2023

2023 somebodyA home inspection report: the liability shield for a seller’s broker

A home inspection report: the liability shield for a seller’s broker somebodyPosted by Carrie B. Reyes | Feb 16, 2023 | Buyers and Sellers, Feature Articles, Laws and Regulations, Real Estate, Your Practice | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

This article explains how a home inspection report (HIR) is used by a seller’s broker to shift the risks of non-disclosure liability in their mandatory use of a seller’s Transfer Disclosure Statement (TDS).

Transparency by design — don’t wait for the buyer to inquire

California’s recessionary housing market, which began in mid-2022, brings brokers and their agents face to face with a dramatic reversal away from the crass seller attitudes about dealing with buyers which developed in recent years of recovery and boom times.

Sellers prefer asymmetric property disclosures, which for agents as licensees is a deleterious path taken at their peril.

Consider that the position of an agent in any transaction — be it a sale, lease or a mortgage — is that of a facilitator. Agents have a duty to deliver discoverable information adversely affecting the value and use of a property to all participants, to document the negotiations, and to ultimately close the transaction as intended.

Today, a seller’s agent needs to inform their seller about the challenges of selling property in a recessionary housing market. A marketing plan of full disclosure — transparency by design — is needed to maintain the seller’s competitiveness in a market thin on prospective buyers and long on inventory.

Transactions in a recession differ from the boom phase of the market when prospective buyers prepare offers and willingly enter into purchase agreements without receiving sufficient (if any) information about material facts mandated for disclosure by a seller and their agent. Thus, sellers and their agents had a wholesale tendency to delay disclosing adverse property information — the Transfer Disclosure Statement (TDS) — until after entering into a purchase agreement. [See RPI Form 150]

Today’s recessionary housing market is demonstrably different. Sellers and their agents need to gather and package critical property information and deliver it as soon as practicable (ASAP) at the time a prospective buyer or their agent first asks for more property information.

A seller during a recession needs to listen and correct any preconceived boom-time notions they espouse about pricing and buyer behavior based on their real estate agent’s listing presentation.

Related article:

Transfer disclosure statement (TDS)

Before a sales agent agrees to take a seller’s listing, the agent first needs the seller to agree to prepare the mandated TDS. The agent provides the seller with a blank TDS form which the seller fills out based on their prior knowledge or suspicions of property defects. Disclosures are not limited to property conditions preprinted for comment on the statutory form mandated for use by the seller. [Calif. Civil Code §1102.8; see RPI Form 304]

The seller notes in the TDS any physical, environmental or neighborhood features which:

- adversely affect the property’s value; or

- interfere with a prospective buyer’s anticipated use of the property.

After the seller has prepared the TDS, the agent and seller meet to review its contents. Meanwhile, the agent schedules their mandatory visual inspection —and home inspection report (HIR) discussed below — of the seller’s property, noting on the TDS any defects observed by the agent which the seller did not note. [CC §2079]

Any seller objections to the mandatory inspection or defects the agent observes — or noted in the HIR — do not control the agent’s conduct regarding property disclosures. The seller’s agent owes a general duty to prospective buyers to conduct the inspection, observe defects affecting the property’s value and marketability and report them on the TDS prospective buyers are to receive.

However, while the agent owes a general duty to disclose adverse property conditions to buyers, they have no duty to further investigate property conditions or make comment on the consequences of the information disclosed.

TDS: Mandated on one-to-four unit residential units

Once the agent lists their findings in the TDS, both the seller and their agent sign the TDS. Thus, they both take responsibility for its content and delivery to prospective buyers as soon as practicable when a prospective buyer asks for additional information concerning the property. Without the TDS, prospective buyers are unable to determine the property’s condition, value, and the price they are willing to pay for it. [Jue v. Smiser (1994) 23 CA4th 312]

First the disclosures, then the agreement to sell

Consider a purchase agreement entered into by a seller prior to the buyer receiving property disclosures. Before closing, the buyer becomes aware of property defects and demands corrections before funding for the reason they were unaware of the defects when they set the price they agreed to pay.

Here, the seller’s broker and their agent expose themselves to liability for non-delivery of the TDS prior to the time the buyer and seller entered into a purchase agreement. Presenting the TDS to buyers before contracting to buy is the first step the seller’s agent and their broker take to shield themselves from liability for non-disclosure of defects.

For a seller’s broker and their agent to best market a property to mitigate risks concerning non-disclosure of material facts to a buyer, a full disclosure package is prepared and presented to prospective buyers ASAP which contains these items:

- TDS or Condition of Property Disclosure Statement; [See RPI Form 304]

- home inspection report (HIR) attached to the TDS;

- Natural Hazards Disclosure (NHD) Statement; [See RPI Form 314]

- an occupancy certificate, when required by local ordinance;

- Home Energy Rating System (HERs) report on energy efficiency;

- Property Operating Expense Profile; [See RPI Form 306

- Residential Earthquake Hazards Report; [See RPI Form 315]

- structural pest control report (SPC);

- Seller’s Neighborhood Security Disclosure; [See RPI Form 321]

- Homeowners’ Association (HOA) addendum;

- Lead-Based Paint Disclosure; [See RPI Form 313]

- Disclosure of Sexual Predator Database; [See RPI Form 319]

- Local Ordinance Report; [See RPI Form 307]

- well water report, when applicable;

- septic tank report, when applicable; and

- Comparative Market Analysis (CMA) for setting values. [See RPI Form 200-1]

The exacting Home Inspection Report

During the initial counseling session with the seller before accepting their listing of the property for sale, the agent needs to ask the seller to provide written authority to order a Home Inspection Report (HIR).

The agent explains the HIR is a written report prepared by a home inspector after their inspection of a property. The HIR will be used to prepare the TDS and is attached to it as an addendum. [See RPI ebook: Real Estate Principles: Chapter 21: The home inspection report]

The HIR, together with the TDS, informs prospective buyers about the precise physical condition of the property so decisions can be made to prepare and submit an offer. An HIR notes any defects adversely affecting the:

- property’s desirability;

- property’s value; and

- buyer’s intended use.

A home inspector is a professional employed by a home inspection company to inspect and advise on the physical condition of property improvements in a home inspection report they prepare. The seller, the seller’s agent and the buyer may rely on an HIR as a warranty of the condition of improvements, except for defects known to the seller or their agents and not included in the HIR or TDS.

The home inspector who holds a professional license with the state as a general contractor, architect, pest control operator or engineer is deemed to be qualified, unless the agent knows of information to the contrary.

When hiring a home inspector, agents can look for qualifications such as the inspector’s:

- educational training in home inspection courses;

- length of time in the home inspection business or related property or building inspection employment;

- errors and omissions (E&O) insurance covering professional liability;

- professional and client references; and

- membership in the California Real Estate Inspection Association, the American Society of Home Inspectors or other nationally recognized professional home inspector associations with standards of practice and codes of ethics.

A qualified home inspector performs a non-invasive physical examination to identify material defects within mechanical, electrical, and plumbing components not observed or observable to the seller’s agent. [Calif. Business and Professions Code §7195]

These material defects affect the property’s:

- market value;

- desirability as a dwelling;

- habitability from the elements; and

- safe usage as a dwelling.

Based on their observations, the home inspector may also recommend the need for further evaluations by other experts regarding defects they discover or perceive to exist.

To cure or not to cure defects

On receipt of the HIR, the seller needs to decide whether they will cure some — or all — of the listed defects. The seller is not obligated to cure any of them unless they agree to make repairs. However, they are obligated to disclose the presence of known defects within the property to prospective buyers.

When the seller cures any of the defects noted in an HIR, an updated HIR is ordered. Either way, the seller signs the HIR and returns it to the agent. [See RPI Form 130]

During a recessionary market, buyers are more likely to demand the seller cures defects or accept a price reduction to cover the costs and efforts of the buyer to cure them after closing.

A TDS prepared to include defects noted in the HIR is the ultimate liability shield for agents and their brokers. An HIR used by the seller’s agent to prepare a TDS acts to mitigate their risk of liability for buyer claims in a transaction should the buyer discover defects not listed in the HIR or the TDS — before or after closing.

To be effective as a shield, the TDS and HIR disclosures need to have been handed to the buyer before the seller entered into a purchase agreement with the buyer.

However, the preparation and use of the HIR does not relieve the sales agent from conducting their mandatory visual inspection of the property. [CC §1102.4(a)]

Delivered to buyers, not to lookie loos

Once all third-party investigative reports for a property have been received, reviewed, and included within the marketing package, the seller’s agent is then prepared to locate prospective buyers and manage property disclosures the agent has a duty to deliver.

The seller’s agent need not provide the marketing package to every prospective buyer viewing the property. However, the seller’s agent does provide copies of the TDS and attached HIR to buyers and buyer’s agents when they request additional information on the property — but not to lookie loos who casually view the property with no indication they might submit an offer.

These inquiries for more information from the buyer or the buyer’s agent are evidence negotiations have started. It is negotiations which trigger the agent’s delivery of the TDS and HIR as part of the marketing package.

