is a prelude to the elimination of the excessive demand on space brought on by the pandemic period which needs to take place before the industrial market can begin to stabilize.

However, there is some movement for unused commercial space. An increase in commercial-to-residential conversions is both helping to alleviate the housing shortage and giving a second life to unprofitable retail and office space.

Related article:

New laws to encourage construction

California continues to experience a statewide housing shortage, which has led to an ongoing population decline as former residents head for states with more reasonable housing costs.

To address the housing shortage, state lawmakers continue to pass new legislation to add to the housing inventory.

Commercial-to-residential conversions are becoming more common with the passage of Senate Bill (SB) 6 and Assembly Bill (AB) 2011, which permit:

- multi-family developers to submit projects for a streamlined ministerial review process, which are exempt from conditional use permits and environmental impact reports; and

- residential development within areas zoned for office, retail or parking uses when specific conditions are met, including requirements for:

- density;

- public notice;

- comment;

- hearing;

- site location and size;

- consistency with sustainable community strategy or alternative plans;

- prevailing wages for builders; and

- a skilled and trained workforce.

Both bills encourage builders to transform office and retail commercial spaces into housing units for low- and middle-income Californians. These housing bills require general plans for land development and the compliance to local zoning laws.

Accessory dwelling units (ADUs) are also having a moment, with the passage of SB 897 and SB 2221, which prohibit:

- owner-occupant requirements for ADUs; and

- a local government from establishing front setback limits for ADUs, specifies detached ADUs may include an attached garage, and decreases ADU permitting times.

California’s infamously restrictive zoning regulations and high building costs mean new housing for low- and moderate-income households remains scarce. But recent pro-ADU legislation has more homeowners cashing in on the shortage and becoming landlords.

Related article:

Property management updates

For landlords, the expiration of pandemic-era eviction moratoriums means a full return to the Tenant Protection Act (TPA) of 2019, which:

- caps annual rent increases at 5% plus the rate of inflation for much of California multi-unit residential properties;

- requires “just cause” to evict tenants in place for 12 months or more.

The applicability of the TPA is comprehensive, covering most multi-unit residential real estate housing in California and those single family residential (SFR) units owned by a real estate investment trust (REIT), a corporation or a limited liability company (LLC) with a corporate member.

However, there are numerous, sizable exemptions for multi-family units and conditions for SFRs to be excluded, including:

- residential units which have been issued a certificate of occupancy within the previous 15 years;

- a duplex of which the owner occupied one of the units as their principal residence at the beginning of the tenancy and remains in occupancy;

- units restricted as affordable housing for households of very low, low, or moderate income, or subject to an agreement that provides subsidies for affordable housing for households of very low, low, or moderate income;

- dormitories constructed and maintained in connection with any higher education institution in California;

- units subject to rent or price control that restricts annual increases in the rental rate to an amount less than that set by the TPA;

- multi-unit transient occupancy housing like hotels and motels;

- accommodations in which the tenant shares kitchen or bathroom facilities with an SFR owner-occupant;

- SFR real estate that can be sold and conveyed separate from the title to any other dwelling unit, like in an SFR subdivision or condominium project, provided:

- the owner is not one of the following:

- a real estate investment trust (REIT);

- a corporation; or

- a limited liability company (LLC) in which at least one member is a corporation; and

- the tenant has been given written notice stating the rental property is exempt from the rent increase caps under the TPA. [Calif. Civil Code §1947.12(d); CC §1946.2(e); See RPI Form 550, 551 and 550-3]

- the owner is not one of the following:

Even though the TPA took effect in 2020, the pandemic interruption has meant many landlords have yet to enact the TPA in practice. The California Office of the Attorney General (OAG) has begun cracking down on landlords committing unjust evictions.

Read more about the rules for just cause eviction under the TPA.

Other new laws for landlords enacted in 2022 include:

- AB 2559, which encourages and clarifies rules regarding reusable tenant screening reports; and

- SB 971, which requires landlords receiving low-income tax credits to allow pets.

Related video:

Shifting requirements for real estate professionals

California requires Department of Real Estate (DRE) licensees to render their services to the public with consistency and competence. This means staying on top of the constantly shifting landscape of laws which affect licensees’ practice and treatment of the public.

Passed in 2022, SB 1495 delays the implementation of the implicit bias and fair housing law components in the Real Estate Practice course required for licensing education until January 1, 2024. Meanwhile, two hours of implicit bias training is already required for renewing DRE licensees, implemented by a 2021 law.

SB 869 requires the Department of Housing and Community Development (HCD) to regulate individuals acting as managers or assistant managers of mobilehome parks and requires the completion of at least 18 hours of training on the rules and regulations for operating a mobilehome park.

For prospective brokers, AB 2745 requires non-licensees applying to the DRE for a broker’s license to show the required two years of general real estate experience accumulated within the five-year period prior to the exam application date.

Forecast for 2023 and beyond

The biggest development of 2022 has been the abrupt about-face in real estate dynamics. What was a seller’s market for the past decade has quickly become a buyer’s market.

The reason? California’s housing market is being dragged down by the economic encore to the short-lived 2020 recession. This time, offsetting government stimulus will be limited while the Fed’s rate increases eliminate excess consumer price inflation and Wall Street resumes the setting of FRM rates.

Real estate sales volume and prices will continue to fall in 2023-2024 as dictated by rising mortgage rates and capitalization (cap) rates.

Watch for a return of real estate speculators in 2024 to provide a “dead cat” bounce in real estate sales volume and pricing, falling back and bottoming in 2025. A sustainable recovery will take off in property sales with the return of end user property buyers — more reliable buyer occupants and long-term buy-to-let investors — around 2026-2027. Then, prices will gradually rise during the recovery from the 2023 recession.

How agents can survive and thrive during the 2023 recession

What can agents do to adjust to the downturn in 2023-2025?

Agents need to pivot from focusing on providing seller services to finding and working with buyer clients. This means refocusing expertise on the needs of buyers (and tenants), and advertising yourself as a buyer’s agent.

Become an expert in assisting clients with the types of sales common during a recession, including purchasing:

- homes at trustee’s sale — foreclosures;

- short sales; and

- real estate owned (REO) properties.

For agents with seller clients during a downturn, they can help along the sale by encouraging the seller to offer seller financing, also known as carryback financing.

For seller’s agents, carryback financing can make their property more marketable, enabling a higher sales price, while also allowing the seller to defer the tax bite on their profits.

Carryback financing generally offers the buyer:

- a moderate down payment;

- a competitive interest rate;

- less stringent terms for qualification and documentation than imposed by traditional lenders; and

- no origination costs or lender processing hassle. [See RPI ebook Creating Carryback Financing]

Finally, agents can take on side gigs available in a multitude of fee-based real estate services, including:

- obtaining a higher fee split by upgrading to a broker’s license;

- gaining new marketable skills like becoming a notary public;

- earning a mortgage loan originator (MLO) endorsement to assist homeowner clients obtaining a mortgage;

- rounding out your skillset by becoming a property manager— one of the few recession-proof real estate jobs;

- becoming a foreclosure and short sale specialist, as distressed sales inevitably rise when home values drop;

- assisting with the management and sale of real estate owned (REO) properties; and

- using the recession as a launchpad for investment by becoming an expert in forming real estate syndicates and 1031 exchanges.

Poised to profit off existing contacts in real estate-adjacent careers, these agents and brokers will survive and succeed even as the housing market continues to slip deeper into the recession.

Track California’s housing market in 2023 with firsttuesday — subscribe to Quilix for your Monthly Statistical Update and more real estate market analysis in your inbox every week.

Related article:

Related topics:

california legislation, foreclosure, mortgage interest rates, recession

California’s home remodeling boom set to peak in 2022

California’s home remodeling boom set to peak in 2022 somebodyPosted by Amy Platero | Apr 25, 2022 | Buyers and Sellers, Economics, Real Estate, Recessions | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

With interest rates on the rise, homeowners who sat out of the pandemic market might feel they missed their chance to trade up. But there’s another solution that feels just as new: home renovations.