After receiving the TDS and HIR, the buyer’s agent reviews their contents. Unlike the seller’s agent, the buyer’s agent has no duty to inspect or confirm whether the contents of the TDS or HIR are complete.

On the outside chance the buyer’s agent observes an unlisted defect relating to the property’s components or the buyer’s intended use, they are to disclose this information to all participants.

An HIR as a relied-upon warranty

The HIR is not a confidential document, no matter who orders the report or pays for it. The HIR contains facts about a property’s conditions, and the preparer cannot limit who may rely on its contents. All buyers are entitled to information in an HIR and may rely on it to further their understanding of the property’s value and determine the price they might be willing to pay for it. [Leko v. Cornerstone Building Inspection Service (2001) 86 CA4th 1109]

Further, any provision in the home inspection contract attempting to waive or limit the inspector’s liability for a negligent investigation or preparation of the HIR is unenforceable. [Bus & Prof C §7198]

When the buyer discovers an error in the HIR after acquiring the property, they have four years from the date of the inspection to pursue any money losses they incur due to the undisclosed defects affecting the property’s value or desirability. [Bus & Prof C §7199]

Any defenses the home inspector asserts to limit the time period to less than four years for the buyer to make a claim are unenforceable. The four-year period is necessary to give buyers enough time to realize the home inspector produced a faulty HIR. [Moreno v. Sanchez (2003) 106 CA4th 1415]

By delivering the TDS and HIR to the buyer or the buyer’s agent upfront — before an offer or counter offer is accepted — the seller and their agent ensure the buyer has all the information needed on the property’s condition to set a price in their offer for their purchase of the property.

Related topics:

home inspection report (hir), material fact, recession, transfer disclosure statement (tds)

An evaluation of streamlined housing production under SB 35 after five years

An evaluation of streamlined housing production under SB 35 after five years somebodyPosted by Amy Platero | Aug 18, 2023 | Economics, Laws and Regulations, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

The California legislature introduced Senate Bill (SB) 35 in 2017 as part of a wave of housing bills meant to address the state’s low- and moderate-income housing shortage.

SB 35 allows eligible housing developments to go through a streamlined approval process — including bypassing a review under the California Environmental Quality Act (CEQA) — so long as projects meet local objective zoning and design standards, provide a minimum percentage of low-income units, and follow labor and wage requirements.

Since its implementation in 2018, SB 35 has:

- streamlined 18,000 new housing units across the state;

- made the approval process for new multifamily infill development faster and more certain;

- become a default approach for many low-income housing developers;

- mostly been used for 100% low-income housing developments; and

- been used to overcome local resistance to new housing, according to The Terner Center.

The number of completed SB 35 housing projects according to the California Department of Housing and Community Development (HCD) has been:

- 375 in 2018;

- 419 in 2019;

- 108 in 2020;

- 21 in 2021; and

- 39 in 2022.

Most SB 35 projects were built in the Bay Area and Los Angeles County, according to The Terner Center. However, use of SB 35 increased in other parts of the state after the first couple years of its implementation.

In 2022, the share of SB 35 projects completed by income level in California include:

- 33% that were very low income;

- 48% that were low income;

- 7% that were moderate income; and

- 12% that were above moderate income, according to the HCD.

Related article:

Build up, not out

Suburban sprawl has proven to be a poor long-term housing and retail strategy, despite the appeal of a mythic stand-alone home on the prairie.

The suburban sprawl trend leads to higher construction costs and less desirable outcomes for homeowners, as they are forced into neighborhoods with fewer amenities and longer commutes.

Prompt action on the re-zoning of city center parcels will take advantage of vertical environment — build up, not out — to level out the next home price boom, expected around 2026, from turning into another market-killing pricing bubble.

Rising prices of existing single family residence (SFR) housing will be subdued when new units can be built at prices comparable to home resale prices. Critically, zoning is the pricing key to builder access and market stability.

Successful zoning laws keep demand for government services at a consistent level when builders are allowed to demolish obsolete and insufficient structures and construct high-density housing on existing blocks and parcels within city centers. Thus, the need to extend roads and utilities (which the cities will then be required to maintain) is avoided.

Encouraging builders to build in urban centers makes cities more favorably centralized. At the same time, center city improvements deliver the convenient apartments and condos the growing cultural flow of urban dwellers most desire. Given the choice, most prefer to live near to where they work.

Legislation like SB 35 makes the permitting and building process for low-income housing options and infill development within urban areas more accessible. It sidesteps the vocal not in my backyard (NIMBY) supporters of restrictive zoning who champion suburban sprawl and place pressure on local city councils to deliver more of the same.

Still, more needs to be done to reduce the costs and time required to develop new housing in California, which will allow housing to reflect the population and its needs.

SB 35 is scheduled to sunset in 2026 unless SB 423, which was introduced in early 2023, is passed. SB 423 seeks to extend and modify the streamlined approval process created under SB 35.

Stay updated on the latest California legislation affecting housing at our Legislative Gossip page and subscribe to the Quilix newsletter for the latest real estate news and market trends.

Related article:

Related topics:

california legislation, construction, housing shortage, low-income housing, zoning

Attorney General files lawsuit against Elk Grove for violating state housing laws

Attorney General files lawsuit against Elk Grove for violating state housing laws somebodyPosted by Amy Platero | May 18, 2023 | first tuesday Local, Laws and Regulations, Real Estate, Sacramento | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

The project and the lawsuit

The City of Elk Grove, located in Sacramento County, has denied the development of a 66-unit housing project called Oak Rose Apartments, aimed at providing permanent housing at rents affordable by homeless individuals. The project met low-income parameters and was subject to a streamlined, ministerial approval process under Senate Bill (SB) 35.

The city’s denial of the housing project resulted in a lawsuit filed against the city by the California Attorney General Rob Bonta and the California Department of Housing and Community Development (HCD).

The lawsuit, filed May 1, 2023, alleges the city’s denial of the project violates state laws, including:

- SB 35 as enacted into law;

- the Housing Accountability Act (HAA);

- the Nondiscrimination in Land Use Law; and

- the Affirmatively Furthering Fair Housing statute (AFFH).

The city denied the project claiming it did not meet zoning standards making it ineligible for SB 35 ministerial review and thus the issuance of a building permit. The Attorney General’s lawsuit sought injunctive relief requiring Elk Grove to approve the project and remain compliant with state law.

While on one hand the city denied the low-income housing project, they then approved a similarly situated, market-rate housing development located within the same neighborhood. This project did not have commercial uses on the ground floor, the main claim for denial of Oak Rose Apartments, but was approved without a low-income housing component.

The state agencies’ actions are a continued effort at supporting general population access to housing in California.

NIMBYism on display

California has the largest homeless population of any state, with 161,548 people experiencing homelessness as of January 2020, according to the U.S. Department of Housing and Urban Development (HUD).

California’s acute housing shortage stems solely because of the refusal of local governments to approve low-income housing to meet the needs of, well, lower skilled employed Californians, especially families of low and moderate income.

One key factor exacerbating the housing shortage is the local desire to enforce local ordinances which are archaic, if not racist single-family zoning in conflict with preempting state housing codes. Another is local vocal opposition to enlarging the availability of housing, evidenced primarily by the not-in-my-backyard (NIMBY) sentiment politically controlling local city councils.

These local factors make it particularly difficult for any developer or builder, and investors to develop new housing supportive of workers employed locally providing necessary low-income services.

Administratively, the objective is to set a standard for implementation which allows people to live where they work, the casita arrangement of accessory dwelling units (ADUs) being an example.

The Elk Grove planning commission and city council demonstrated NIMBY sentiments when they faulted the project in this neighborhood for not being in the “proper location.” They attempted to relocate the project to a possible alternative site, though the site suggested provided fewer resources for the future residents as remote from community services.

To combat this sort of forced housing shortage, California’s Department of Justice (DOJ) established a Housing Strike Force in 2021 aimed at advancing:

- access to housing;

- availability of priced right housing;

- environmentally sustainable housing; and

- equity in California’s housing market.

Related article:

State agencies are needed with their resources to battle it out against local political jurisdictions brazenly acting to skirt state housing laws and stifle low-income housing starts. The goal here is to take politics out of the permitting process for new housing which is administrative in nature, so real estate activity has commercial certainty of attaining objectives.

California since WWII has been increasingly committed to housing all levels of society unaffected by balkanized locals seeking to bar any equilibrium in the nature of the local population. We are a state in constant movement, with a few parochial enclaves remaining.

Subscribe to the weekly Quilix for more developments on California’s housing shortage sent straight to your inbox.

Related topics:

attorney general (ag), low-income housing, not in my backyard (nimby)

Attorney General fines landlords for TPA violations

Attorney General fines landlords for TPA violations somebodyPosted by Carrie B. Reyes | Jul 7, 2023 | Fair Housing, Laws and Regulations, Property Management, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

What percentage of tenants are aware of their rent control and eviction rights under the Tenant Protection Act (TPA)?

- Less than 25% (62%, 21 Votes)

- Over half (24%, 8 Votes)

- 25%-50% (12%, 4 Votes)

- Zero (3%, 1 Votes)

Total Voters: 34

California has some of the most equality intense housing laws in the nation, partially brought about by the state’s high housing costs which has forced the majority of tenants into housing-burdened financial status. Meanwhile, landlords evict tenants or simply raise rents with conduct that is out of step with the state’s landlord-tenant laws.

From both the tenant’s and the landlord’s perspective, it is all about vying for money when housing is in very short supply. Construction starts is another method for leveling the pricing of rentals in contrast to rent control, a legislated zoning condition builders are settling into.

For four years and counting, 2019’s Tenant Protection Act (TPA) has provided the most comprehensive set of tenant-centered laws. However, the TPA got a late start with implementation and thus understanding, as pandemic-era tenant protections superseded the Act through much of 2022.

Now that the TPA is fully in effect, California’s Office of the Attorney General (OAG) as the enforcement agency is meeting resistance from landlords reluctant to follow — or simply unaware of — the rules.

Broadly, the TPA:

- caps annual rent increases at 5% plus the rate of inflation for much of California’s multi-unit residential properties; and

- requires “just cause” to evict tenants in place for 12 months or more.

The applicability of the TPA covers most multi-unit housing in California and those single family residential (SFR) units owned by a REIT, a corporation or an LLC with a corporate member. To complicate landlord compliance, numerous exemptions for multi-family units and conditions for SFRs exclude some properties.

Read more about who is exempt from the TPA.

TPA violations

Requiring a just cause for eviction creates another roadblock for landlords seeking to re-rent their properties to new tenants at a higher rate by evicting current tenants. Further, when a tenant is being evicted at no fault of their own, the landlord may be required to provide modest financial relocation assistance.

Still, while some landlords continue to work the loopholes in the TPA, others attempt to make their own loopholes.

Related article:

As one of the original authors of the TPA, the Attorney General has a special stake in making sure landlords are paying attention.

For example, the OAG recently made explicit that landlords renting to Section 8 recipients are not exempt from the TPA.

When landlords are guilty of violating the TPA, landlords may face consequences such as a:

- court trial;

- penalty fine; and

- jail term of one year or less.

For example, the OAG recently reached a settlement with a housing developer — Green Valley Corporation — for violating the TPA.

Green Valley Corporation unlawfully issued rent increases and eviction notices to its employee-tenants. Green Valley Corporation acted on the erroneous belief that the TPA did not apply to the tenants in their employ.

As part of the settlement, it will be required to pay $391,130, including:

- refunding 15 months of overpaid rent, totaling $331,130; and

- paying $60,000 in penalties to the state.

It will also return the units to the rental rates in place before the unlawful increases. Further, its staff is required to complete annual training on fair housing laws. The landlord will provide annual reports to the OAG regarding any rent increases, eviction notices and the annual training completed.

Related article:

Stay up to date with new housing laws and informed about laws being considered by the state legislature – follow the latest at firsttuesday’s Legislative Gossip page.

Related topics:

attorney general (ag), landlords and tenants, tenant protections

Bankruptcy’s tie to homeownership

Bankruptcy’s tie to homeownership somebodyPosted by ft Editorial Staff | May 3, 2023 | Charts, Economics, Forecasts, Laws and Regulations, Market Watch, Recessions | 4