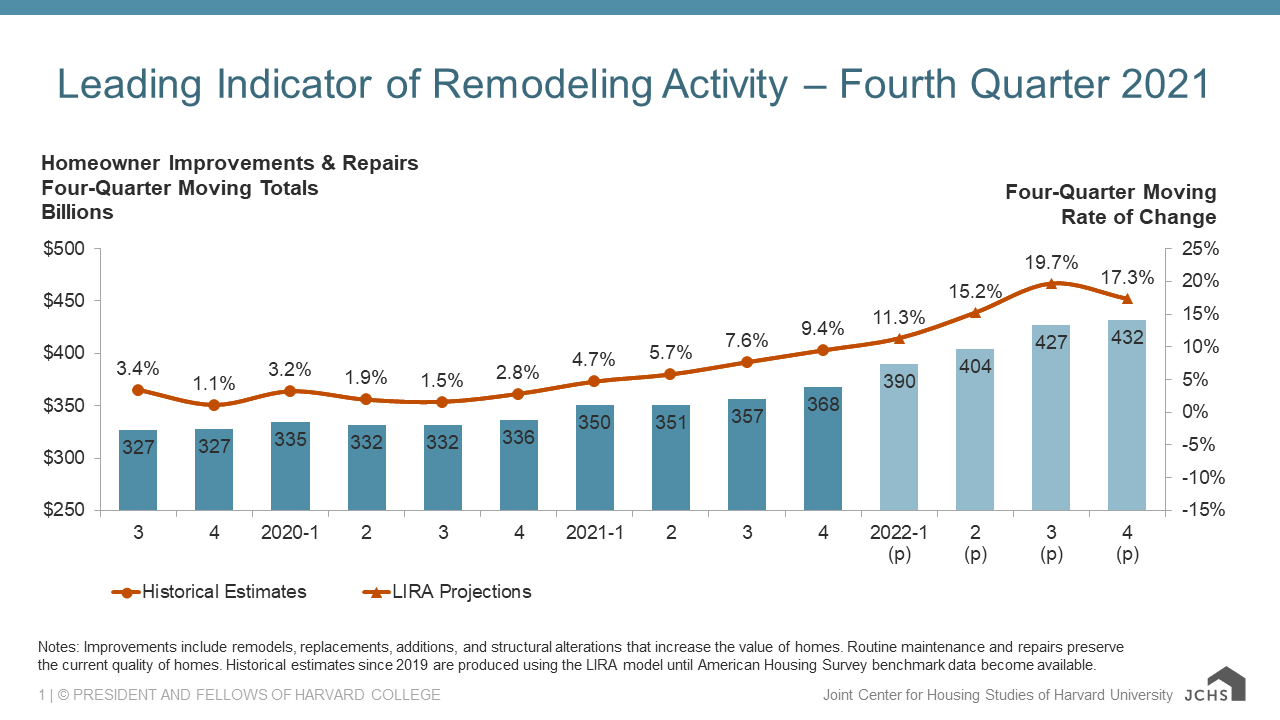

For owners of residential real estate, renovations have become increasingly enticing — and expensive. The home remodeling market may peak to a new height of $430 billion by the end of 2022, according to projections from Harvard University’s Joint Center for Housing Studies (JCHS).

Year-over-year, the home remodeling market increased a robust:

- 4.7% in Q1 2021;

- 5.7% in Q2 2021;

- 7.6% in Q3 2021; and

- 9.4% in Q4 2021.

2021’s nearly double-digit gains in expenses for home repairs and remodels came as a surprise even to the Joint Center for Housing Studies. Early on in the year, they projected the home remodeling market to have a much more moderate annual increase of 3.8% for 2021.

In Q2 2022, total homeowner expenditures for home renovations are projected to ramp up into double-digit territory, increasing 15.2% year-over-year and surpassing $400 billion for the quarter, according to JCHS.

{kind=link}