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

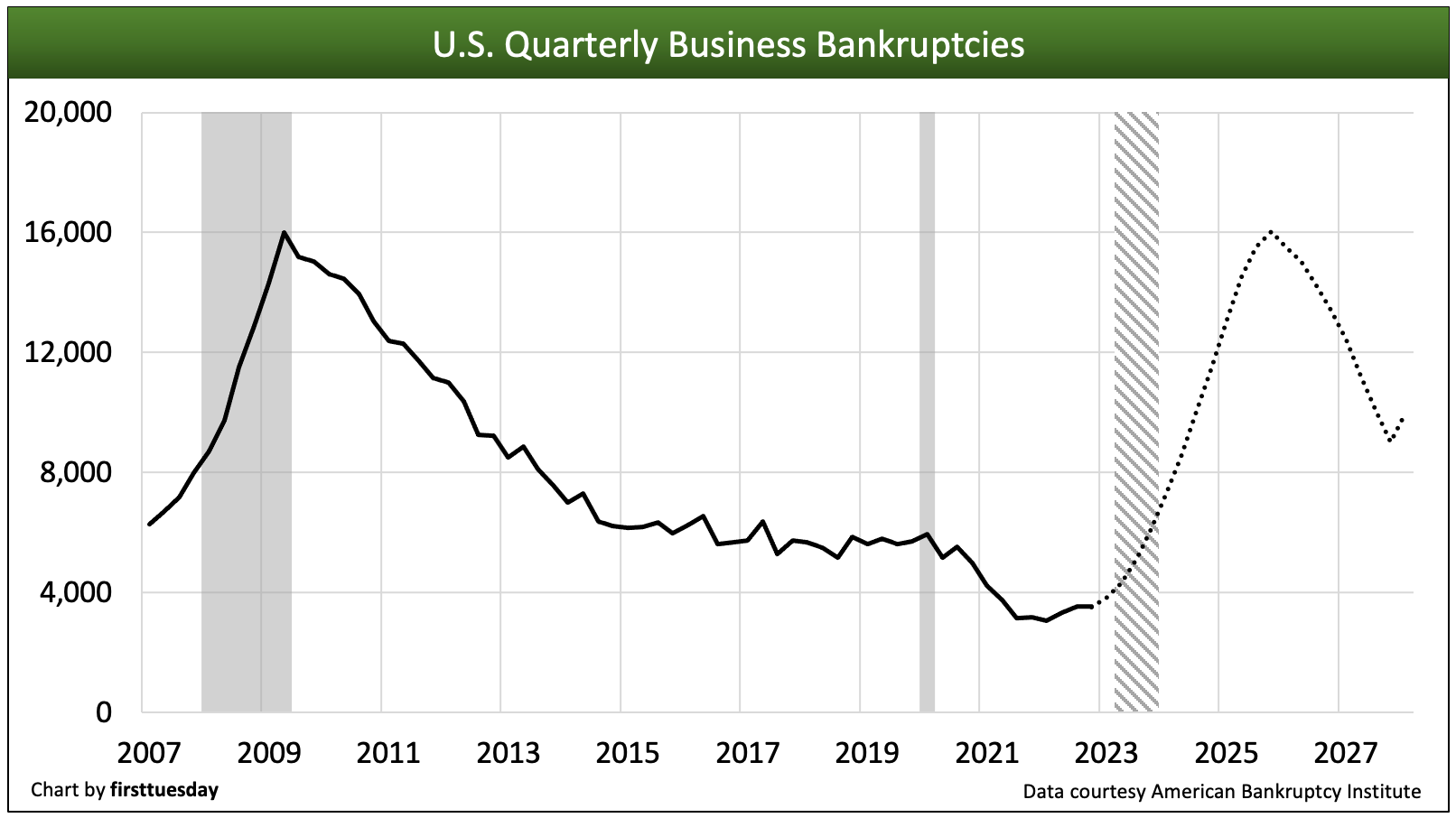

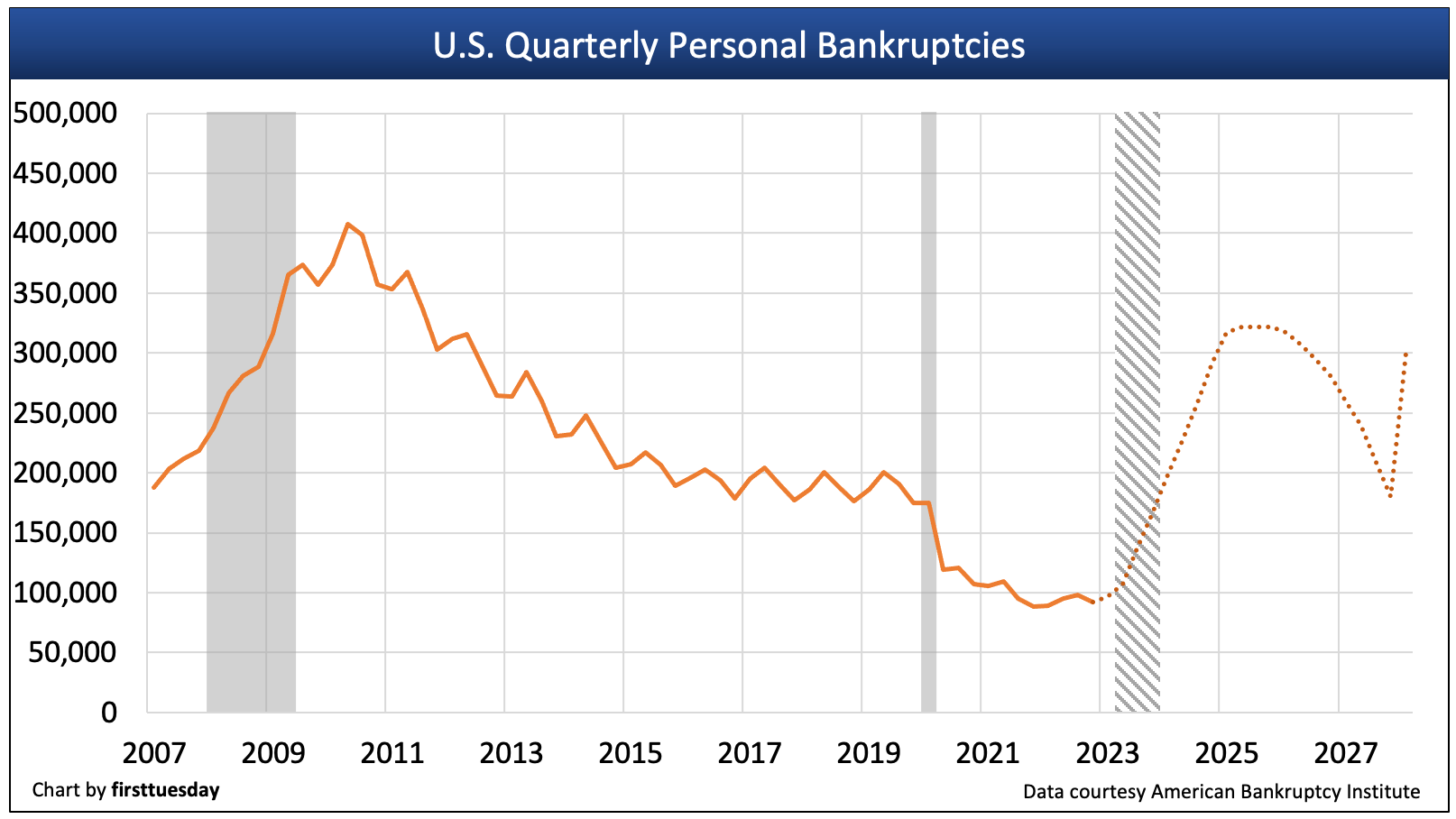

Bankruptcy filings began to inch higher during 2022, with 91,900 personal bankruptcies and 3,500 business bankruptcies filed nationwide in Q4 2022. Further, bankruptcies continue to increase in the first half of 2022, currently up 17% from a year earlier when filings were near a decades’ low.

With a below average filing share, California represents approximately 9% of the national filings versus 13% of the population.

Bankruptcies plummeted during the 2020-2021 pandemic period, despite the onset of the 2020 recession. Without pandemic interference, bankruptcies would have risen significantly, as in any recession. Businesses which otherwise would have folded found fuel in economic stimulus and rising inflation generated by the pandemic. Just 6,100 business bankruptcies were filed in California during 2021, a fraction of the 63,200 filings that were recorded during the 2011 peak of the 2008 recession. In 2022, this number increased to 6,800 business bankruptcies.

When it comes to recessions, bankruptcy numbers tend to be a lagging indicator. That is, many businesses hold on until they run out of cash, bleeding off market share as disruptors to a recovery while they exist as zombie businesses. Eventually they give in to market forces and throw in the towel. Compared to businesses, bankruptcy offers few benefits for individuals, though bankruptcy proceedings extend the foreclosure process by several months.

In 2023, the economy is rapidly contracting as the curtain opens on the second act of the 2020 recession. In 2020-2021, government stimulus bridged the pandemic gap for most individuals and businesses lacking the financial foundation to weather a recession — hence the artificially low bankruptcy numbers resulting in a buildup of bankruptcy candidates. But with the effects of stimulus now in the rearview, the recession — expected to officially arrive in the second half of 2023 — will deliver the killing blow for those lacking sufficient cash reserves or equity. The result will be a cyclically disproportionate rise in bankruptcy filings in the next three years.

For the housing market, the reduction in home sales volume which began dramatically in 2022 paced by rapidly doubling interest rates will see home values fall to wipe out the past four+ years of home price increases. Homeowners who see their home values diminish are more likely to go bankrupt when household financial stress occurs. As the struggle for ascertaining home values takes root and buyers simply wait for prices to bottom and hold, expect more personal and business bankruptcies to occur, expected to peak around 2026.

Updated May 3, 2023. Original copy released January 2010.

Chart update 05/03/23

Chart update 05/03/23

| Q4 2022 | Q4 2021 | Q4 2020 | |

| Personal Bankruptcies | 91,900 | 88,300 | 107,400 |

| Business Bankruptcies | 3,500 | 3,200 | 5,000 |

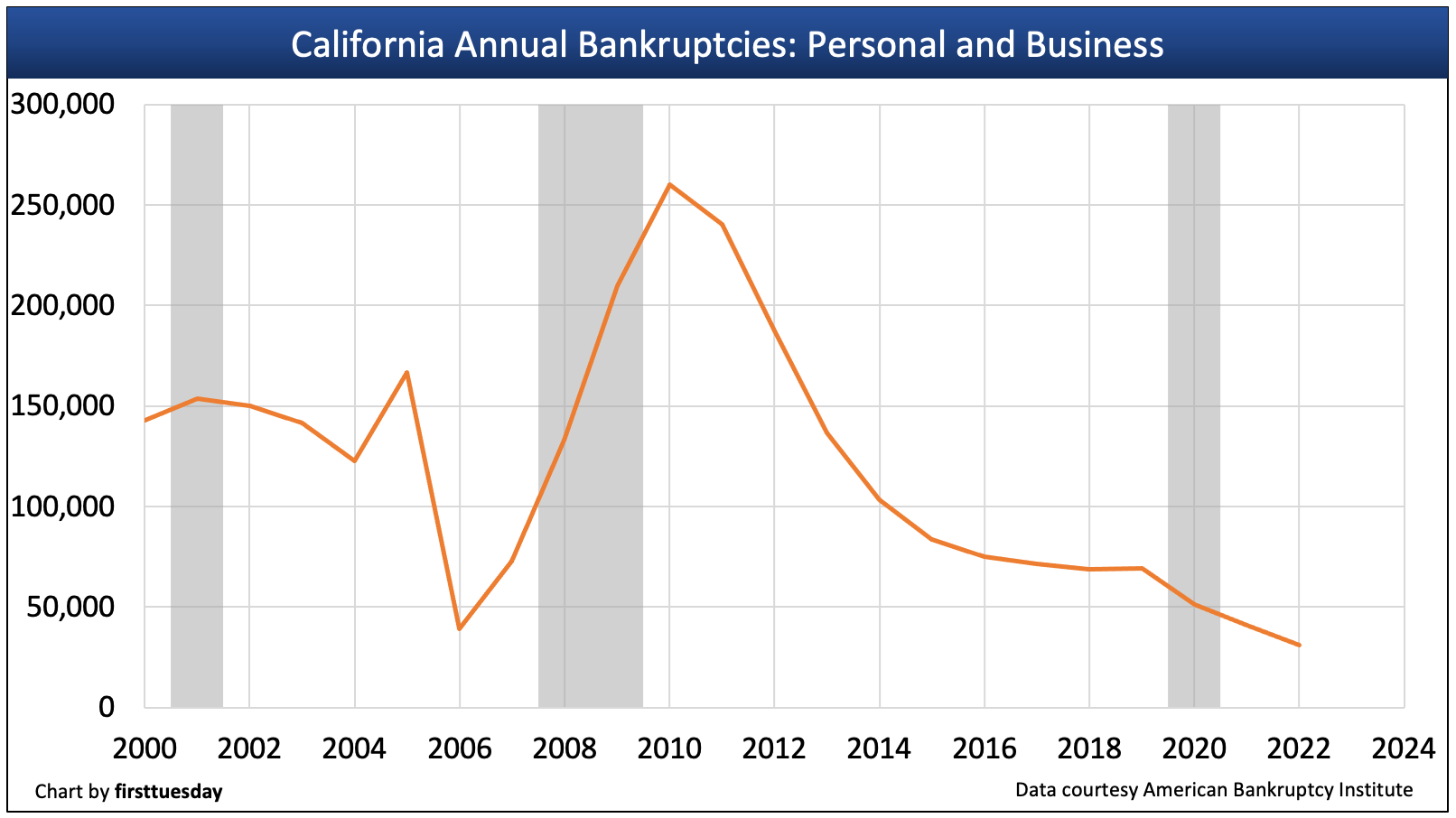

Dashed lines are firsttuesday’s forecast. The number of bankruptcy filings has decreased each year since the end of the Great Recession. By the end of 2014, personal bankruptcy levels had fallen below the average levels seen during the 1990s and early 2000s, where they remain today. California districts with the highest number of bankruptcy filings in 2021 were:

- Central California, with 20,300 personal bankruptcies and 2,800 business filings;

- Los Angeles, with 8,500 personal bankruptcies and 3,300 business filings; and

- Riverside, with 6,000 personal bankruptcies and 700 business filings.

The majority of these personal bankruptcy filings were completed through Chapter 7.

Chart update 05/03/23

Chart update 05/03/23

Two forms of bankruptcy

Two separate bankruptcy procedures exist, both governed by federal law.

Chapter 7 bankruptcy requires the insolvent homeowner in bankruptcy to repay their debt from whatever assets they possess, unless those assets are lower than state-allowed levels of assets and income. In Chapter 7 bankruptcy, a home without equity is counted among these assets, and foreclosed upon.

Chapter 13 bankruptcy, on the other hand, requires the homeowner to repay their delinquent debts over a longer period of time than contracted for, after deducting reasonable living expenses.

The Chapter 13 repayment plan can include the homesteaded sale of the owner’s home, if the home has any equity in the home. Bankruptcy law no longer permits a homeowner’s mortgage to be reduced by a bankruptcy court (a cramdown, or principal reduction). However, Chapter 7 bankruptcy voids any deficiency obligations on recourse mortgage refinancing, just as it voids all unsecured debt with a value exceeding the amount of the homeowner’s nonexempt assets.

In addition to putting an immediate stop to lender collection efforts, the process of filing bankruptcy allows a homeowner to pay delinquent mortgage payments over a three-to-five year period. Troubled homeowners often choose to file Chapter 13 Bankruptcy to discharge their non-mortgage (unsecured) personal debts, and then use the newly freed funds to make future payments on their mortgages.

Homestead exemption protections

Bankruptcy laws do enforce California homesteads. For positive equity homeowners, this exemption acts as an incentive to file bankruptcy to avoid unsecured debts and free up cash by making it available under the homestead.

On the other hand, the homestead exemption has no effect on the priority or payment of an owner’s mortgage. The bankruptcy process adversely affects lenders who have obtained involuntary liens (judgment liens) against the homeowner’s title.

In 2021, California homeowners qualify for a net equity homestead protection of:

- up to $300,000; or

- the median sale price for a single family residence (SFR) in the homeowner’s county in the calendar year prior to the year in which they claim the exemption, not to exceed $600,000 (adjusted annually for inflation). [CCP §704.730]

Related article:

Bankruptcy and foreclosure

The most important aspect of bankruptcy, from the point of view of mortgage lenders, is the “automatic stay” provision. This provision of bankruptcy law also delivers the most direct and immediate results for troubled homeowners. Any owner who files bankruptcy immediately places an automatic stay on all collection efforts, including foreclosure sales.

Lenders prefer to quickly move to a foreclosure sale, take title to the property or what proceeds they can and cut their losses, and are thus hamstrung by the automatic stay provision. They are forced to wait until a bankruptcy court allows them to proceed. The stay provision increases the lender’s costs of dealing with a homeowner who does not maintain their mortgage payments while in bankruptcy.

On average, filing Chapter 7 bankruptcy extends the foreclosure process from six months to a year. Chapter 13 delays the foreclosure sale even longer, often drawing it out to a year and a half. A homeowner who files bankruptcy without the ability to make payments on their mortgage merely extends the time before the eventual foreclosure sale. For the lender, the bankruptcy process increases the risk the home will be damaged or otherwise devalued before the sale takes place, increasing the lender’s eventual loss.

Lenders thus have a vested interest in government regulations that make it difficult for homeowners to obtain relief on their mortgages in bankruptcy, and they intend to keep their hard fought gain of a cramdown-free bankruptcy law intact. Lenders don’t want the threat of a bankruptcy judge endowed with the power to reset the loan balance at exactly the amount the security for the loan is worth (which, of course, is all the lender can expect to get from foreclosure anyway).

When bankruptcy is unavoidable, lenders want to get out of bankruptcy court as quickly as possible. Often they can be persuaded to agree to a short sale in order to hasten the process and cut their losses. Bankruptcy can thus be an effective way for homeowners to force the lender’s hand.

Costs and benefits of bankruptcy

So does filing bankruptcy, and thereby discharging unsecured debt and putting off a potential foreclosure sale, actually help homeowners pay their mortgages, or do the other costs of bankruptcy cancel out the benefits?

Evidence is mixed, but homeowners and their attorneys certainly seem to believe that bankruptcy can be beneficial. Troubled homeowners already make up the majority of those who file for Chapter 13 bankruptcy (studies in other states found that over 80% of filers were paying for homes with a loan to value ratio (LTV) over 90%).

Of the total number of homeowners who file bankruptcy, only about 33% successfully kept their homes, according to the Federal Reserve Bank of Philadelphia. It is certain that bankruptcy does, at least on occasion, have a positive effect for those desperate homeowners who turn to it as a last resort, and it is also sure that bankruptcy will almost always have a negative effect for lenders.

Equally important, homeowners who file for bankruptcy will find later that their past bankruptcy interferes with their future ability to qualify for mortgage financing.

Related topics:

bankruptcy, chapter 13 bankruptcy, chapter 7 bankruptcy, foreclosure, income, lien, mortgage, tenant

California Attorney General clashes with NIMBYs in Huntington Beach

California Attorney General clashes with NIMBYs in Huntington Beach somebodyPosted by Carrie B. Reyes | Mar 23, 2023 | Laws and Regulations, Los Angeles-Santa Barbara-Ventura, Real Estate | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

The fight over California’s housing density laws is just getting started. The newest saga features Huntington Beach, the coastal community known for its surfing competitions, conservative politics and now, their “no casitas allowed — ever” stance.

The City Council recently instructed the city to stop processing permit applications for accessory dwelling units (ADUs) and projects submitted under The HOME Act of 2021 – SB 9. At the same time, it directed the City Attorney to take legal action to challenge any and all “laws that permit ADUs.”

This came on the same day California’s Office of the Attorney General (OAG) and Department of Housing and Community Development (HCD) issued letters to the Council urging them to repeal their unlawful ADU moratorium ordinance.

The HOME Act aims to ease the process for homeowners to create a duplex or subdivide their single-family residential lot into up to four units. Now, as permitted by statewide zoning codes, homeowners may:

- split their lot into two parcels — each parcel may be no smaller than 1,200 square feet and no smaller than 40% of the original lot; or

- build duplexes — a project containing up to two dwelling units on each single-family parcel. [Government Code 66411.7 (a)]

However, as essentially an elimination of single family zoning, the HOME Act has met opposition from various conservative enclaves across the state, with Huntington Beach the latest bastion to willfully ignore state law.

But Huntington Beach wasn’t done.

Next, the City Council introduced an ordinance to unlawfully exempt the city from the Builder’s Remedy enacted by California’s Housing Accountability Act (HAA). The HAA streamlines approval for low- and moderate-income housing developments in cities which have not produced a compliant housing element to include sufficient low- and mid-tier housing for its residents (and, you guessed it, Huntington Beach does not have a housing element compliant with state laws).

Following the Council’s refusal to heed the OAG’s warning, the OAG sued the city, including a request for the court to issue a monetary fine on the Council members.

As the awareness that state codes really do preempt local ordinances, made clear by the OAG’s legal action, has quickly escalated, the Council is backpedaling. They are now considering a plan to reopen permit applications for ADUs and for parceling under the HOME Act, and amend its Housing Element to comply with state law.

For those counting, this is the second time the state has sued Huntington Beach over housing law violations, the first of which the city settled in 2020 after losing out on millions of dollars in state funding.

Related article:

Strict zoning restricts fees

California’s housing crisis is ultimately the result of tight local zoning ordinances, which include restrictive:

- land use regulations;

- parking restrictions;

- lot size minimums;

- height limitations; and

- permitting costs and processing times.

With all these restrictions, builders looking for a “sure thing” tend to stick to single family residences (SFRs) on post-WWII lot sizes. With large lots restricted to a single unit on a parcel suitable in all ways for eight residential units, the inefficiencies created have resulted in a reduced housing supply. In fact, each year since 2018 there have been more SFRs constructed in California than multi-family units.

The end result is less housing — an intentional supply-and-demand imbalance — which has led to reduced homeownership, higher rents, and a lower quality of life for California’s owners and renters. Home sales have been in the doldrums for years, and that has hurt those servicing the housing market’s needs.

We need more housing units — not more occupants per unit.

Going forward, housing laws have now shifted from local control to a statewide housing policy. Legislation has focused on loosening zoning, seizing the reins from the hands of vocal not-in-my-backyard (NIMBY) advocates, and allowing private property owners to make their own choices to add an ADU or subdivide their lot — not the city fathers.

But when cities like Huntington Beach seek to sidestep the progress made by the state legislature for residents to live where the jobs are, our population’s housing preferences are artificially stifled.

Demand for more low- and moderate-income rentals is alive and well, even in today’s restrained housing environment which has seen sales volume and pricing plummet from their mid-2022 peak. Further, demand for low- and mid-tier for-sale inventory will rebound soon enough, likely around 2026 when prices will cyclically resume their upward trajectory after reaching a base-value price.

Related article:

Real estate brokers understand the state’s anemic housing inventory has only held back transaction volume in recent years — and know that increasing the number of housing units will open up more opportunities for their fee-based brokerage services.

The housing shortage will be solved only when residential construction is allowed to rise to meet the level of demand for additional housing in every neighborhood – no matter its purported social status. This organic growth will gradually occur as California’s Home Act legislation allows builders to catch up — but only when local governments cooperate, voluntarily or by court order.

When city councils are not cooperative, the AG has the tools and the willingness to help homeowners become mini-landlords, free up builders from permit processes barricaded by city councils and allow employees to live where they work.

What’s more, the AG seems hungry for a fight.

Related article:

Related topics:

accessory dwelling unit, attorney general (ag), not in my backyard (nimby)

California is experiencing unlawful telemarketing practices — are you in compliance?

California is experiencing unlawful telemarketing practices — are you in compliance? somebodyPosted by Carrie B. Reyes | Aug 18, 2023 | Laws and Regulations, Mortgages, Real Estate, Your Practice | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Economic stress has many real estate licensees considering how to connect with previously untapped clientele.

As part of their financial strategy to stay afloat despite reduced sales and leasing of property and origination of mortgages, brokers, agents and mortgage loan originators (MLOs) are doubling down on their solicitation efforts by FARMing past contacts — and others.

But in their rush to reach new and prior clients, these adaptive licensees may have missed an important step or two to comply with telemarketing and advertisement laws. The rules are simple and straightforward.

California’s attorney general recently announced a crackdown on illegal telemarketing, highlighting a number of lawsuits and court rulings against companies guilty of deceptive marketing practices.

Marketing and advertising are a fundamental part of a licensee’s ultimate business success. Potential clients need to be made aware of the licensee’s services. The telemarketing rules permit the achievement of this success while applying guardrails for reasonable conduct in disclosures and timing of calls to customers.

In application, MLOs who use phone calls as part of their marketing need to take note of and follow telemarketing rules.

We will explain.

Telemarketing rules for MLOs

Telemarketing by an MLO is any marketing campaign conducted by telephone to induce consumers to apply to originate a mortgage.

The conduct of an MLO’s telemarketing campaign is regulated and enforced by the Federal Trade Commission (FTC) under their Telemarketing Sales Rule. [16 Code of Federal Regulations §§310]

For starters, an MLO telemarketer must understand that deception is wrongheaded; they may not make false or misleading statements to induce the consumer they call to accept the mortgage the MLO is promoting. [16 CFR §310.3(a)(4)]

Further, the MLO placing a call must immediately, when the person called answers, orally disclose their:

- identity — name of the MLO and their employer;

- purpose of the call as soliciting a mortgage origination application; and

- nature of the particular type of mortgage origination offered on the call. [16 CFR §310.3(d)]

An MLO placing telemarketing calls must also — without first being asked — voluntarily disclose to the person they are calling:

- all costs incurred, directly or indirectly, to originate the specific type of mortgage offered;

- any restrictions or limitations on the use of the funds provided by the mortgage offered;

- conditions for processing the mortgage origination which alter the MLO’s or their employer’s ability to originate the offered mortgage without incurring greater costs, efforts and time;

- any affiliation of the MLO or their employer with any person or government agency including the mortgage lender or originator; and

- in a prize promotion, any conditions regarding receiving a prize, the odds of winning the prize, and that no mortgage origination is required to participate. [16 CFR §310.3(a)(2)]

Time of day avoids abusive call rule

A telemarketing call placed without prior consent is permitted by the Telemarketing Sales Rule. Permitted calls may only be made between 8:00 a.m. and 9:00 p.m. for the time at the location of the person receiving the call. A call placed at any other local time without prior consent constitutes a violation as abusive telemarketing. [16 CFR §310.3(c)]

Further, it’s not enough for an MLO to simply comply with FTC rules for acceptable telemarketing practices. Any MLO who knowingly supports or facilitates a violation of these rules by others — even the company they work for — is also in violation. [16 CFR §310.3(b)]

Related video:

Advertising rules for real estate licensees

Advertising introduces and fully identifies the licensee, their activities and services, and the message they want to convey to potential clients. Advertising is a form of communication which uses signs, symbols or actions to create brand awareness and promote a positive image of the licensee.

While telemarketing rules do not apply to material mailed by the MLO or their employer in marketing campaigns which intend to induce the recipient to call about their mortgage origination services when the mailing contains the physical business address of the MLO’s employer, there are additional rules that apply to these mailed advertisements.

When advertising on a website, in print or otherwise, real estate licensees are required to provide their:

- name;

- Department of Real Estate (DRE) license number;

- Nationwide Mortgage Licensing System (NMLS) ID number (when applicable); and

- responsible broker’s identity. [Calif. Business & Professions Code §10140.6]

Solicitation materials licensees use where these requirement apply include:

- business cards;

- stationary;

- websites owned and maintained by the soliciting real estate licensee;

- promotional and advertising flyers, brochures, postal mail, leaflets and FARM letters;

- advertisements in electronic media (including internet, email, radio, cinema and television);

- print advertising in any newspaper or periodical; and

- “for sale,” “for rent,” “for lease,” “open house,” and directional signs that display the name of the licensee. [DRE Regs. §2773]

Noncompliance by an agent or employing broker may result in:

- disciplinary action by the DRE;

- criminal prosecution; or

- both DRE disciplinary action and criminal prosecution.

For more information about advertisement compliance, see the DRE’s Real Estate Advertising Guidelines informational booklet DRE’s website. [See RE 27]

Related article:

Related topics:

advertising, mortgage loan originator (mlo)

California targets unlawful crime-free housing policies

California targets unlawful crime-free housing policies somebodyPosted by Carrie B. Reyes | May 24, 2023 | Fair Housing, Property Management, Real Estate | 1

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

Has the California Attorney General’s Housing Strike Force caused more residential units to be built in your local housing market?

- No (79%, 11 Votes)

- Yes (21%, 3 Votes)

Total Voters: 14

California’s Office of the Attorney General (OAG) is warning local governments about housing policies that conflict with state and federal anti-discrimination laws.

Several of the state’s local Crime-Free Housing Policies violate fair housing laws by targeting members of protected classes. The OAG is calling on local jurisdictions to either amend or repeal these policies, including any training programs or materials which unfairly target protected classes.

This guidance is a follow-up on a notice from the U.S. Department of Housing and Urban Development (HUD) which states that seemingly neutral Crime-Free Housing Policies can violate the federal Fair Housing Act (FHA) when they have a discriminatory effect and are “not supported by a legally sufficient justification.”

California’s fair housing law is more extensive than federal law in providing consumers equal status and protection. California prohibits discrimination in the sale or rental of housing accommodations based on an individual’s:

- race;

- color;

- religion;

- sex;

- gender;

- gender identity or expression;

- sexual orientation;

- familial or marital status;

- disability;

- genetic information;

- national origin;

- source of income;

- veteran or military status;

- ancestry;

- citizenship;

- primary language; or

- immigration status. [Calif. Government Code, §§ 12955; Calif. Civil Code §§51 et. seq.; Calif. Government Code §12955; DRE Reg. §2780 and §2781]

However, as noted by HUD and now the OAG, even when a landlord follows the letter of the law, discriminatory effects may occur when they selectively refuse to rent to a tenant based on their criminal history.

While a landlord may consider criminal activity in their screening of tenants, landlords are prohibited from enforcing blanket bans against prospective tenants or evicting tenants due to a criminal record.

Editor’s note — Assembly Bill 1418 is currently being considered in California’s legislature. This bill prohibits local governments from encouraging landlords with their crime-free housing policies to perform a criminal background check on a tenant or prospective tenant. Stay tuned for updates by following firsttuesday’s Legislative Gossip page.

Critically, landlords may not apply their crime-free policies in a discriminatory manner. For example, a landlord who only screens tenants for criminal history when they are a certain race, age, sex or other protected class is considered intentional discrimination.

Implicit discrimination is overtly discriminatory

Though tenants with a criminal history are not a protected class under fair housing laws, criminal record-based housing restrictions are used to disparately impact racial minorities — a protected group. Denying applicants who have any criminal record disproportionately impacts racial minority and low income groups which are convicted and incarcerated at higher rates — a discriminatory effect in violation of fair housing laws.

Thus, even when a landlord is not being explicitly discriminatory, housing restrictions based on a tenant’s criminal history are violations of California’s Fair Employment and Housing Act (FEHA) and the federal Fair Housing Act (FFHA), which separately expose a landlord to civil liability. This is a form of unintentional, or implicit discrimination everyone needs to learn to observe. [Gov C §12900, et seq.; 42 United States Code §3601, et seq.]

Further, landlords cannot refuse to rent to prospective tenants or evict existing tenants they suspect of having gang affiliations or who “appear” to be involved in criminal activity. Such a screening practice encourages arbitrary and unlawful housing discrimination on the basis of race, ethnicity, family composition, gender and appearance. [Castaneda v. Olsher (2007) 41 C4th 1205]

Editor’s note — The only exception to these guidelines occurs when a tenant has a conviction for the manufacturing or distribution of controlled substances. Here, a landlord may deny housing based on a conviction for drug manufacturing or distribution — though not based on a conviction for possession — without violating fair housing laws. [42 USC §3607(b)(4)]

Thus, landlords who impose blanket bans on applicants with any criminal record are subject to civil penalties and tenant money losses for housing discrimination.

Related article:

Reporting suspected housing discrimination

California’s Civil Rights Department (previously the Fair Employment and Housing Department) is the agency which enforces anti-discrimination housing law. [Gov C §§12901, 12903, 12930, 12935]

Any individual who feels they have been discriminated against may file a complaint with the Department. The Department investigates the complaint to determine any wrongful conduct. When grounds exist, the Department then seeks to resolve the situation through discussions with the individual against whom the complaint is made. [Gov C §12980]

When the Department believes a discriminatory practice has occurred, it will first attempt to reach a resolution through the Department’s mandatory dispute resolution division. The dispute resolution is provided without charge to either party. However, when the dispute cannot be effectively resolved, the Department will file a civil action on behalf of the individual who was discriminated against in the county where the discriminatory conduct is alleged to have occurred. [Gov C §12981]

Read more in the RPI ebook: Implicit Bias, Office Management & Supervision, Agency, Fair Housing, Trust Funds, Ethics and Risk Management.

Related topics:

criminal activity, housing discrimination, implicit bias, landlords and tenants

California voters approve new measures to combat housing shortage locally

California voters approve new measures to combat housing shortage locally somebodyPosted by Ashley Collins | Jan 16, 2023 | Laws and Regulations, Real Estate | 3

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

When it comes to California’s housing crisis, residents are saying enough is enough.

Last November, Californians voted on transformative housing measures in their cities amid a long-simmering statewide shortage. The 2022 midterm election highlighted voters’ growing displeasure with priced right housing, but the results also renew optimism as the state pivots its policies for 2023 and beyond.

Voters focused their ire on local zoning, tax and homelessness issues. Read on for the most critical housing-related measures passed in November 2022 across California’s major metros. Find your service area below for a breakdown of the changes impacting your practice.

In Los Angeles, residents voted “yes” on:

- Measure LH — earmarking public money to aid the development of an additional 5,000 low-income rental units per city council district;

- Measure EM — authorizing the rent control board to modify or reject annual rent adjustments during a state of emergency declared by the president, governor, LA public health officer, or city council;

- Measure H — enacting a rent control program limiting annual rent increases to 75% of consumer price index (CPI); and

- Measure RC — requiring residential landlords to intend occupancy for a minimum of two years, move in within 60 days of vacancy to evict a tenant, and reduce the rent increase cap to $70 per month.

In Orange County, voters approved:

- Measure K — allowing the city council in Costa Mesa to adopt publicly-reviewed land use plans to refresh areas, expand low- and mid-tier housing, and restrict building height.

In Riverside County:

- Measure K — passes the fee of 15 cents per building square foot on single-family residential (SFR) units, the authorization of bonds, and an appropriation limit of $39 million.

In San Diego County, voters secured:

- Measure B — ends free trash pick-up for single-family units; and

- Measure C — places a 30-ft. height limit on buildings in most areas west of Interstate 5, according to the San Diego Union-Tribune.

In Sacramento County, residents can look forward to:

- Measure D — allows the county to develop low-income housing equal to 1% of its existing housing, according to Sacramento County.

- Proposition M — enforces a tax, at a rate between $2,500 and $5,000 per vacant unit, on owners of vacant residential units in buildings with three or more units when the units have been vacant for more than 182 days in a year.

Lastly, Santa Clara County voters said “yes” to:

- Measure M — imposes a parcel tax of $348 per parcel for 8 years to fund schools; and

- Measure A — adjusts zoning regulations to disallow construction with characteristics of new storage and distribution use.

Editor’s note — For an exhaustive roundup of California’s midterm election results, visit Ballotpedia.

Taken individually, these changes represent only incremental steps toward more priced right housing for low- and middle-income earners. But together, these policy changes reflect residents’ roiling frustration with cities to do something about housing costs. Perhaps the biggest mandate to emerge from the midterm’s results is on homelessness.

Related article:

Measures for housing the unhoused

While homes prices and sales volume swelled during the pandemic, so too did the number of California’s unhoused. In fact, the state’s unhoused population rose by 22,500 between 2019 and 2022 — a conservative figure to be sure. But the passage of a few notable housing measures across the hardest-hit counties is turning compassion into legislative action.

To alleviate the homelessness crisis in their counties, voters passed:

- Measure ULA in Los Angeles, which raises nearly $1 billion annually for housing and homelessness efforts by taxing property sales of $5 million or more;

- Measure S in San Diego, which raises sales tax by one penny to aid the homelessness crisis;

- Measure O in Sacramento, a new homelessness policy that requires a minimum number of emergency shelter spaces based on number of unhoused individuals, prohibits encampments, and limits the city’s annual budget of $5 million;

- Measure B also in Sacramento, creating gross receipt tax from cannabis and hemp businesses to fund county homelessness services; and

- Proposition C in San Francisco, which creates a Homelessness Oversight Commission to oversee the Department of Homelessness and Supportive Housing and requires the city controller to conduct audits of services for people experiencing homelessness.

Though these measures ensure funding for vital homelessness programs and services, they do not directly address the root of the issue: California’s housing inventory shortage. The state is about 2 million units short of meeting demand, according to a landmark McKinsey & Company report.

Ultimately, only increasing housing inventory and production will make a long-term material impact in the prevalence of homelessness across California neighborhoods. This means clearing obstacles to construction starts, which are sluggish going into 2023.

At the local level, the housing bottleneck starts early — in the planning stage. Vocal not-in-my-backyard (NIMBY) advocates have long wielded outsized power in city council meeting, killing residential construction projects in their neighborhoods despite an urgent need for greater density.

Related article:

The market braces for impact

Though the state’s emergency response ended in 2022, the pandemic disruption will still ripple through 2023. Agents and brokers can expect inflation, mortgage interest rates, and evaporating sales volume to continue dominating 2023’s news cycle. It’s no surprise that many of the midterm’s housing measures were created in response to these forces.

Consider Measure EM and Measure H in Los Angeles. Both measures address rent control in response to housing price spikes fueling gentrification across the state. As home and rental prices spiked, many Californians lost their jobs and their ability to cover housing costs. This prompted a renewed push by YIMBY advocates to combat restrictive housing policies in desirable residential areas.

Housing policies informed by the pandemic’s economic lessons are finding their way into legislation as the state level as well. Senate Bill (SB) 6 and Assembly Bill (AB) 2011 encourage builders to transform office and retail commercial spaces into housing units for low- and middle-income earners.

Surviving (and thriving) during the 2023 recession means staying on top of shifting economic and legislative environments. Be the first on your team to pivot with California’s market and laws by subscribing to Quilix, the weekly firsttuesday real estate newsletter.

Related article:

Related topics:

housing crisis, housing shortage, nimby, rent control

Cancellation excuses further performance

Cancellation excuses further performance somebodyPosted by Carrie B. Reyes | Mar 2, 2023 | Buyers and Sellers, Feature Articles, Market Watch features, Real Estate, Your Practice | 0

Reprinted from firsttuesday Journal — P.O. Box 5707, Riverside, CA 92517

This article explains when a buyer or seller is entitled to exercise their right to cancel a purchase agreement and escrow instructions, such as on a breach or failure of an event to occur or condition to be approved.

The recession wave of buyer cancellations

Over the past decade, home sellers — and their agents — have had the luxury of home sales being a virtual guarantee. If you list it, they will come. Easy.

That is, until 2022 when the bubble of buyer irrational enthusiasm — or fear — popped, and home sales volume and prices began what will be a prolonged crash.

In a falling price environment, the certainty of a quick and easy sale for real estate listings is a thing of the past. As buyers already in escrow see equivalent homes listed below their contract price, they are more likely to find reasons to back out. Likewise, willing buyers may succumb to job losses during the pending recession, losing access to funding.

What are the situations when a breach or failure of conditions in provisions of a purchase agreement entitles a buyer or seller to exercise their right to cancel?

Further, how can you distinguish a unilateral cancellation to terminate further performance under a purchase agreement from a bilateral rescission of a purchase contract — which restores the buyer and seller to their respective positions before entering into their purchase agreement?

Exercising the right to terminate the deal

Consider a seller who agrees to carry back a note secured by a trust deed junior to an existing mortgage the buyer will assume. The purchase agreement entered into with the buyer contains a further-approval contingency provision which grants the right to cancel the transaction to:

- the seller when the buyer’s creditworthiness is unacceptable to the seller [See RPI Form 150 §8.5]; and

- both the buyer and the seller when either one disapproves of the existing trust deed lender’s terms for an assumption of the mortgage by the buyer when the terms offered exceed the mortgage parameters agreed to in the purchase agreement. [See RPI Form 150 §8.6 and 10.3]

On the seller’s receipt of the buyer’s credit application form, the seller’s agent orders and receives a report on the buyer’s creditworthiness from a credit reporting agency. [See RPI Form 302]

Editor’s note – One such source of a comprehensive credit report is Tenant Screening Center. More information is available from their website.

The seller, on review of the credit report information with their agent, is concerned about the buyer’s payment history. The seller’s agent acts on these concerns by asking the buyer for financial statements including:

- a balance sheet listing assets and liabilities [See RPI Form 209-3] and

- an end-of-year financial statement on the buyer’s income and expenses for the past two calendar years.

The buyer promptly supplies the requested financial data. The seller notes the buyer is cash poor with insufficient cash on hand to make the down payment called for in the purchase agreement.

Meanwhile, the seller’s agent learns the buyer is going to use a line of credit at a bank to finance the down payment. This debt-leveraging information when known to the carryback seller might affect their decision to exercise their right to cancel the transaction under the credit approval contingency. Thus, the seller’s agent relays the information to the seller.

The seller now has all the relevant credit information readily available or known to the seller’s agent. The seller determines they have justification for exercising their option to cancel the purchase agreement and escrow instructions. However, the seller has not yet decided what to do about allowing the transaction to continue.

Related article:

Review data and respond timely

The seller’s agent is mindful of the upcoming expiration date of the seller’s right to cancel and of their duty to protect the interests of the seller. Seeing their client’s inaction, the agent advises the seller that when they do nothing to cancel before the expiration of their right, they will lose their ability to be excused from completing the transaction as agreed.

Thus, a choice is made through inaction.

The seller understands they need to serve the buyer with a notice of cancellation before the expiration date stated in the contingency provision. Otherwise, the period for cancellation will expire and they will need to proceed to close escrow. [See RPI Form 183]

By the expiration date of the seller’s right to cancel, the seller decides to do nothing. The seller is willing to undertake the additional risks, including the possible need to foreclose presented by the buyer’s insufficient creditworthiness to become owner of the property subject to the seller’s carryback mortgage.

Meanwhile, the existing mortgage lender processes the buyer’s application to assume the mortgage and forwards assumption documents to escrow for the buyer to sign and return. The terms for an assumption demanded by the lender include:

- a modification of the interest rate to current rates;

- a new payment schedule for amortization; and

- a fee extracted for allowing the assumption.

However, these terms exceed and are more financially burdensome than the mortgage assumption parameters agreed to in the purchase agreement.

Related article:

Carryback seller’s refusal to subordinate

The buyer promptly signs the mortgage documents and returns them to escrow, along with the assumption fee demanded by the mortgage holder. Thus, the buyer, by conduct inconsistent with their right to cancel granted by the mortgage assumption contingency provision, waives their right to cancel the transaction.

The buyer now no longer has the authority to terminate the purchase agreement based on excessive financial demands by the mortgage holder to allow an assumption than agreed to in the purchase agreement. [See RPI Form 150 §10.3]

Meanwhile, the carryback seller determines the terms for assumption and modification of the existing mortgage are financially unacceptable and that they exceed the parameters of the mortgage assumption terms agreed to in the purchase agreement. The seller instructs their agent to prepare a notice of cancellation to terminate the transaction and escrow. The notice is immediately signed by the seller and delivered to the buyer and escrow, called a unilateral cancellation. [See RPI Form 183]

Here, the seller has a valid reason for refusing to subordinate. The risk of loss presented by the mortgage modification accompanying the assumption agreement is greater than the risks presented by the terms agreed to in the purchase agreement.

The seller’s notice of cancellation terminates the purchase agreement and escrow. Cancellation avoids any further performance of the purchase agreement or escrow instructions by the seller and buyer since all obligations to close escrow have been excused.

As authorized to cancel unilaterally

Unilateral cancellation of a real estate purchase agreement and escrow instructions may be initiated by a seller or buyer due to:

- a material breach of the agreement by the other participant; or

- the failure of an event to occur or a condition to be approved as called for in a contingency provision in the agreements.

Unilateral cancellation eliminates whatever remains to be performed under the purchase agreement, called a termination of the contract. Thus, a cancellation abolishes any future enforcement of the agreement by either participant from the moment of cancellation.

Here, the purchase agreement is cancelled by a unilateral act since the cancellation is achieved by one participant acting alone.

Further, the cancellation of a purchase agreement does not alter the consequences of any liability for activities and events which precede the cancellation.

Conversely, a rescission of either an unexecuted purchase agreement (i.e., escrow has not yet closed) or of a completed real estate transaction (i.e., escrow has closed) is a bilateral agreement. As a bilateral rescission, both the buyer and seller act in concert to retroactively annul the purchase agreement as ineffective from the moment it was entered into.

Alternatively, a cancellation brings a purchase agreement and escrow instructions to a standstill. Only future obligations under the agreement are eliminated.

In contrast, a rescission returns the buyer and seller to the respective positions they held prior to entering into the purchase agreement. When a contract is rescinded, it is as though the participants had never agreed to the transaction. The retroactive return to their former, pre-contract positions is called restoration.

When both the buyer and seller enter into a rescission agreement, the buyer and seller are restored to their pre-purchase agreement positions. Thus, a rescission eliminates all claims they may have had against each other for conduct which occurred after entering into the purchase agreement and prior to its rescission.

A rescission is a mutual agreement, entered into voluntarily, which eliminates the purchase agreement, by a buyer and seller executing a release and waiver agreement. [See RPI Form 181]

This episode digests agency disputes which arise between the agent and their client after a purchase agreement has been entered into, and principal disputes between the buyer and seller.

Escrow instructions cancelled separately

Consider a buyer in escrow on a purchase agreement with a contingency provision for the origination of mortgage financing necessary to fund the purchase price. The provision contains no parameters for acceptable terms of the new funding.

When the mortgage lender forwards the note and trust deed documents for the buyer to sign and return before funding, the buyer rejects the mortgage terms. The interest rate and payment schedule set by the lender in the closing documents are greater than orally represented by the mortgage loan originator (MLO) and do not support the price the buyer agreed to pay.

The buyer instructs escrow to prepare instructions to cancel escrow and the purchase agreement and return all funds and documents – instruments – to the participant who deposited them with escrow. The seller refuses to cancel the purchase agreement or reduce the sales price, but agrees to cancel only the escrow instructions. The seller claims the buyer seeks to cancel the purchase agreement to avoid paying the agreed price since comparable properties are now selling for a lower price.

Here, the cancellation of a purchase agreement is distinguished from both a unilateral or mutual cancellation of the escrow instructions. The cancellation of only the escrow instructions does not cancel the purchase agreement which continues in effect.

Often, due to a dispute or failure of a contingency, escrow will not close. Here, escrow issues instructions calling for the return of funds and documents to the participants who deposited them in escrow, part of the provisions canceling escrow instructions.

These escrow cancellation instructions, signed by both the buyer and seller, need not but may provide for cancellation of the purchase agreement. When the purchase agreement is not referenced as cancelled, the cancellation instructions handed to escrow do not interfere with any rights the participants may have to enforce the purchase agreement. Thus, the purchase agreement remains intact to be enforced to buy, sell or recover money losses since it has not been cancelled or rescinded, just escrow. [Calif. Civil Code §1057.3(e)]

Negotiations by the transaction agent to resolve the misunderstandings or differences and close escrow might not be successful. When the purchase dispute is unresolvable, the agents need to consider advising the buyer and seller to terminate not only escrow, but the purchase agreement as well. On cancelling both documents, the property is released and placed back on the market by the seller — and the buyer is free of obligations to the seller.

When the buyer and seller terminate the transaction, it is in everyone’s best interest for the buyer and seller to also release each other, the brokers and escrow from any claims they may have against one another. They do so by entering into a cancellation, release and waiver agreement to put the transaction to rest forever. [See RPI Form 181]

Cancellation for a valid reason

A seller or buyer occasionally refuse or are unable to hand escrow the instruments (funds and documents) needed to close the transaction in compliance with escrow instructions. Unless their nonperformance is excused, they have breached the purchase agreement.

Nonperformance is excused and the refusal to act is not a breach of the purchase agreement, when:

- a contingency provision exists authorizing the buyer or seller benefitting from the contingency to terminate the purchase agreement on the failure of an event to occur or on disapproval of data, information, documents or reports;

- the event fails to occur or the condition reviewed is disapproved; and

- the person authorized or benefiting from the contingency provision acts to terminate the agreement by delivering a notice of cancellation prior to the expiration of their right to cancel. [See RPI Form 183]

When a valid reason exists which triggers the buyer’s or seller’s right to exercise their right to cancel and they choose not to timely serve a notice of cancellation on the other participant, their right to be excused from further enforcement of the transaction expires.

Related article:

Conduct less than disapproval

Consider a buyer who enters into a purchase agreement to acquire an income-producing property before a recovery from a recession has taken hold. A provision calls for the buyer to review and approve the operating income and expenses experienced by the property. The buyer is handed a property operating cost spreadsheet for review and approval, called an income and expense statement or an Annual Property Operating Data sheet (APOD). [See RPI Form 352]

The receipt of the data commences a period of review for the buyer to determine whether to exercise their right of approval.

The data tends to confirm the general information received by the buyer before making the offer. However, the breadth and depth in the detail of the information seems inadequate for a long-term investment, the price of which is based on the buyer’s capitalization (cap) rate.

The buyer’s agent asks the seller to supply additional data and information, including access by the buyer for a review of all supporting documents regarding the property’s operating history, including leases, unit occupancy rates, expense records, list of contracted service providers — the works.

The seller claims the buyer’s request for more data and documents constitutes disapproval of the information and a cancellation of the agreement since the information already handed over sufficiently discloses the property’s operating history.

The seller claims the deal is dead – cancelled – and they are no longer required to perform. The seller has back-up offers at a higher price which the seller has accepted based on cancellation of this sale.

Has the buyer, by seeking additional information, disapproved of the condition of the income and expenses, and thus exercised their right to terminate the agreement?